Aerosun's (SHSE:600501) Earnings Growth Rate Lags the 15% CAGR Delivered to Shareholders

Aerosun's (SHSE:600501) Earnings Growth Rate Lags the 15% CAGR Delivered to Shareholders

While Aerosun Corporation (SHSE:600501) shareholders are probably generally happy, the stock hasn't had particularly good run recently, with the share price falling 16% in the last quarter. On the bright side the returns have been quite good over the last half decade. After all, the share price is up a market-beating 98% in that time.

而当Aerosun公司(上海证券交易所:600501)股东可能总体上很满意,该股最近表现不是特别好,上个季度股价下跌了16%。从好的方面来看,过去五年的回报相当不错。毕竟,在这段时间里,该公司股价上涨了98%,涨幅超过了市场。

In light of the stock dropping 6.9% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive five-year return.

鉴于该公司股价在过去一周下跌了6.9%,我们希望调查更长期的情况,看看基本面因素是否是该公司五年来正回报的驱动因素。

See our latest analysis for Aerosun

查看我们对Aerosun的最新分析

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

在他的文章中格雷厄姆和多德斯维尔的超级投资者沃伦·巴菲特描述了股价并不总是理性地反映一家企业的价值。评估围绕一家公司的情绪变化的一个有缺陷但合理的方法是将每股收益(EPS)与股价进行比较。

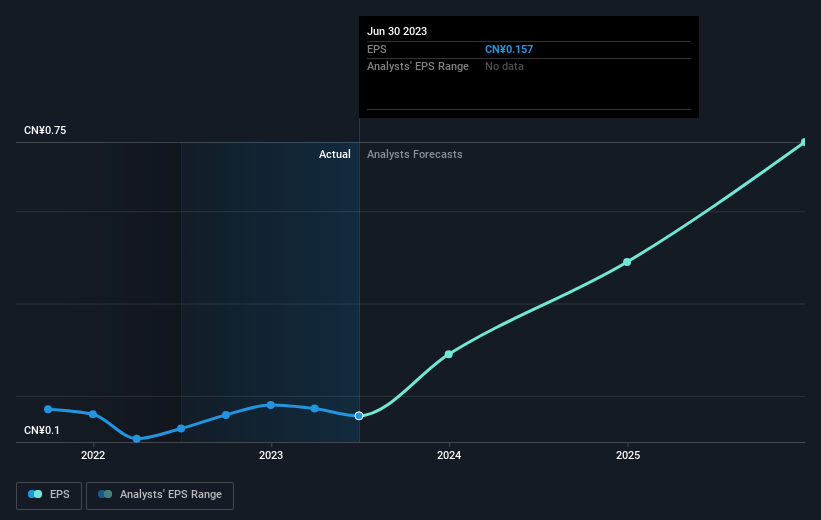

Over half a decade, Aerosun managed to grow its earnings per share at 33% a year. The EPS growth is more impressive than the yearly share price gain of 15% over the same period. So one could conclude that the broader market has become more cautious towards the stock. Of course, with a P/E ratio of 78.93, the market remains optimistic.

在过去的五年里,Aerosun的每股收益以每年33%的速度增长。每股收益的增长比同期15%的年股价涨幅更令人印象深刻。因此,人们可以得出结论,更广泛的市场对该股已变得更加谨慎。当然,市盈率为78.93倍,市场仍持乐观态度。

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

该公司的每股收益(在一段时间内)如下图所示(点击查看具体数字)。

We know that Aerosun has improved its bottom line lately, but is it going to grow revenue? This free report showing analyst revenue forecasts should help you figure out if the EPS growth can be sustained.

我们知道Aerosun最近提高了利润,但它会增加收入吗?这免费显示分析师收入预测的报告应该会帮助你弄清楚每股收益的增长是否可以持续。

A Different Perspective

不同的视角

It's good to see that Aerosun has rewarded shareholders with a total shareholder return of 9.3% in the last twelve months. And that does include the dividend. However, the TSR over five years, coming in at 15% per year, is even more impressive. The pessimistic view would be that be that the stock has its best days behind it, but on the other hand the price might simply be moderating while the business itself continues to execute. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. To that end, you should be aware of the 1 warning sign we've spotted with Aerosun .

很高兴看到Aerosun在过去12个月里回报了股东9.3%的总回报。这确实包括了股息。然而,五年来的TSR,以每年15%的速度增长,更令人印象深刻。悲观的观点是,该股的最佳时期已经过去,但另一方面,当业务本身继续执行时,价格可能只是在放缓。我发现,把股价作为衡量企业业绩的长期指标是非常有趣的。但为了真正获得洞察力,我们还需要考虑其他信息。为此,您应该意识到1个警告标志我们已经发现了Aerosun。

We will like Aerosun better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

如果我们看到一些大的内部收购,我们会更喜欢Aerosun。在我们等待的时候,看看这个免费最近有大量内幕收购的成长型公司名单。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

请注意,本文引用的市场回报反映了目前在中国交易所交易的股票的市场加权平均回报。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有什么反馈吗?担心内容吗? 保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

译文内容由第三方软件翻译。