Author: research

There is a kind of company that has a beautiful name called growth companies (growth company). Today we're going to talk about how to use the absolute valuation method-- that is,Discounted Cash flow Model-- valuing growth companies that can't make moneyI may use a company whose name begins with the word "Beijing" and ends with the word "East", purely for the sake of convenience.

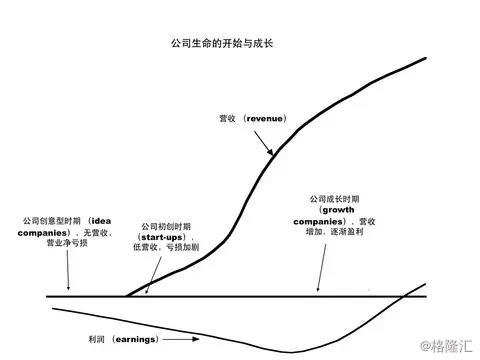

There are generally five kinds of companies that lose money for a long time and can't make money.Idea companies at midnight, start-ups at the fifth shift, growth companies at dawn, declining companies at sunset, and cyclical companies at the bottom of the cycle with a sudden solar eclipse.

Characteristics of growth companies

Some people look at whether a company is growing.Just go to see if the industry is a sunrise industry.For example, the IT information technology industry is now looking sunrise, so all IT companies are growth companies. This is, of course, a flawed argument that can be overturned by a counterexample:IBM is an IT company and IBM is a mature (if not declining) company rather than a growth company, so not all IT companies are growth companies.

Others (such as the financial encyclopedia website investopedia) say that thisA growth company is a company that can generate a large amount of cash flow or profit at a rate much higher than that of the overall economy. We can take another counterexample to let it go up in smoke, such as Tesla, Inc., who has not seen positive free cash flow in his quarterly report for nearly three years.。

The growth type is actually very difficult to define. Of course, you can use your own figures to fence and cut the boundary. You can say that in your mind, the sales revenue of the growth company will grow by at least 10% and the cash flow will grow by at least 15%. But there will always be a day when you have to be honest with your conscience: why 10% instead of 9.9%? Why 10% instead of 10 times the golden section of GDP growth?Just as you laugh at a buddy who is fat, your basis is certainly not that you know that he weighs more than 200jin or BMI more than 30, but by your precious natural ability to define a fat person; defining a growth company is also not a scientific quantitative process, but most of the time is an art, is to take a feeling.

Let's try to refine the characteristics of a growth company:

The financial statements have changed, and revenue, operating profit, EBITDA, EBIT, net profit, cash flow and so on are all in seemingly endless turmoil.

The market value of corporate equity is much higher than its book value. Make up a sexy word called scale deviation. There may be only hundreds of billions of shareholders' equity on the balance sheet, but the market capitalization of stocks may be tens of billions.

The debt is relatively light. Of course, this is not absolute, and some growth companies may be highly leveraged. But generally speaking, the debt leverage of growth companies is much lower than that of mature companies in the same industry. It's not that they don't want to borrow, it's just that they can't afford it, and the cash flow is not enough to cover interest payments from high leverage.

The company's "market history" is often short, and even though the company may have been established for many years and has been successfully listed, the traceable "market history" with data records is still very short.

Careful readers may have found that there is no mention of the word "growth" in these features, but in fact "The "growth" gene has been hidden in it.. For example, if a company's financial statements change its face, if a company's financial affairs are steadily rising, it is likely to be mature; if a company's financial affairs are very stable and deteriorating, it is likely to be a declining type, and generally only growing financial personnel will cry and laugh; for example, the market value of a company's equity is much higher than its book value, generally because the market is willing to pay a premium for "growth". For example, the short history of the market shows that the company is in the early stage of the life cycle and reflects the growth.

Give an example. It's our big JD.com $(JD) $coming out:

Financial report volatile √

Scale deviates from √

Debt saving √

Short market history √

With a little bit of artistic intuition, the growth type is you.

Valuation of growth companies

Corporate valuation is a huge topic, and even if we shrink to only talk about the valuations of growth companies, we still have to talk about the end of life. So I just want to talk about weird things in growth companies-- or normal ones, depending on how you feel about "growth"-- valuations of unprofitable growth companies, though, this remaining topic is probably beyond my lack of talent.

The perfect Logic of discounted Cash flow Model: the essence of Investment

The discounted cash flow model (discounted cash flow model,DCF model) is designed to pass theIt is logically impeccable to convert all future cash flows into present values to obtain the intrinsic value of assets (intrinsic value). It is a perfect thinking framework.You think, what is investment? investment is the act of expecting future cash inflows at the expense of immediate cash outflows. Now there is a slick marketing method is to deliberately confuse the two concepts of investment and consumption, for example, he will not sell you to "buy" a mink coat, but will encourage you to "invest" in a mink coat. You still think it sounds cool. But this is obviously not an investment behavior, because your mink clothes will not generate cash flow in the future, unless you buy it to be a bad guy.

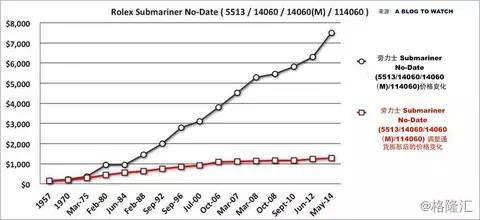

It just makes you feel good and then one more excuse to spend, such as "invest" in an LV or "invest" in a Tesla, Inc.. Stop deceiving yourself. However, there are some seemingly consumer behaviors that can be classified as investment, such as buying a Rolex. If you don't consume it in the safe, the Rolex Submariner No-Date you bought for $150 in 1957 has risen to $7500 in 2014; even after adjusting for inflation, the Rolex has risen from $150 to $1265, reaping a 750% inflation-adjusted return on investment. This performance is already very good, easily outperforming gold by about 400%, while the inflation-adjusted return of the s & p 500 is only about 900% over the same period. Of course, S & P also has countless trickles of dividends, which is far from comparable to Rolex, which has only one future cash flow.

So sometimes it is not only difficult to distinguish between investment and speculation, but also foolishly indistinguishable from consumption; but as long as we keep a close eye on the "future cash flow" in our eyes, as long as we understand how a certain model can recover cash flow with sufficient certainty in the future, generally speaking, this should be investment behavior.According to this line of thinking, we can see that the DCF model is only logically reliable: she understands the nature of investment and will never regard consumption as an investment. To answer how much an asset is worth (that is, want to know the intrinsic value), isn't this the immediate cash flow that I have to sacrifice to possess you now, and I have you for the purpose of getting cash flow in the future? Then I'll add up all the cash flows that may be generated in the future and I'll know how much it's worth.

Here we also have to accept a small inconvenience: cash flow has time value. I let you choose, either give you 100 yuan now, or give you 100 yuan a year later, people who follow the normal routine will definitely choose the former; even if I let you choose 100 yuan now or give you 110 yuan a year later, you are likely to choose to give it now.

On the one hand, due to the existence of inflation, the currency is expected to depreciate.

Second, cash flow has potential profitability, even if you just deposit it in the bank.

Third, from a human psychological point of view, a bird in the hand is better than a bird in the forest, or our nature is to have fun in time, if you have money or not, you must give me a reasonable explanation. Therefore, we have to give them a discount on the future cash flow, so as to know the present value of the future cash flow (present value).

How can I get a discount? We can consider an opportunity cost. For example, if I put my money in the most stable and safest Swiss government bonds in the universe, which has the lowest risk of default, I can harvest 2% a year (just assuming that Swiss government bonds are far lower than this), or if I have an opportunity to invest in a coal mine in Shanxi, I can earn 20 yuan a year after 100 yuan, that is, I can recover 120 yuan of cash flow in a year. Then I can't compare this 120 yuan to my initial 100 yuan, but I should compare it to the 102 yuan I would have recovered after a year of buying Swiss bonds if I hadn't done it. This 2% is called risk-free rate (risk-free rate). But in addition to the risk-free return discount, we also have to add a risk premium (risk premium) to this coal mine investment as a discount. after all, the psychological distortion caused by investing in Shanxi coal mines is not the same as that caused by investing in Swiss government bonds. The former may lead to a decline in the quality of my sleep, mood depression and sexual dysfunction, so I have to add another discount to compensate for my extra pain.

So in the simplest sense,Discount rate (discount factor) = risk-free rate of return + risk premium. Like the DCF model, this formula is hopelessly perfect in theory.

We have all the cash flow on one hand and a perfect discount rate on the other, so we can find the value of the asset through the discounted cash flow model. Although I once joked that writing articles should be based on storytelling, adding one more formula would hurt a thousand readers, but I risked death to add this formula, which is, after all, the logical cornerstone of the DCF model. To organize a sentence in the language of a liberal arts student, that is, the value of assets is equal to the sum of the present value of all future cash flows after discounts.

Some people may have a question. How can you know the sum of all the cash flows? If I buy a piece of land, and this vast and fertile land can produce 5000 pieces of cash flow every year, and there are endless children and grandchildren, how can you make peace? This is financially called perpetual annuity (perpetuity). For example, the cunning British government has introduced a bond called permanent bond (consols) to deceive onlookers, which will give you a yield of 3.5% a year forever (but the government has the right to recall at face value). On hearing this, many people think that Yoxi is very good, so the value of this bond is equal to infinity. It is too worthwhile to trade "limited" for "infinite", so they buy it. But in fact, mathematically, the present value of a perpetual annuity is very easy to calculate.

So a permanent bond with a face value of £1000 and an annual interest rate of 3.5%, if we assume a discount rate of 5%, is actually worth 35 ➗ 5% = 700 pounds.. If you pay 1000 pounds for the bond at first, it is impossible to trade "limited" for "infinite". It can only be regarded as "limited" in exchange for a bad head and paying a lot of IQ tax. Although the above two formulas have lost 2, 000 readers for me, I still think it is very necessary, because our absolute valuation of DCF depends on the success of these two guys. So how can we value the growth potholes that are not making money right now? In short, to do the three most important things:1. Open one hand and estimate all the free cash flow in the future; 2. Spread out the other hand to determine a reasonable discount rate; 3. Clap both hands and discount all future cash flows to the present value.

These three things are said in a few words, but it is as difficult to do as giving birth to a giant baby. it is from here that our resentment of "as deep as the sea of valuation" begins. Before this point, everything is perfect logic, thorough theory and exquisite models; after this point, everything is tricky practice, everything is suspicion and suspicion, everything is smoke and strife.

The dividing line between gunpowder smoke and dispute

1. What are the difficulties that valuation growth companies are likely to encounter?

In general, normal companies have profits, cash flow, a long history, and a lot of next-door companies that can be compared; and what we are dealing with now is unprofitable, no positive cash flow, short market history, and the growth type of the only other family in the universe, which causes multiple embarrassments for our valuation.

Awkward one: not making a profit.

If the company is operating at a loss and has no stable profits, it is difficult to estimate the growth rate of future profits; in addition, without profits, it is very difficult for you to defend the company's "sustainable operation". When we value the company, we usually acquiesce to a "going concern" assumption, that is, my valuation is based on the premise that you will not wake up this dream, otherwise the value of the company can only be equal to the scrap iron price that has been dismantled and sold. But if your company only bleeds but does not return blood, it is difficult for me to assume that you can continue to operate forever, because the possibility of bankruptcy is too high.

Awkwardness 2: the market history is short.

Although the financial industry is a web of lies, we occasionally encounter one or two straight truths in our investments, the most frequent of which is the sentence "Historical performance cannot predict future outcomes" written in all fund prospectuses. (Past performance does not necessarily predict future results.) having said that, when it comes to valuation, finance still has to turn to history for help. Without a long history, many things that require subjective evaluation are more like castles in the air, such as Beta (the volatility of the company's stock price relative to the market) when calculating the discount rate, because you can't make a regression model, and it's hard to estimate your cash flow and its growth rate.

Awkwardness 3: no similar.

If a company is in an industry with a row of competitors, the competitor will drive across from your house. Although her industry is bad, our valuation will be relatively easy, because we can use the competitor's data: for example, if we mentioned earlier that there is no Beta in the short history, an alternative is to find the Beta of companies of the same size in the same industry. If it were the only one in the universe-- which many growth companies have faced or are facing-- then the data would be much more likely to be guessed.

Give an example.

It's our big JD.com 's turn again. As of the second quarter of 2016, JD.com is famous for losing money. Throughout history, there was only a flash in the pan in one quarter in 2013 and losses at other times, so there have been endless voices that JD.com is going to be finished. JD.com 's market history is very short and has less than three years, so you can't even return to the most basic three-year Beta, let alone five and ten years. JD.com can directly compare very few competitors, even if there are, but because the e-commerce industry is booming in recent years, everyone is novice and everyone does not have data, so it is difficult for you to follow suit.

two。 How to overcome these difficulties?

Awkward one unprofitable solution number one: normalize profits.

If the company's profit is negative, you must not be able to calculate the profit growth rate, even if the loss is decreasing year by year; then one way is to "normalize profit" (normalized earnings), that is, we assume that the current situation of losing money year after year is abnormal and the company will eventually achieve a profitable state, so we answer a question: how much profit will the company generate in a normal year in the future?

Before we answer this relatively ultimate question, we have to answer a key question:Why is the company losing money now? Is it because the company is in a cyclical industry and the industry is at a low ebb? Is it because the company is expanding crazily and the early capital expenditure (capital expenditures) is too high? Is it because the company invests poorly and its assets are repeatedly impaired? Is it because the company is in short-term difficulties? Is it because the company's capital structure is unreasonable and the debt ratio is too high? Or is it because there are major problems in the company's long-term management?...

If it is a cyclical industry downturn, or the company's temporary capital expenditure is too high, or the company is in temporary difficulties, then we can normalize the company's profits.For example, cyclical industries can average early profits or return on capital, but companies that can grow rapidly at low ebbs are rarely seen here; or some companies can add back amortization if they lose money due to a large amount of amortization of intangible assets. Or there are temporary difficulties, such as exchange rate factors or some non-recurrent profit and loss items (extraordinary items), such as the collapse of the company building, which can be added back to achieve normal profits.

For example, our big JD.com, this guy's loss is not the loss of ordinary people, but the so-called "strategic loss", which means that I deliberately want to lose money, but I want to make a profit. I can make a profit right away.For example, JD.com suffered a crazy loss of 7.6 billion yuan in the four quarters of 2015, of which 2.5 billion was due to the asset impairment of shutting down the paddle network. in addition, it is the "strategic layout" of various O2O and financial businesses, as well as the impairment of intangible assets acquired from Tencent's business (East Brother's investment capacity.), to put it bluntly, these are one-time expenses, which can be added back if you have to normalize profits.

But I can't stand it, like JD.com, even if you add back a row of non-recurrent items, he will still lose money. There are other ways to deal with him for this evil, as will be said later. But at this point, some people may ask, aren't you trying to use the discounted cash flow model? why are you so obsessed with making a profit or not? just have cash flow.

This is because our goal is not to have the cash flow of the past, but to predict the cash flow of the future, and it is very important to have a "normalized" expectation of profitability in the future. "abnormal" enterprises that lose money year after year must not be sustainable, and the king must return at some point in the future.

Awkward one is not profitable solution two: the forecast of sales revenue X profit margin forecast.

Although it is not profitable, at least we do not lose revenue; as long as the business of your company is not to stand on the street and give money to people, then your revenue should be a positive number. And most of the growth companies can not grow, but the revenue will generally rise angrily, otherwise you have the nerve to go out and say you are a growth company?

Now that there is revenue, it will be easier. We can find some clues about the future revenue forecast.。First, look at the company's own revenue growth history (the more recent data, the more important); third, look at the growth trend of the industry as a whole; three times, see if the industry barriers are high enough and whether the company's own moat is deep enough. whether the current growth can be sustained; four times, to see if the company has any future revenue growth, to see if it can add another fire.

These are all subjective analyses, which need to be done by yourselves. For example, Big JD.com, you can see that sales revenue grew by 100%, 72%, 65% and 54% respectively from 2011 to 2015. Then take a look at the environment of e-commerce retail, O2O platform, financial services, cloud computing and other industries involved in JD.com 's ecosystem, and then look at JD.com 's position and competitive advantages and disadvantages in these industries. So you finally judge whether the current relative decline in revenue can be reversed or whether the high growth can be sustained, and finally judge how much revenue may be in the future, and so on. This article is about methodology, and the specific content of a certain company will not be filled.

The next step is to determine what the profit margin will be if the company gradually enters a healthy state of profit.. This can generally refer to the profit margins of other profitable companies in the same industry, and then go back to analyzing the company's own comparative advantage and moat (if any) to see if it is possible for the company to achieve higher profit margins than the industry average.

Of course, profit margins are not immutable. With the prosperity of business and the growth of scale, economies of scale (economies of scale, see below) are beginning to emerge (decreasing marginal costs, reducing the average cost of each additional product produced). Then this period may usher in a small spring of profit margins, which will gradually increase until "economies of scale" transition to "diseconomies of scale" (diseconomies of scale) If the company does not encounter anything at this time, it should gradually stabilize at a profit margin (sustainable margin). If the company's moat is deep enough, then the profit margin should be sustainable.

With a forecast of sales revenue on the one hand, a forecast of profit margin on the other, and a clap on the other, there is a profit forecast.

The solution of embarrassment two without history and three without embarrassment: mutual compensation and tricky market analysis

These two embarrassments can be combined to say that there is no history or there is no similar, if the two difficulties exist alone, then it is not so troublesome. Because history can compensate for the absence of the same kind, while the same kind can compensate for the absence of history.To value a company with no history, as long as there are many comparable peers in his industry, then everything can be light. For example, a fast food restaurant wants IPO listing, zero market history, but IPO pricing often does not have too much smoke, because the industry data is not too rich. Valuing a non-comparable company, as long as you have a long market history, pricing will not be easier than fast-food restaurant IPO, at least a wealth of historical data can compensate for the embarrassment of non-similar.

For example, JD.com, although the market history is very short and less than three years, in the industry, he is not completely the only one in the universe. There are Amazon.Com Inc, BABA and some domestic small breasts for reference. Although it can not be said to have 100% matching and comparability, but at least there is a line and outline. So some data, such as Beta, although the company can not get its own, to build an industry average is also alive, valuation, is a constantly make do with the art.

The most annoying thing is that these three non-enterprises: no profit, no history, no similar, valuation is the most likely to become metaphysics.

For these companies, we still need to use the methods mentioned earlier to predict future earnings and cash flow:

Use the latest financial data, or at least give more weight to the latest data when analyzing, because the financial situation of such companies looks like a doll's face in April.

It is expected that the growth of sales revenue, if there is no history and no similar, we should pay more attention to the analysis of the overall segment of the industry, since there is no such kind of market, it is likely to be a very niche market (niche market).

Expected sustainable profit margin

Anticipate the company's reinvestment needs, such as the need for capital investment and the addition of working capital (working capital), and so on.

In essence, all the revolutionary efforts we have made so far are to anticipate future cash flow. The free cash flow of a company can be calculated through the third formula in this article below. Of course, some other free cash flow formulas start with profit before interest and tax (EBIT) or operating cash flow (cash from operating activities), which are essentially the same. I won't enumerate them all, otherwise too many formulas are easy to cause riots.

Here is one thing to explain. There are generally two ways to discount cash flow:One is to calculate the cash flow that the fellow shareholders can share, and then calculate the "value of equity", which is the so-called discounted equity free cash flow method (free cash flow to equity, FCFE). The other is to calculate the cash flow enjoyed by the shareholders and the creditors of the company (that is, the cash flow of the whole company, FCFF), then calculate the "value of the whole company", and then divest the company's debt, and the rest is the equity value.. The FCFF above refers to the latter way of thinking. Some people may have several puzzles about this FCFF formula.

1. Why add back non-cash expenses?

Color text because non-cash expenses do not affect cash flow, for example, your goodwill is impaired by 5000 yuan, you do not have a direct cash loss of 5000 yuan, the real cash outflow actually occurred at the time of the acquisition that year.

two。 Why add back the after-tax interest expense? You can think about it from two angles:

Because the FCFF we calculate is the cash flow belonging to the shareholders + creditors of the company, and the interest expense is the cash belonging to the creditors, it should be added back after excluding the influence of the tax shield.

Because the cost of debt financing is already included in our discount rate, if the interest expense (a kind of debt financing cost) is excluded from the cash flow at the same time, it is tantamount to two consecutive discounts, repeated discounts.

3. Why subtract capital expenditure and operating additions?

Because this is the real cash flow that you really spend over a period of time. Fully understand these three reasons, this seemingly ghostly formula will not be forgotten.

Let's invite out our big JD.com again. If we put in the formula, we can get the frame model in the following figure. The formula I use is FCFF =[EBIT * (1-Tax)]+ NCC-Inv LT-Inv WC, this is just a simple modification of the above formula, which can be laughed off. Please just look at my valuation framework and reiterate that this article is an introduction to methodology and does not make a serious valuation for JD.com. In addition to the known financial data from the 2015 report, many of the figures in the table that need to do homework and subjective judgment are randomly filled in. Please do not believe that if you believe me, it is very difficult for you to hunt me down in the United States anyway.

So now that we have the FCFF every year, all we have to do is press the calculator with our fat hands and fold them into present value. But there is also the problem of terminal value, that is, if my company continues to operate forever, I can get cash flow all the way to the end of my children and grandchildren. So, the price formula of the perpetual annuity P=C/r mentioned before can come out to show off now, but we have to make a key adjustment, because the perpetual annuity mentioned earlier is not rising, 35 pounds a year is paid to the end of life; but the free cash flow of our company, generally speaking, with the development of human society, it must grow more or less, then we can not directly apply P=C/r, how to do?

It's all right, the sages have paved the road for us:The final value of the n-year free cash flow = FCFF/ of the n + 1 year, where g is the sustainable growth rate of the cash flow. This is the famous Gordon growth Model (Gordon growth model).I won't show up about the derivation of the formula, otherwise there won't be any readers left.

When choosing a sustainable growth rate, I have only one suggestion: be taut, don't be too bold, or it will easily lead to miracles. I had an article earlier that Evernote, an investment bank, used a sustainable growth rate of 6% and 8% when valuing Tesla, Inc.. This is simply an industry joke. I don't know on which planet such sustainable growth can be realized. If you set sustainable growth abnormally high, the final value will be huge. I personally suggest that we try not to let sustainable growth outpace the growth of the economy as a whole, because how strong a company has to be in order to keep growing faster than the economy in which it lives.

Then when we find out the sum of all the discounted free cash flow, we can add back the company's current cash, subtract the debt, and then subtract the value of the options issued by the company, which is equal to the current equity value for the company's shareholders.Divided by the total share capital, it is the so-called intrinsic value of each share. This is the gold smash that we have been panning for a long time, of course, it is also likely to be a bubble.

Discount rate and original sin of DCF model

The topic of discount rate is so big that I'm going to save it for the next article; this one is long enough, maybe too long. In the above framework, I randomly filled in the discount rate of 15% and 10%, just to satisfy the integrity of a model. People will say, "Yo, not bad?" you calculate the intrinsic value of 33.93 yuan, which is quite close to the current price, good job well done;, but I must be clear:I'm sorry, I actually transferred this figure back and forth. If you want 100 yuan, I can transfer 100 yuan to you.

This is the biggest sin of the discounted cash flow model, which is why I generally don't pay much attention to the investment bank's DCF estimate of a stock, because the trick is too heavy.As I said earlier,The thinking logic of DCF model is actually very perfect, but in practical application, there will be too many assumptions and predictions, and there will be too much smoke and disputes.For example, the two key variables, "growth rate" and "discount rate", simply control the final output of the model; in addition, it is often several orders of magnitude more difficult to predict the future than we think, and your predicted future cash flow may actually be a mirage.

If investment bank analysts want to convince you that Jingdong is worth 50 yuan, they can use reverse engineering to make a model with a result of 50 yuan, and then sell it to you shamelessly; so you must be careful about these analysis reports. to keep questioning their assumptions and predictions, to maintain a highly skeptical heart, as to how black they can be and how evil they can be. So it is not so much DCF's original sin as man's original sin, the model she is innocent, she is flawless.

However, the thinking training of absolute valuation is still very useful for us to understand the company's business model and financial data. If your assumptions and forecasts come from in-depth research and solid data, and if you are conservative enough, then your valuation results still have good reference significance. Of course, such a model is absolutely necessary without sensitivity analysis, we can create many future parallel universes, according to different assumptions and predictions, different scenario to simulate different valuation results, and then we can look at their distribution; I can not say that this kind of simulation will certainly enable us to find the intrinsic value of the company, but at least it will bring us closer.