UTS Marketing Solutions Holdings Limited (HKG:6113) shareholders have had their patience rewarded with a 33% share price jump in the last month. Unfortunately, despite the strong performance over the last month, the full year gain of 3.8% isn't as attractive.

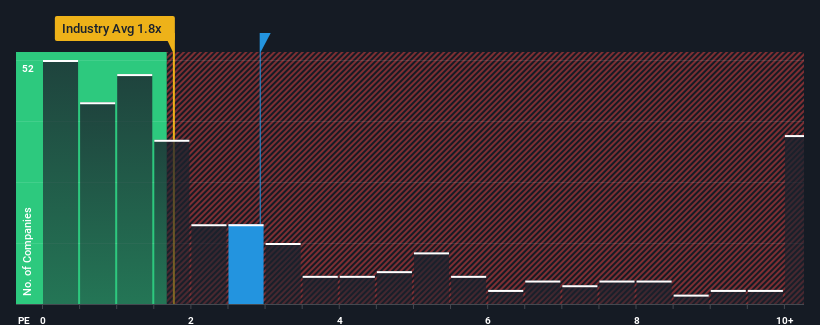

Since its price has surged higher, you could be forgiven for thinking UTS Marketing Solutions Holdings is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 2.9x, considering almost half the companies in Hong Kong's Professional Services industry have P/S ratios below 0.5x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for UTS Marketing Solutions Holdings

SEHK:6113 Price to Sales Ratio vs Industry September 11th 2023

How UTS Marketing Solutions Holdings Has Been Performing

For example, consider that UTS Marketing Solutions Holdings' financial performance has been pretty ordinary lately as revenue growth is non-existent. It might be that many are expecting an improvement to the uninspiring revenue performance over the coming period, which has kept the P/S from collapsing. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on UTS Marketing Solutions Holdings will help you shine a light on its historical performance.

What Are Revenue Growth Metrics Telling Us About The High P/S?

In order to justify its P/S ratio, UTS Marketing Solutions Holdings would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Fortunately, a few good years before that means that it was still able to grow revenue by 13% in total over the last three years. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 10% shows it's noticeably less attractive.

With this information, we find it concerning that UTS Marketing Solutions Holdings is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

Shares in UTS Marketing Solutions Holdings have seen a strong upwards swing lately, which has really helped boost its P/S figure. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

The fact that UTS Marketing Solutions Holdings currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

We don't want to rain on the parade too much, but we did also find 5 warning signs for UTS Marketing Solutions Holdings (1 shouldn't be ignored!) that you need to be mindful of.

If you're unsure about the strength of UTS Marketing Solutions Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

UTS Marketing Solutions Holdings Limited(HKG: 6113)股东们的耐心在上个月股价上涨了33%。不幸的是,尽管上个月表现强劲,但3.8%的全年涨幅并不那么吸引人。

由于其价格飙升,考虑到香港专业服务行业中将近一半的公司的市盈率低于0.5倍,你认为UTS Marketing Solutions Holdings是一只值得避开的股票,其市售比率(或 “市盈率”)为2.9倍,这是可以原谅的。尽管如此,我们需要更深入地挖掘,以确定高涨的市盈率是否有合理的基础。

查看我们对悉尼科技大学营销解决方案控股公司的最新分析

香港联交所:6113 市售比率与行业对比 2023年9月11日

UTS Marketing Solutions Holdings Limited的表现如何

例如,考虑一下UTS Marketing Solutions Holdings最近的财务表现相当普通,因为收入没有增长。许多人可能预计,未来一段时间内平淡无奇的收入表现会有所改善,这使市盈率无法暴跌。如果不是,那么现有股东可能会对股价的可行性有些紧张。

想全面了解公司的收益、收入和现金流吗?然后我们的 免费的 UTS Marketing Solutions Holdings的报告将帮助您了解其历史表现。

收入增长指标告诉我们关于高市盈率的哪些信息?

为了证明其市盈率是合理的,UTS Marketing Solutions Holdings需要实现远远超过该行业的出色增长。

首先回顾一下,我们发现,在过去的一年中,该公司几乎没有任何收入增长可言。幸运的是,在此之前的几年里,它仍然能够在过去三年中将总收入增长13%。因此,可以公平地说,该公司最近的收入增长一直不稳定。

将最近的中期收入趋势与该行业10%的一年增长预测进行比较,可以看出它的吸引力明显降低。

有了这些信息,我们发现UTS Marketing Solutions Holdings的市盈率高于该行业,这令人担忧。显然,该公司的许多投资者比最近所显示的要看涨得多,他们不愿意不惜任何代价放弃股票。如果市盈率降至更符合近期增长率的水平,现有股东很有可能为未来的失望做好准备。

最后一句话

UTS Marketing Solutions Holdings的股价最近出现了强劲的上涨,这确实有助于提高其市盈率。我们可以说,市售比率的力量主要不在于作为一种估值工具,而是用来衡量当前的投资者情绪和未来预期。

UTS Marketing Solutions Holdings目前的市盈率高于该行业,这一事实很奇怪,因为其最近三年的增长低于整个行业的预测。当我们观察到收入增长慢于行业且市盈率高时,我们假设存在股价下跌的巨大风险,这将导致市盈率降低。除非公司的中期业绩有显著改善,否则很难防止市盈率下降到更合理的水平。

我们不想在游行队伍中下太多雨,但我们也发现了 悉尼科技大学营销解决方案控股公司的5个警告信号 (1 不应该被忽视!)这是你需要注意的。

如果你是 不确定悉尼科技大学营销解决方案控股公司的业务实力,为什么不浏览我们的互动股票清单,为你可能错过的其他一些公司提供坚实的商业基本面。

对这篇文章有反馈吗?担心内容吗? 请直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St 的这篇文章本质上是笼统的。 我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。 它不构成买入或卖出任何股票的建议,也没有考虑您的目标或财务状况。我们的目标是为您提供由基本面数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感公司公告或定性材料。简而言之,华尔街在上述任何股票中都没有头寸。