Is Planet Green Holdings Corp (PLAG) Significantly Overvalued?

Planet Green Holdings Corp (PLAG) recorded a daily gain of 16.77%, and a three-month gain of 57.89%. However, it reported a Loss Per Share of $0.56. This prompts the question: Is the stock significantly overvalued? In this article, we will delve into the valuation analysis of Planet Green Holdings (PLAG) to answer this question.

A Snapshot of Planet Green Holdings Corp (PLAG)

Planet Green Holdings Corp operates in North America and China, offering a diverse range of products and services in the Chemical Products, Tea Products, and Online Advertising Services sectors. Despite its current stock price of $0.78, our analysis suggests that the fair value (GF Value) of the stock is around $0.48. This indicates a significant overvaluation of the stock.

Understanding the GF Value

The GF Value is a proprietary measure of a stock's intrinsic value. It is calculated considering historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. The GF Value Line denotes the stock's ideal fair trading value.

Currently, the GF Value of Planet Green Holdings (PLAG) suggests that the stock is significantly overvalued. The stock price is likely to fluctuate around the GF Value Line. If the price is significantly above this line, it indicates overvaluation, and its future return is likely to be poor. Conversely, if the price is significantly below the GF Value Line, its future return will likely be higher.

Given that Planet Green Holdings is significantly overvalued, the long-term return of its stock is likely to be much lower than its future business growth.

Assessing Financial Strength

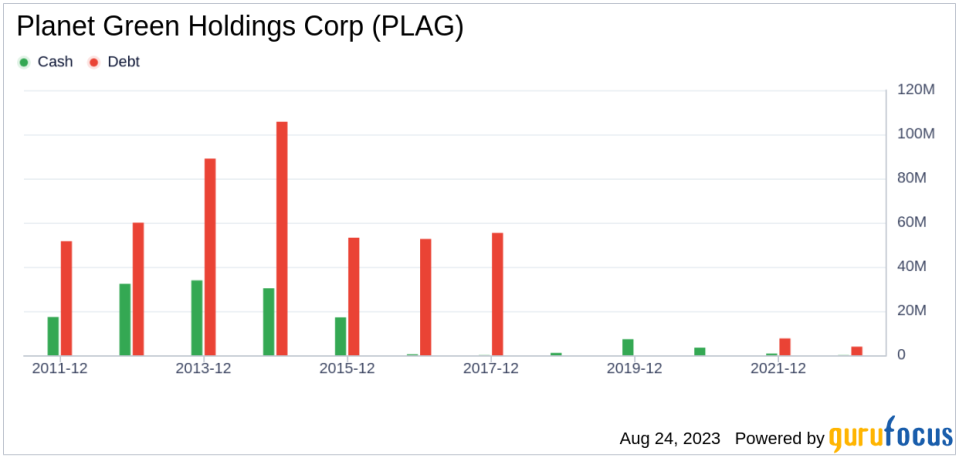

Investing in companies with low financial strength could result in permanent capital loss. Planet Green Holdings has a cash-to-debt ratio of 0.19, ranking worse than 67.88% of 1759 companies in the Consumer Packaged Goods industry. This suggests a poor balance sheet and low financial strength.

Profitability and Growth

Planet Green Holdings has been profitable for 5 out of the past 10 years. However, its operating margin of -16.78% ranks worse than 87.95% of 1818 companies in the Consumer Packaged Goods industry, indicating poor profitability.

On the growth front, Planet Green Holdings's 3-year average revenue growth rate is better than 96.97% of 1714 companies in the Consumer Packaged Goods industry. However, its 3-year average EBITDA growth rate is -157.1%, ranking worse than 99.15% of 1523 companies in the same industry.

ROIC vs WACC

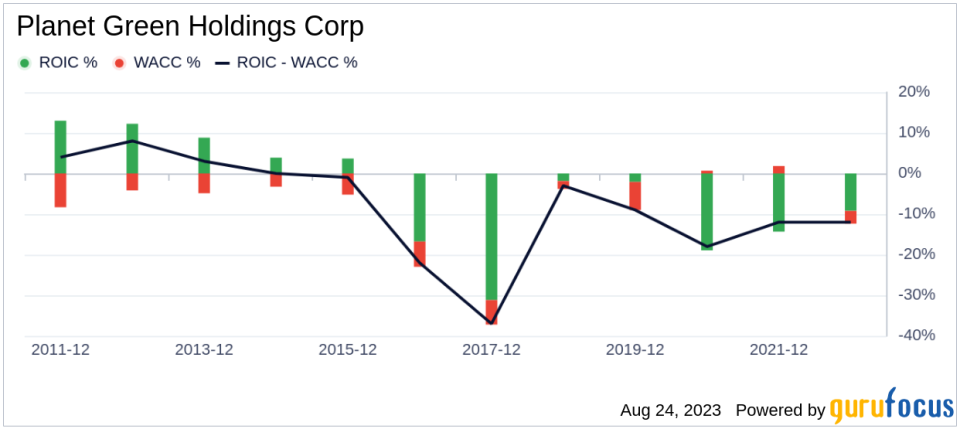

Comparing a company's Return on Invested Capital (ROIC) to its Weighted Average Cost of Capital (WACC) can provide insights into its profitability. Over the past 12 months, Planet Green Holdings's ROIC was -8.66, while its WACC was 7.08, suggesting that the company is not creating value for shareholders.

Conclusion

In conclusion, the stock of Planet Green Holdings appears to be significantly overvalued. The company's financial condition is poor, its profitability is poor, and its growth ranks worse than 99.15% of 1523 companies in the Consumer Packaged Goods industry. To learn more about Planet Green Holdings stock, you can check out its 30-Year Financials here.

To find out high-quality companies that may deliver above-average returns, please check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.