Author: Ren Zeping Ganyuan Shi Lingling

Source: Zeping Macro

Event

On May 17, 2019, the central bank released its monetary policy implementation report for the first quarter of 2019.

Unscramble

1. Core ideas:

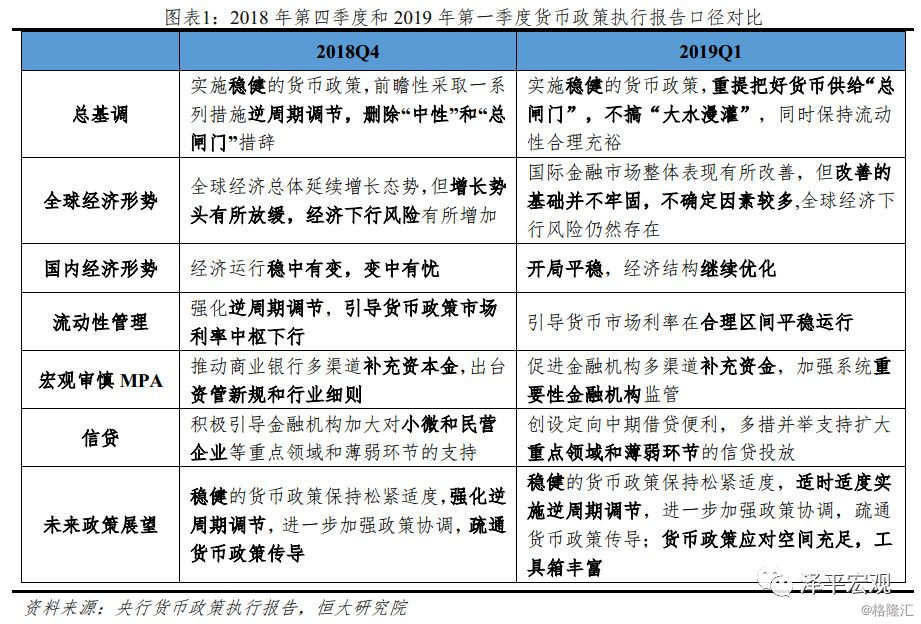

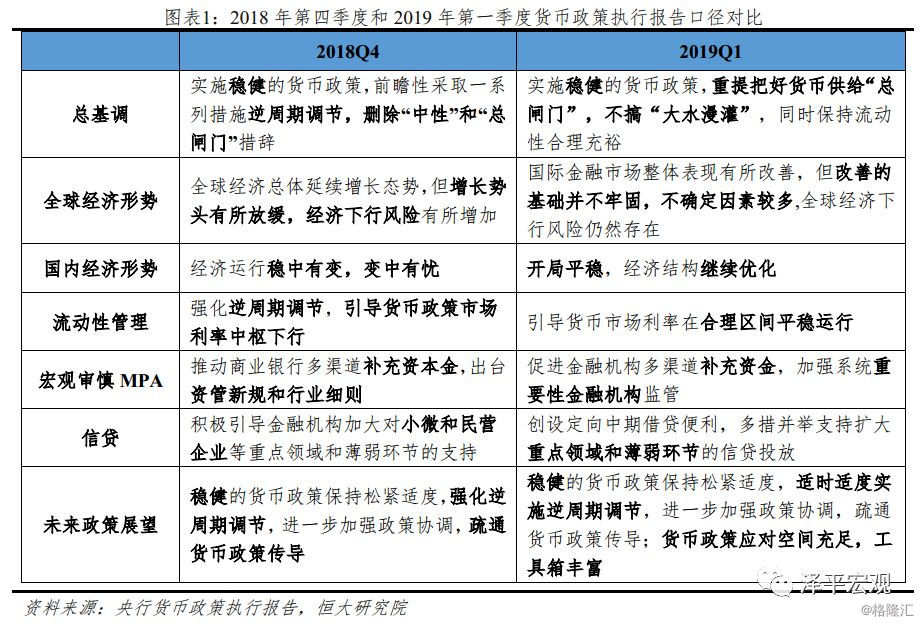

1) the central bank mentions the "main floodgate" of money supply again.It is stressed that prudent monetary policy should be kept loose and tight, while adhering to the general tone of striving for progress in stability, and keeping liquidity reasonable and abundant. In additionThe central bank highlighted the structural reform on the financial supply side and proposed that more attention should be paid to dredging the transmission of monetary policy in the next stage.Efforts should be made to solve the problems of difficult and expensive financing. In the face of the escalating trade war between China and the United States, the best response is not the release of money, but reform and opening up.

2) China's economy got off to a smooth start in 2019, and macroeconomic indicators remained within a reasonable range. But it's important to note thatThere is still downward pressure on the domestic economy, and these factors are not only cyclical, but also structural and institutional. At present, economic growth is mainly supported by real estate and infrastructure investment.The transformation of the new and old momentum of economic growth will be accelerated, and the endogenous driving force of economic growth needs to be further strengthened.

3)From the perspective of exchange rate, the RMB exchange rate has depreciated sharply recently.In the short term, under the influence of the slowdown in global economic growth and the resurgence of Sino-US trade frictions, the RMB exchange rate is gradually weakening; in the long run, the export growth rate continues to be under pressure, and the RMB exchange rate faces the risk of increased volatility, but there is no basis for substantial depreciation.

4) from the price point of view, the current domestic price situation is generally stable, but the uncertain factors have increased.In the future, it is necessary to better achieve a better macroeconomic combination of steady economic growth, stable prices and basically stable macro-leverage ratio.

5) the momentum of global economic growth has weakened, and the growth momentum of major developed economies has slowed slightly.International financial markets improved in the first quarter of 2019, but the foundation is not solid. From the perspective of the international environment, the world economic situation is complex, geopolitical risks are still large, the external economic environment is generally tightening, trade frictions are still significant risks, and downside risks to the global economy still exist in the future.

6)At present, the central bank believes that China's monetary policy has sufficient space to deal with, rich toolboxes, and the ability to cope with internal and external uncertainties.In the next stage, we should deepen the structural reform on the financial supply side and further dredge the transmission channels of monetary policy.We will innovate monetary policy tools and mechanisms, reduce the financing costs of the real economy, especially small and micro enterprises, and improve the ability and willingness of financial services to the real economy.

2. The central bank puts forward the "general floodgate" again, emphasizing that the prudent monetary policy should be kept loose and tight, while adhering to the general tone of seeking progress in the midst of stability, and keeping liquidity reasonable and abundant. In addition, the central bank will deepen the structural reform on the financial supply side, dredge the transmission of monetary policy, and strive to solve the problem of difficult and expensive financing.

First, the central bank mentioned the "floodgates" again, pointing out that monetary policy should not engage in "flooding". At the same time, it should also maintain reasonable and abundant liquidity, timely and appropriately implement counter-cyclical adjustment, and timely pre-adjust and fine-tune according to economic growth and changes in price forms.The deletion of the word "floodgate" by the central bank in the fourth quarter of 2018 reflects the sound and loose tone of monetary policy from the fourth quarter of last year to the first quarter of this year, but the return of the "floodgate" in the first quarter shows that the central bank will not invest money on a large scale and will not engage in "flooding", so it is less likely for the central bank to loosen monetary policy significantly in the short term.We believe that in the future, macro policies should not only prevent hedging from being untimely and insufficient, but also prevent excessive efforts and going back to the old path.

Second, the central bank believes that there are many favorable factors for China's economy to maintain steady development, but there is still downward pressure. These factors are not only cyclical, but more structural and institutional.Compared with the judgment of "changes in stability and worries in the course of change" in the fourth quarter of 2018, the central bank believes that the current economy still needs to solve structural and institutional problems.We believe that in the future, it is still necessary to further mobilize the enthusiasm of local governments and entrepreneurs to promote a new round of reform and opening up.

Third, the central bank focuses on "structural deleveraging", increasing support for private enterprises and small and micro enterprises, reducing the leverage of local governments and state-owned enterprises, deepening structural reform on the financial supply side, and improving the quality and efficiency of the real economy of financial services.The central bank believes that a sound monetary policy will help to find a balance between debt stock and increment, total leverage and structure, and provide an appropriate macroeconomic, monetary and financial environment for structural deleveraging. At present, it is necessary to deepen financial supply-side reform, properly use structural monetary tools, give full play to the role of "precision drip irrigation", increase support for private enterprises and small and micro enterprises, and lower the leverage of local governments and state-owned enterprises as soon as possible. efforts should be made to achieve a stable and gradual decline in macro leverage.

3. China's economy got off to a steady start in the first quarter of 2019, and macroeconomic indicators remained within a reasonable range. However, it should be noted that there is still downward pressure on the domestic economy, and these factors are not only cyclical, but more structural and institutional. At present, economic growth is mainly supported by real estate and infrastructure investment, the transformation of new and old momentum of economic growth is accelerated, and the endogenous driving force of economic growth needs to be further strengthened.

First, China's economy is off to a steady start, but there is still downward pressure on the domestic economy. These factors are cyclical, but more of them are structural and institutional problems, and we must further readjust the structure and promote reform.At present, this inventory cycle is in the early stage of recovery from active destocking to passive destocking, and in the second half of the financial cycle, the leverage ratio of enterprises, residents and local governments is on the high side, and the ability to continue to add leverage is restricted. Most of these factors are structural and institutional. To further adjust the structure and promote reform, on the one hand, we should continue to promote the supply-side structural reform of finance, promote the steady deleveraging of state-owned enterprises and local governments, and achieve a stable and gradual decline in the macro leverage ratio. On the other hand, we will continue to expand the opening up of the financial industry to the outside world and build a diversified financial system.

Second, the momentum of domestic economic growth has been transformed, and the momentum of endogenous economic growth needs to be further strengthened.Since the first quarter, the growth of manufacturing and private investment has slowed, which is still supported by real estate and infrastructure investment, and the endogenous growth momentum needs to be further strengthened. In the next stage, we need to adhere to the general tone of seeking progress in the midst of stability, implement the eight-character principle of "consolidation, enhancement, upgrading, and smooth flow", and pay attention to stabilizing demand by means of supply-side structural reform. Innovate monetary policy tools, consolidate the foundation from both sides of supply and demand, and promote the smooth transformation of economic growth momentum.

Third, the economy is mainly supported by real estate and infrastructure investment.Since the beginning of this year, real estate investment has maintained high growth against the cycle, but consumption, import and export, and manufacturing investment have all been in the doldrums, and the economy is still highly dependent on real estate and infrastructure investment. Fixed asset investment rose 6.1% from January to April compared with the same period last year, down 0.2 percentage points from January to March. In terms of the growth rate of the same month, fixed asset investment grew by 5.7% in April, down 0.7 percentage points from March, which is related to the weakening of the marginal adjustment policy against the cycle in April, including the obvious slowdown in local bond issuance compared with the first quarter, the seasonal decline in social finance credit, and so on. Real estate investment continued to rise and infrastructure remained stable, but manufacturing investment and private investment declined.

We believe that the economic and financial data from January to April show that the current economy continues to stabilize but the rebound is weak, mainly because the weaker inventory cycle is suppressed by the second half of the financial cycle. it is in line with our judgment that "the economy hit bottom in the middle of the year, before low and then stable (rather than before low and then high)". Business expectations are still high, prices have rebounded, profits have improved, the inventory cycle has shifted from active destocking to passive destocking, the follow-up broad money to broad credit will continue to be smooth, and investment is expected to stabilize in the second half of the year, but because monetary policy is not flooding, it will not rise sharply.

4. RMB exchange rate weakens periodically in the short term, and there is no basis for substantial depreciation in the long run.

Affected by the slowdown in global economic growth and the resurgence of trade frictions between China and the United States, the RMB exchange rate faces short-term depreciation pressure; however, in the long run, export growth continues to be under pressure, and the RMB exchange rate faces the risk of increased volatility, but there is no basis for substantial depreciation.1) the marginal external demand is picking up but still weak.In April, the global manufacturing PMI index fell for the 12th month in a row; in developed economies, the US manufacturing PMI was 52.6% in April, up 0.2 percentage points from the previous month; and the European manufacturing PMI was 47.9%, up 0.4% from the previous month, but remained below the decline line for three consecutive months. The monthly average of BDI freight in April was-31.5% year-on-year, compared with 13.6% month-on-month; South Korea's exports in April were-2% year-on-year, negative for five consecutive months. 2) China's new export order index of PMI in April is 49.2%, which is still below the rise and fall line although it has picked up.2) Trade frictions between China and the United States make waves againTrump began imposing tariffs on 200 billion US dollars of Chinese goods imported to the United States on May 10, raising the tariff rate from 10 percent to 25 percent, and proposed imposing tariffs on another 325 billion dollars of goods in the short term, bringing Sino-US trade negotiations back to tension. Enterprises are faced with uncertainty, which will accelerate the transfer of the industrial chain and cause a drag on subsequent exports.3) however, the depreciation of the RMB exchange rate supports exports.。Since the Sino-US trade friction continued to escalate in 2018, the RMB exchange rate has depreciated, and the RMB has continued to depreciate recently. But in the long run, there is no basis for a sharp devaluation of the renminbi.

5. At present, the main factors of domestic price uncertainty are pig prices and oil prices, and we think inflation is expected to remain moderate this year.

The overall price situation is relatively stable, but uncertainties have increased, mainly due to pig prices and oil prices.Generally speaking, the recent economic operation is stable, the total supply and demand is basically balanced, and the core CPI is generally stable. Further progress has been made in supply-side structural reform and the problem of overcapacity has been significantly alleviated, which is conducive to keeping prices stable. However, it should also be noted that the recent classical swine fever epidemic in Africa, the gradual rise in international crude oil prices, the rebound in the prices of domestic oil products, steel, and other industrial products, and the different impact of tax reduction measures on the price index of different sectors will create uncertainty about the price level, and we still need to continue to pay attention to price changes in the future.

Whether it is appropriate to grasp the strength of a prudent monetary policy depends on whether monetary conditions match the requirements of steady economic growth and price stability.Over the past two years, China's economy has grown at an average annual rate of 6.7%. The average annual growth rate of GDP is 1.8%. The growth rates of M2, social integration and nominal CPI are 8.1%, 11.6% and 10.3% respectively. In the future, through the adjustment of prudent monetary policy, a better macroeconomic combination of steady economic growth, stable prices and basically stable macro-leverage ratio should be achieved.

The stabilization and rebound of CPI and PPI reflects the effectiveness of previous policies, and inflation is expected to remain moderate this year under the influence of internal and external factors.Both CPI and PPI rose month-on-month, reflecting the strength of both monetary and fiscal policies in the previous period, the restoration of entrepreneur confidence, the overall stabilization of the macro-economy in the first quarter, and the transformation of the inventory cycle from active destocking to passive destocking. In the short term, demand-driven headline inflation is unlikely, and inflation is expected to remain moderate. First, the pig cycle to promote CPI continued to rise in the main tone unchanged, the performance in the second half of the year is more obvious. Second, the foundation for economic stabilization is not solid, and the issuing speed of local government special bonds has slowed down, which restricts the continued rise in inflation. Third, the effect of value-added tax reduction will continue to be reflected.

6. the momentum of global economic growth has weakened, the growth momentum of major developed economies has slowed slightly, and downside risks to the global economy still exist.

From the perspective of the international environment, the world economic situation is complex, geopolitical risks are still large, the external economic environment is generally tightening, trade frictions are still significant risks, and downside risks to the global economy still exist in the future.Since the second half of 2018, the momentum of global economic growth has weakened, the growth momentum of major developed economies has slowed slightly, and the scope for policy response has been limited. In the first quarter of 2019, the overall performance of international financial markets improved, but the foundation for improvement is not solid, there are many uncertain factors, downside risks to the global economy still exist, and trade frictions and policy uncertainties are still significant risks.

The economic performance of the major developed economies is divided. The US economy is generally sound, but there are signs of a slowdown.Economic growth in the euro zone has slowed and uncertainty has increased. The volatility of the Japanese economy has increased, and inflation expectations are still low due to structural factors such as lack of incentive for companies to raise wages and low inflation expectations. The UK economy continues to grow at a low rate, and the uncertainty brought about by Brexit has increased. Emerging market economies are polarizing.

Since 2019, the expectations of international financial markets have improved, global stock markets rose in the first quarter and Treasury yields fell, but recent volatility has increased.The dollar index fluctuated higher, while the yen and euro depreciated against the dollar. Stock markets in major economies rebounded, but bond yields generally fell. Affected by factors such as the weakening of the Fed's expectation of raising interest rates, the dollar Libor of the London interbank lending market fell slightly.

Looking ahead, the multi-point outbreak of geopolitical conflicts and the accelerated accumulation of risk factors and uncertainties have brought new challenges to the global economy.First, the weakening growth prospects of major economies are a drag on global economic growth, which in the short term has weak momentum and limited room for policy response; second, trade frictions and policy uncertainties remain significant risks. in the future, trade frictions and policy uncertainties may push up inflation, damage household and business confidence, and trigger financial market fluctuations; third, a variety of uncertainties may be intertwined, which may amplify the vulnerability of economies.

At present, the central bank believes that China's monetary policy has sufficient space to deal with, rich toolboxes, and the ability to cope with internal and external uncertainties.In the next stage, it is necessary to deepen the structural reform on the financial supply side, further dredge the transmission channels of monetary policy, innovate monetary policy tools and mechanisms, reduce the financing costs of the real economy, especially small and micro enterprises, and improve the ability and willingness of financial services to the real economy.

It is necessary to deepen the structural reform on the financial supply side, adjust and optimize the structure of the financial system, and constantly improve financial services. In the face of changes in the internal and external economic environment, due to the current situation, more targeted implementation of macro-control, to promote the virtuous circle of the national economy. Therefore, it is necessary to achieve the following six points:

First, we should adhere to a prudent monetary policy and make timely pre-adjustments and fine adjustments in accordance with economic growth and changes in the price situation, so as to maintain reasonable and adequate liquidity and reasonable and stable market interest rates.The central bank believes thatIf monetary policy is too looseIt may lead to the disorderly expansion of new debt, leading to idling of funds and getting out of reality.If monetary policy is too tightIt may lead to excessive pressure on the repayment of stock debt, resulting in tight repayment in the credit and bond markets. Therefore, a sound monetary policy helps to find the balance between debt stock and increment, total leverage and structure, and provide an appropriate macroeconomic, monetary and financial environment for structural deleveraging.

Second, we should promote structural optimization and better serve the real economy.First, we should give full play to the role of monetary and credit policies in promoting economic restructuring and do a good job in financial support for supply-side structural reform. Second, we should make proper use of structural monetary tools, give full play to the role of "precision drip irrigation", and give market-oriented principles to improve support for key areas and weak links of the national economy, such as private enterprises and small and micro enterprises. optimize the financial supply to different sectors and different main bodies.We believe that in order to tie in with the financial supply-side structural reform and dredge the monetary transmission channels, targeted reserve rate cuts, MLF, PSL and other structural monetary instruments will become more and more important in the future.

Third, it is necessary to further deepen the marketization of interest rates and the reform of the RMB exchange rate formation mechanism, and steadily promote the "two-track integration" of interest rates.Strengthen the guiding function of the central bank policy interest rate system, improve the interest rate corridor mechanism, enhance the ability to regulate and control interest rates, focus on dredging the transmission of central bank policy interest rates to market interest rates, especially credit rates, and enhance the loan pricing ability of financial institutions. Appropriately enhance market competition and better serve the real economy.

Fourth, it is necessary to improve the financial market system and give full play to the role of the financial market in stabilizing growth, restructuring, promoting reform, and preventing risks.On the one hand, we should encourage commercial banks to replenish their capital through various ways, such as issuing permanent bonds, and continue to promote private enterprise bond financing support tools; on the other hand, we should actively promote the two-way opening of the bond market to create a more friendly and convenient investment environment for market participants.

Fifth, we should deepen the structural reform on the financial supply side, open wider to the outside world, and improve financial services by optimizing supply and increasing competition.First, it is necessary to optimize the financing structure, financial institution system, market system and product system, so as to provide high-quality and efficient financial services for the real economy. Second, it is necessary to deepen the reform of large commercial banks and financial enterprises and improve corporate governance. Third, we should continue to promote inclusive finance, stimulate the vitality of county business departments, and improve the ability and level of serving county economy. Fourth, it is necessary to implement the reform of financial institutions and policy banks of the Development Bank, and speed up the construction of development and policy-oriented financial institutions that serve the economy and operate sustainably.

Sixth, we should do a good job in the battle to prevent and defuse major financial risks.We will promote structural deleveraging in an orderly manner, pay attention to risk prevention on the basis of steady growth, better support the development of the real economy, guard against the risk of abnormal fluctuations in the financial market, accurately and effectively deal with risks in key areas, and pragmatically promote the reform and opening up of the financial industry.