Author: Zhongtai International Xu Bo

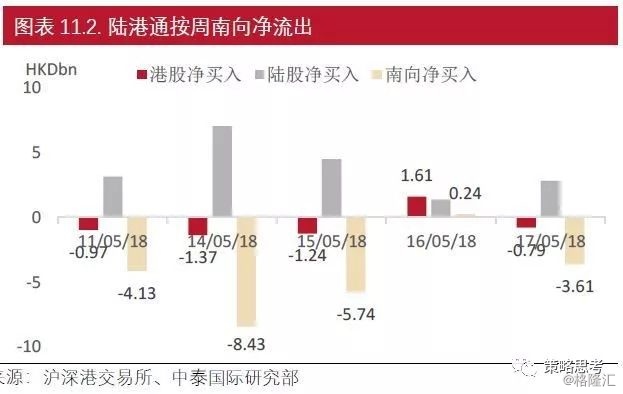

As of May 18, the MSCI global, developed and emerging market indices all retreated slightly, falling 0.73 per cent, 0.52 per cent and 2.3 per cent, respectively, on a weekly basis. The onshore index is slightly better than the offshore index, with the CSI 300 and Shanghai Composite Index rising 0.78% and 0.95% respectively on a weekly basis, while the Hang Seng Index and the State-owned Enterprise Index are basically flat on a weekly basis. In terms of valuation, the Hang Seng Index fluctuates around a standard deviation on the historical average. Stimulated by the inclusion of MSCI into A shares, Land Stock Tong and Hong Kong Stock Connect continued the pattern of net buying and selling for nearly a month respectively.

In terms of industry, the energy, health care and utilities sectors led the gains during the week, up 4.55%, 6.87% and 2.40%, respectively. The rising international crude oil prices, both independence and growth, and defense are the driving factors driving the sustained rise of these three sectors. The Sino-Thai international strategy portfolio has benefited from quality factors, and the cumulative income has further increased.

China's capital market has taken an important step in opening up to the outside world

In the semiannual index review, MSCI proposed that 302 listed companies will be added to the global standard index of China after the close of trading at the end of May, and the old companies will not be excluded. Of these, 234 Chinese A-share companies will be included in standardized regional and global indices with 2.5% of their market capitalization adjusted for foreign investment. The weight of newly included A-share companies is equivalent to 1.26% and 0.39% of the current MSCI China and emerging market indices, respectively. Further, in the review in August 2018, the proportion of A-share companies included in the MSCI global standard index will be increased from 2.5 per cent to 5 per cent adjusted for foreign capital.

We thinkThe expansion of MSCI is an important step in the process of opening China's capital market to the outside world.First, the substantial expansion of constituent stocks, especially the inclusion of listed companies in mainland China, will greatly enhance the representativeness and allocation ability of the MSCI index to the Chinese economy. As of the end of April, the MSCI China Index consists of 153 stocks mainly concentrated in information technology and financial stocks listed in Hong Kong. The more than 300 newly listed Chinese companies listed in mainland China, Hong Kong and the United States will quickly make up for the lack of market capitalization and industry coverage of the MSCI China Index, and enhance the willingness and initiative of overseas investors to allocate the Chinese economy. Second, it will significantly boost the allocation of international stock capital to China's economy. At present, the shares of Chinese companies account for about 3.65% and 30% of the emerging market index and the global index, respectively, which is extremely disproportionate to the size of the Chinese economy in the global economy.

Calculated on the basis of public funds tracking the MSCI China and emerging markets indices on May 18, the size of the relevant China allocation will increase by $22 and $4.5 billion in this round of MSCI adjustments in June and August. In the medium to long term, a further increase in China's weight will lead to a larger demand for international capital allocation. Third, the role of the Hong Kong market as a hub connecting mainland China and the international market is on the rise. As the mainland capital market is difficult to fully open in the medium term, the interconnection mechanism between the Chinese and Hong Kong capital markets has become the main channel for the international capital allocation of the Chinese mainland market and the global allocation of Chinese capital. Hong Kong securities companies, especially Chinese-funded securities, are facing a new round of development opportunities.

China's demand for opening up to the outside world and system construction are promoted simultaneously.

According to the joint statement issued by China and the United States on economic and trade consultations issued by China's Xinhua News Agency on May 20, China and the United States reached a four-point phased agreement. First, "the two sides agreed to take effective measures to substantially reduce the US trade deficit in goods with China." Second, "the two sides agreed to meaningfully increase US agricultural products and energy exports." Third, "China will promote the revision of relevant laws and regulations, including the Patent Law." Fourth, "the two sides agreed to encourage two-way investment and will strive to create a level playing field for business." Fifth, the two sides reached a consensus on creating favorable conditions to expand trade in manufacturing products and services.

We believe that the outcome of this negotiation has partially dispelled market concerns about the escalation of US protective trade barriers (tariffs and bans) and increased pressure on Chinese exports. China's imports of energy and agricultural products, as well as external barriers to the domestic market are expected to be reduced, the industry is open, and intellectual property protection is expected to be enhanced. Overall, expanding imports will significantly reduce the long-term price gap between domestic and foreign raw materials and reduce the cost of raw materials in the industrial sector, but it will increase the level of competition in industrial manufactured goods and tradable service industries. Consumption upgrading and expansion of the residential sector are facing more positive factors, competitive science and technology growth companies are expected to get a better business environment, and the theme of import substitution will shift from simple replication to more reliance on medium-and long-term R & D investment. Putting aside the short-term political game factors, from the perspective of long-term changes in international economic and financial relations, we believe that China's economy is changing from relying on resource endowments and exporting middle-and low-end manufactured goods and excess capital to technological upgrading, exporting market demand and financial credit. This transformation process will not only face more constraints from technical, financial and institutional construction, but also put forward higher requirements for capital allocation.