Source: Everyone is excited, minority investors

Author: Everyone is excited

1. Wrong attribution brings wrong experience

Hegel said, “The only lesson humans can learn from history is that humans can't learn any lessons from history.”

But taking lessons, especially from our failures, may be the only way we can improve. The philosopher said this just to remind us --Summarizing the experience correctly is more difficult than we thought.

A few days ago, a friend asked me, “I bought two funds recommended by the platform at the beginning of the year, saying that the yield has been very good for the past ten years or so, but both have gone bad this year. Do you think it's a false advertisement for the platform? Or is the fund thing really risky?”

I can only comfort him. This year was indeed a relatively “bad” year, and many star fund managers with excellent long-term performance have fallen. It's not surprising if this phenomenon has been invested for a long time; it has happened before — but for new citizens, finding the reason and summing up the experience is not an easy task.

After failure, we first have to think about “finding” the reason. In fact, the human mindset “guesses” the reason:

Step 1: Intuitively guess a reason

Step 2: Use some methods to verify it

Whether it's a philosopher or an ordinary person,First, there is intuition. The difference is whether the second step has a scientific method. Let's first take a look at how ordinary people “guess” the reason.

2. The three instincts of ordinary people

There are three most common instinctive reactions to losing money when you see a celebrity fund bought in an advertisement:

Intuitive reaction 1: Any celebrity fund manager, any past performance, is deceptive in advertising.

When ordinary people verify this intuition, they use an internal logic that they take for granted:

If you're a star fund manager, your performance should always be good; if your past performance was good, you should still be good now. So, this is false advertising, fake celebrity fund managers, fake past performance.

If I were to sum up the experience from this instinctive reason, it would be — you can't trust advertisements when you buy funds; next time you choose your own.

Isn't that the right experience? If you only choose funds based on performance, it is likely that these people who chose them — Hegel — won.

Intuitive reaction 2: It's too difficult for funds to make money; let's honestly buy wealth management products.

The underlying logic is: Star fund managers are nothing more than that; buying other funds is even less reliable.

This logic doesn't stand up to scrutiny at all. The earnings of star fund managers this year were below average, but overall they weren't that bad. Even if they bought at the highest point before the Spring Festival, up to now, 30% of funds are profitable.

The conclusion that came to was “you can't buy funds”, which may be a good thing, but it's definitely not about experience — Hegel won again.

Intuitive reaction 3: This group of fund manager grandchildren defrauded people of money, acted as a hoarder for mice, and did not do personnel work...

Internal logic, isn't it just the same as what the teacher thought back then? My grades have regressed; I must be proud and complacent, mischievous and playful; anyway, my mind must have declined.

There's nothing to refine in this logic; it's just emotional venting, it's all a loss of money; can't you just say a few words of curse?

The premise of learning from experience is to find the reason. The prerequisite for finding the reason is to know what are the most likely causes, and to know these, you have to have experience first — this became a dead cycle, and that is why Hegel was so straightforward and strong.

To solve this problem, we first need to break out of this dead cycle and see how professionals analyze this problem.

III. Professional intuition

As an unknown fund manager, of course, I always have to study the positions, performance, and opinions of star fund managers, so the first reason that comes to mind is --

The market style is wrong, this is the professional's first instinctive reaction

The intrinsic logic of this intuition is that investment is an industry where half of the food is eaten by the sun. If the market style is wrong, it's like farmers encounter a natural disaster and when food prices are cheap after harvesting, even the hardest farmers will lose money.

But isn't that the right idea? You can check whether this fund manager's style is the opposite of this year's market style. Of course, you need to know: What is a market style? What are the market styles? What is the fund manager's market style? How to determine whether market styles are the same, opposite, or unrelated?

This verification is a bit difficult for ordinary investors. If it's just financial management, the intention is that they don't want to spend too much time; many people definitely don't want to sum up such professional experience. Furthermore, the explanation for this reason is limited. Some people's style is not that strong, and some people also adjust the style's adaptability.

So are there any reasons that are more suitable for ordinary people to judge?

Professional Intuition 2: Increased scale causes investment methods to fail

The intrinsic logic of this intuition is that smaller funds have more ways to obtain excess income (of course, the risk is greater), and people like to buy funds whose performance rankings have risen rapidly recently. As a result, after the performance of small-scale funds has improved, their scale quickly grew and their performance deteriorated.

This intuition is relatively easy to verify. Just take a look to see if the fund's size increased more than fivefold last year? Is the style of adjusting positions and being quick to catch up with hot spots?

Professional Intuition #3: The Fund Manager's Investment Method Is Outdated

This is an issue I'm more concerned about. Investment is an industry whose methodology is changing very fast. There were countless star fund managers who were eliminated in the past because they couldn't keep up with the times, and failure will always be a better source of useful experience than success.

Other than that, there are a few less common reasons. For example:

The fund manager changed

Heavy stocks have been bombarded continuously

The company's research team has undergone major changes

...

Even the instincts of ordinary people mentioned earlier, fund managers don't work hard, which may be one of the reasons. Now some star fund managers spend a lot of time on marketing, have a large number of funds under their name, and are also responsible for many administrative matters.

So, with so many listed above, how can you find the most important reason?

I'm very sorry,Proving the causal relationship between two things is much harder than finding a bunch of reasons, or even a “causal relationship” may not exist naturally.

However,We need to know the “why”; we don't really want to know the reason, but rather that we can do better ourselves. There are more important things than “finding the reason” in summing up our experiences.

IV. The four levels of the methodological framework

The important purpose of learning from experience is to hope to update our methodological framework, so in addition to the two steps mentioned above, there are three more important steps to learning from experience:

The first step is to intuitively guess a reason

Step 2. Use some methods to verify it

Step 3. Refine your methodological framework

Being able to have and be proficient in using one's own “methodological framework” is the essential difference between professionals and non-professionalsJust like you can check your illness and what medicine you should take online, but only a doctor can use a methodological framework to see you.

All of the “whys” analyzed earlier must fit into this framework before they can be used by you.

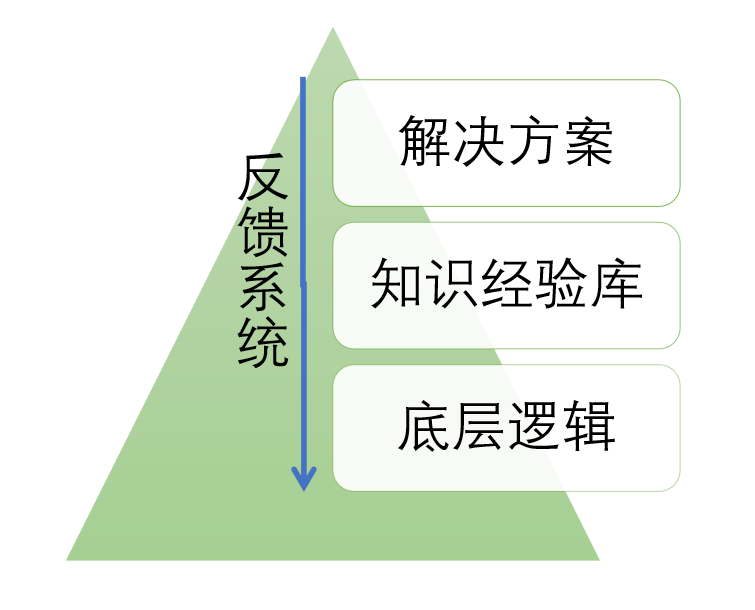

The professional's methodological framework includes four levels:

The first layer: the underlying logic

The definition of this layer is the core question of direction: if you are a public account operator, do you focus on traffic management or self-media brand development? If you're a fund manager, do you get more from long-term earnings or short-term stock price fluctuations? Do you want to develop in a professional direction or in management?

The underlying logic should be very stable to distinguish which experiences are more valuable to you, what angle do you prefer to analyze experience from.

Second level: knowledge and experience base

Knowledge and experience verified by underlying logic are stored here, just like a warehouse, through continuous classification and sorting, so that it can be verified with reality at any timeJust as experienced teachers have their own “teaching experience bank”, every knowledge point is a reserve of mistakes that students are likely to make, even classic question types.

The professionalism of professionals depends partly on the richness of this library, while the other part depends on the proficiency of access, or “solutions.”

Tier 3: Solution

If I want to get things right, including the three aspects of “perception, decision, and execution”, I summarized them in an article “Color Cognition, Black and White Decisions, and Grayscale Execution”The requirements for professionals go a step further and require the formation of analytical models, decision-making models, and action models.

Fourth layer: feedback system

This level is actually a review method. Through sorting through the results and traceability of “causal relationships”, the “underlying logic, knowledge base, and solutions” are continuously revisedThis is exactly what this article is about.

So, be curious, ask more questions about why, and not satisfied with existing explanations. The process of summing up experience is more like a mental training, in order for our “methodological framework” to be more structured, richer in content, and more adaptable to the ever-changing reality environment.

So let's go back and see what kind of upgrades the previous analysis can bring to our methodological framework.

V. Upgrading the methodological framework

One upgrade of the general fund investor methodological framework: the performance of half a year or a year was poor or even very poor, and did not affect long-term returns.

It's easy to prove this. If you take a look at these star fund managers who have performed brilliantly in the past, you'll know if there have been any years with poor performance before.

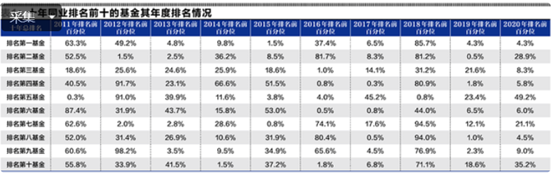

Some people counted all 398 active stock public funds established before 2011. After ranking each year in the past ten years, they found that:

Only one fund ranks in the top 50% each year(It's not intuitive, but it's easy to understand from a probabilistic point of view), but its overall ranking is only third;

The fund with the highest total return ranked below 50% in two years, and the worst year ranked 85%;

The second-ranked fund ranked below 50% in three years, and the worst two years ranked 81%;

The fourth and fifth largest funds ranked 91% in one year;

The ninth largest fund actually ranked 98% of the total market in 2012.

If they are eliminated in the last 20% according to the regulations of many companies, eight of the ten most powerful fund managers in China will be violently expelled.

Most importantly, the year after receiving an extremely poor performance of ranking 80% 9 times, it was within 10% 8 times, and the worst score was 31.9%. The conclusion is:Fund managers with good long-term performance are likely to perform very well in the year after experiencing extremely poor performance — this should be related to a reversal in market style; of course, more data verification is needed.

Investments rely on long-term compound interest rather than short-term profiteering——This experience corresponds to the underlying logic of investment theory.

This isn't necessarily the only right way to invest, but in my opinion, it's the best method for non-professional investors.

Second upgrade to the general fund investor methodological framework:Choosing a fund manager should suit your investment cycle and match your personal expected returns.

This knowledge and experience corresponds to the third level of “solutions”: If you have a new sum of money, you first need to analyze when it will be used in the future and what is your reasonable expected return to determine the most suitable financial management channel for it, not the higher the profit the better, or the safer the better.

Additionally, the previous analysis had a few updates to the “experience bank”:

Avoid funds that have skyrocketed to more than 1 billion dollars due to excellent short-term performance;

If you don't like big withdrawals, avoid funds with a style that is too obvious;

Avoid star fund managers who manage too many funds, hold too many executive positions, or have too much exposure;

...

6. The Two Stages of Professional Competence Building

Finally, I want to answer the dead cycle question at the beginning: “The premise of learning from experience is to find the reason. The prerequisite for finding the reason is to know what are the most likely reasons, and to know these, you have to have experience...”

A person's professional competence is usually built like this:

In the beginning, it's easy for you to master a lot of new knowledge and experience through causal relationships, but because of the lack of a professional framework, your professional ability appears insufficient.The most important task at this stage is to first develop the easiest professional framework that can be used. As for whether it is good or not, it doesn't matter.

After a certain period of time, it became more and more difficult for you to get more clear causal relationships, and you became more and more in awe of your profession. However, once you have a professional framework, it is relatively easier to get some experience that is likely to be correct, and continuously revise and enrich your professional framework to obtain professional problem-solving skills.

Editor/jayden