If ten years are a reincarnation, then the development of China's insurtech industry also happens to be at the end of such a cycle; it is also a new beginning.

In fact, the “encounter” between insurance and technology in China has been around for no less than 40 years, but the development of insurance technology in China did not really begin until 2013.

Back then, one of the most iconic events was the opening of Zhongan Insurance, the “first Internet insurance company in China” formed by Ping An, Tencent, and Alibaba.

From that year on, there was an explosion in the number of domestic professional insurtech companies.

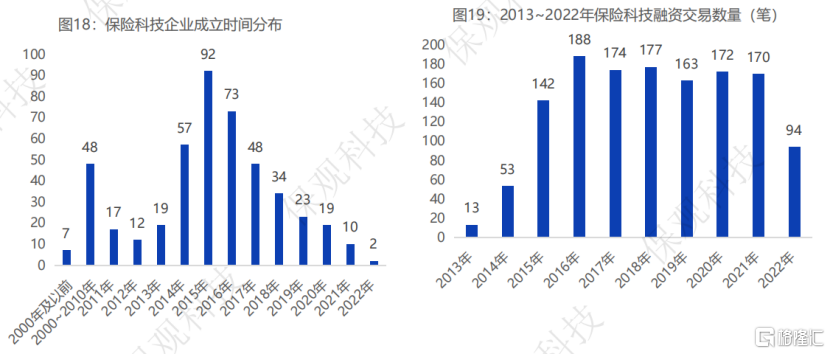

According to industry media, watch the latest releases“A Ten-Year Review and Prospects of China's Insurance Technology”According to the report (hereinafter referred to as the “Report”), 2014-2016 was the peak period for the establishment of insurtech companies. Of the companies that received investment according to the report statistics, 222 were established at this stage.

At the same time, the report points out that since 2015, the activity of investment and financing activities on the insurance technology circuit has increased markedly, and has remained high for many years. The number of transactions reached 142 that year, an increase of nearly 168% over the previous year.

(Source: Watch the “Ten-Year Review and Prospects of China's Insurance Technology” published in May)

It is worth mentioning that at this time, traditional insurers have also reached a point where changes are urgently needed.

In 2014, the domestic interest rate marketization reform accelerated, leading to a narrowing of interest spreads and an increase in credit premiums. Coupled with the loosening of regulations on the investment side, competition in the entire asset management industry intensified, and it was difficult for insurers to gain an absolute advantage in yield. The original model was impacted, especially in terms of yield and channels. For insurers, it is necessary to make adjustments and innovations in various areas, including investment, product structure, and channels.

Therefore, a number of leading traditional insurance companies have also “touched the Internet” one after another and cooperated with Internet platforms, setting off a trend of digital transformation in the traditional insurance industry. For example, in 2013, Taikang Life Insurance and Taobao launched the Internet life insurance platform “Leye Insurance” to provide insured life insurance products for Taobao sellers.

In fact, 2013 was also the first year of internet finance - Alibaba's “Yubao”, Tencent's “WeChat Pay”, and JD's “Beijing Baobai” were also launched one after another, opening the curtain on the rapid growth, integration, and market education of Internet finance.

Looking at it now, the rise of internet finance has touched almost all fields of the financial industry except insurance, and has provided a favorable technological and market environment for the digital transformation of traditional institutions. In other words, this ten-year history of insurance technology development is also a brief history of the digital transformation of the financial industry.

The “Report” points out that at the beginning of its establishment, Zhongan Insurance chose the “digital” route, opening up the application of technology in all aspects of insurance before, in the middle, and back office. Zhongan has also integrated with the new Internet ecosystem such as e-commerce and OTA to develop a series of innovative insurance products and services that meet market needs, such as popular products such as return shipping insurance and one-million medical insurance, expanding the coverage of risk protection scenarios and injecting fresh blood into the industry with distinct characteristics of the times.

Ten years of “butterfly transformation”, the future can still be expected

Over the past ten years, the development of the insurance technology industry has gradually moved from an early stage to maturity, and the market size has also developed by leaps and bounds. According to statistics from the China Insurance Industry Association, in 2013-2022, the number of enterprises carrying out internet insurance business has grown from 60 to 129, and the premium scale of internet insurance has increased from 29 billion yuan to 478.25 billion yuan, with a compound annual growth rate of 32.3%.

From the perspective of penetration rate, the penetration rate of China's Internet insurance market ranged from 2% in 2013 to 6.4% in 2020. Some organizations expect that the Internet insurance penetration rate is expected to exceed 10% in 2023, which means that the potential for future improvement should not be underestimated.

Looking at overseas markets, the insurtech industry has also shown a booming trend in ten years, and its business models have become more diversified. According to statistics from the CICC Report, the amount of global insurance technology financing in 2015 jumped from the previous scale of 2-4 billion US dollars per year to the level of 2 to 4 billion US dollars since then.

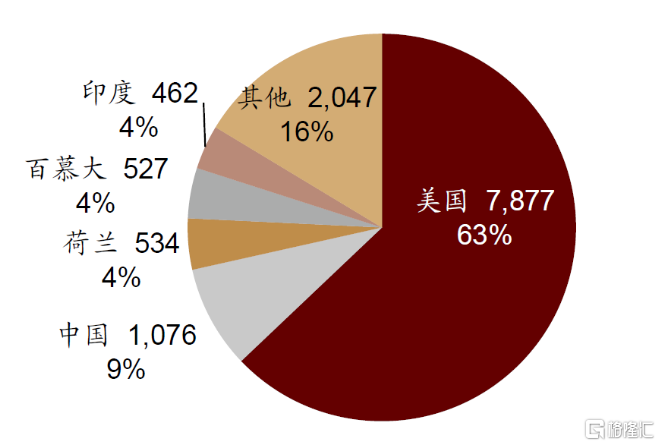

Among them, the US is the central location for overseas insurance technology investment and financing. According to statistics from MILKEN (a non-profit economic think tank), in the first half of 1998-2018, the country's insurtech companies accounted for 63% of the world's financing, and the number of newly established insurtech companies accounted for 51%.

In 1998-2018H1, US insurtech companies accounted for 63% of global financing

(Source: CICC's “Overseas Insurtech Industry Is in Full Bloom, Different from “China”)

In terms of penetration rate, the development of China and the US is basically close (according to Statista, the penetration rate of US internet insurance in 2019 was 7.2%); however, regardless of the depth of insurance or the density of insurance, China is still far below the US, and there is even a certain gap with the global market average.

(Source: National Bureau of Statistics, Banking Insurance Regulatory Commission, Forward-looking Industry Research Institute)

In addition to this, in terms of the absolute size of premiums, China also has a significant gap compared to it. According to statistics, in 2022, life insurance premiums were 1142.7 billion US dollars, and financial insurance premium income was 864.1 billion US dollars, all far higher than China's life insurance premiums of 3209.1 billion yuan and financial insurance premiums of 1486.7 billion yuan during the same period.

Since the application of technology is inseparable from the industrial base, the lower depth, density, and scale of insurance have all fundamentally determined the gap in the development of insurance technology between China and foreign countries. Of course, this also once again reflects the future market potential of China's insurance technology.

Comparisons and Implications between China and Foreign Countries

In view of the above, model diversity is a reflection of the relative advantage of insurance technology development in mature overseas markets represented by the US. Take the insurance technology companies listed above as an example. According to incomplete statistics, the current business is mainly internet insurance sales and insurance companies. In addition, it also includes other categories such as health services and technical services. Among them, American companies account for the vast majority and cover various categories, such as China's Zhongan Online (HKG:6060) and Huize (NASDAQ: HUIZ),Water Droplets (NYSE: WDH)The three companies are represented. They mainly carry out businesses such as internet insurance sales, etc., and the categories are still relatively uniform.

CICC believes that differences in the business environment, stage of development, and regulatory policies are the main factors leading to these differences. Looking at the medium term, the development stage will gradually mature, and changes in regulatory policies in specific fields will be the main driving force for China to bridge the model diversity gap with the US, while the business environment will be more difficult to change.

In addition to the model, there are also significant differences in the development paths of China and abroad.

Still taking the US as an example, according to industry analysts, its insurtech companies usually start as technology companies to quickly obtain financing and build up a technological base. After the products are verified by the market and supported by sufficient capital, they acquire insurance companies, obtain insurance licenses, and then go public for financing, such as Root, MetroMile, etc. The development of insurance technology in China, although “different” such as Zhongan Online, may rely more on the independent R&D of insurance companies that have a relatively monopoly position, independent insurance technology innovation enterprises, or help insurance companies develop customer acquisition marketing based on their traffic and scenario advantages, gain a certain dominant position, or export technological capabilities and system platforms to insurance companies.

Overall, objectively, there is still a big gap between Chinese and foreign innovation in the field of insurance technology. This may be due to differences in economic development models, industrial patterns, and regulatory policies between the two countries.

Despite the differences, there is no shortage of consensus.

First, the trend of integration with physical industries is intensifying. Whether in the fields of medical technology and services, big data risk control, the Internet of Things, agricultural technology, automotive technology and services, insurance technology will be deeply connected to various other industries. Through the integration of data and technology, the insurance industry will be strongly empowered, and the “fintech” attributes of insurance technology will gradually weaken as a result.

Second, support for financial insurance and health insurance is more promising. According to statistics from the report, currently 60% of global insurance technology investment goes to property and accident insurance, and the other 40% goes to life and health insurance.

Furthermore, Baoguan pointed out in the report that it is expected that insurance technology will experience a transformation from application to basic development and from shallow technology to high-end technology in the future. For related companies, this also means combining technical capabilities and business models to build a real moat.

AIGC may be a new “engine” -- triggering a new round of productivity change, and insurance technology is no exception. Some industry media even called it “a new 'fork in the road' for the development of internet insurance. In response, Zhongan Insurance and Zhongan Technology have invested in research and practical exploration of this new technology.

What are the opportunities in the next ten years?

In fact, as mentioned in the opening article, there are many signs that China's insurtech industry is at a “crossing of a storm.”

In addition to technological change ushering in a critical inflection point, policies, consumption habits, etc. are also developing in a more favorable direction.

Policy side, end of 2021“The 14th Five-Year Plan for the Development of Insurance Technology”It was announced that 2022 will be the beginning year of implementation of the industry's “14th Five-Year Plan” development policy, and the goals, schedule and road map for the future development of the industry have been clarified from the top-level design level.

At the consumption level, some recent reports and statistics show that post-80s people have become the “mainstay” of insurance consumption, far exceeding consumers of other age groups in terms of insurance spending. Of these, 75% of families spend more than 5,000 yuan on annual insurance. Also, they prefer internet channels to buy insurance.

(Source: China Insurance and Pension Research Center, Wudaokou School of Finance, Tsinghua University, and the Internet insurance technology platform Yuanbao jointly released the “2022 China Internet Insurance Consumer Insights Report”)

In addition, the “Report” also mentions several major trends in the development of the industry:

First, the industry is expected to usher in a new growth cycle. The “Report” study found that the epidemic has had a positive impact on consumers' overall insurance purchasing awareness and decisions. Consumers' future insurance spending budgets are expected to be higher. The report predicts that consumers with an annual household insurance budget of 10,000 yuan or more will rise to more than 40% in the next year.

Second, the Internet will become the main channel for purchasing insurance, and the entire insurance business process will gradually become online and intelligent.

ChatGPT has sparked a new round of technological revolution with AICG as the main line. The digital level of the insurance industry will also use this to enter a new era, and achieve a new leap forward in insurance value chain restructuring and user experience is becoming an industry consensus.

In this context, recently, Zhongan Insurance and Zhongan Technology jointly released the first AIGC application white paper in the domestic insurance industry“AIGC/ChatGPT Insurance Industry Application White Paper”(“White Paper”) provides a guide for the industry to explore AIGC applications.

According to information, through expert research, the “white paper” sorts out more than 30 specific implementable application links of this technology in the insurance field (including full link links such as product design, actuarial, marketing, operation, and customer service) and AIGC scenario applications, and predicts the feasibility of implementing the technology in application scenarios from multiple dimensions. At the same time, a number of domestic and foreign technical standards research and overall analysis of government systems, investment and financing markets were compiled, and the application exploration of Zhongan in this technology field was brought together.

As we all know, opportunities and challenges coexist.

Objectively speaking, the application of this technology has attracted widespread attention in the domestic insurance industry. The “White Paper” points out that although AIGC technology still faces many challenges in large-scale commercial applications in the insurance industry, the technology is still expected to become an important strategic tool for insurance institutions to win the future.

Major technological changes often harbor historic opportunities, and they also mean exponential risks. Even for excellent companies, this is evident in the rapidly changing technology industry.

So, as one boss said, “If you can't see, look down on, or understand opportunities, the future will fall short.” This scene will be more extreme in the current context of the “emergence” of big models, the failure of Moore's Law, and global tech giants racing to “compromise”.

On the other hand, those visionary “activists” will have more opportunities to get “tickets” to a new round of change, thus embarking on a new “sweet” journey.