Source: Wall Street News

Author: Wu You

On the evening of May 24, Xiaopeng Motor, one of the three former new car builders, announced its results for the first quarter of 2023.

Looking at key indicators overall, Xiaopeng's operating income reached 4.03 billion yuan in the first quarter of this year, a year-on-year decrease of 45.9%, a decrease of 21.5% over the previous year; operating losses continued to expand to 2.34 billion yuan, an increase of 37.4% over the previous year, a slight decrease of 1% over the previous month; gross margin fell sharply to 1.7%, down 10.5 percentage points from the 12.22% gross margin level in the same period last year, while the gross margin of 8.7% in the fourth quarter of last year was reduced by 7 percentage points.

According to Wall Street news and insight research, Xiaopeng's sales level in the first quarter of this year was not as good as expected due to the unsuccessful release of the new model G9 in the early stages and the painful period brought about by the subsequent remodeling and launch of the old model. In order to meet the price war brought about by Tesla's pioneering price reduction, Xiaopeng's unavoidable price reduction strategy also caused overall revenue and gross margin levels to be low. It can be seen that Xiaopeng is still quite far from turning back against the wind. It is still necessary for subsequent remodeled models to quickly recover the situation.

Looking at it now, the response of Xiaopeng's first facelifted P7i after it was released in March has been quite good. It has led to a slight recovery in sales, and whether the recovery trend can be maintained in the next few quarters will be a top priority for Xiaopeng to return to its peak next.

1. Sales continue to be sluggish, and it is necessary to give time to remodel models to recover the situation

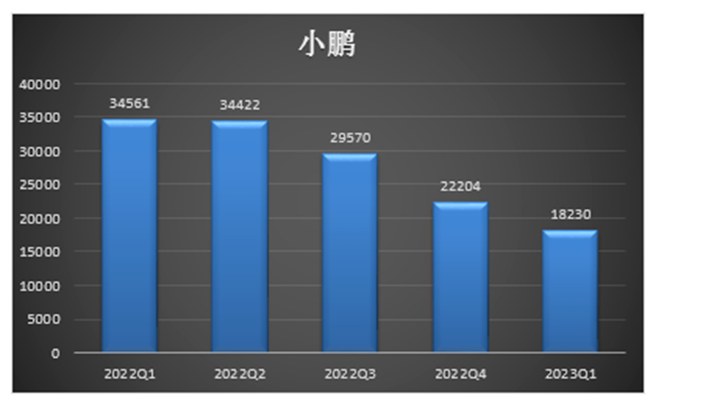

Xiaopeng's sluggish sales have now become an absolute problem. Following product sales in the fourth quarter of last year, which was the lowest level for the whole year, Xiaopeng continued to decline in the first quarter of this year. Although it was still within the previous first-quarter sales guide range of 18,000 to 19,000 units, which barely met expectations, the overall sales volume was only 18,000 units. This is already the 5th consecutive quarter where Xiaopeng's sales have declined month-on-month.

If Xiaopeng's sales continued to decline year-on-year due to seasonal factors during the peak season of the automobile market and the temporary “minor illness” that occurred after facing the impact of NEV subsidies at the end of the year (Xiaopeng's sales in the first quarter fell 18% month-on-month, and the year-on-year growth rate fell to -48%, close to a slump), then the sharp decline over the previous year was really a “major illness” caused by poor alternation between new and old Xiaopeng and modified models and falling demand.

Moreover, according to Xiaopeng's sales guidelines for the second quarter of this year, the company expects car deliveries in the second quarter to be 21,000 to 22,000 units. Considering that Xiaopeng's sales volume in April reached 70,000 units, which is equivalent to the average monthly delivery in May and June remaining below 10,000 vehicles, it can be seen that Xiaopeng still has a long way to go to return to sales and break the 10,000 mark.

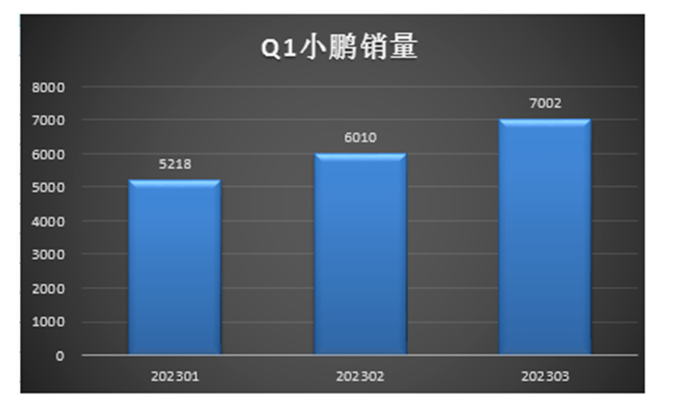

Of course, looking at the positive side, although Xiaopeng's monthly sales have been slow and difficult to return to the level of 10,000 units, each month alone is still slowly recovering month-on-month (sales volume from January to March was 520,000 units, 60,000 units, and 70,000 units, respectively), unlike NIO's sales in March and April, which once again experienced a continuous negative month-on-month increase.

Furthermore, with the launch of Xiaopeng's main model, the revised P7i, in March and the rapid commencement of delivery, Xiaopeng's total delivery volume of P7 models reached 3,030 units in March of this year, accounting for nearly half of total sales, an increase of 32% over the previous month. It can be seen that the market and consumers have given some recognition to Xiaopeng's former flagship model.

However, in the second half of this year, whether the remodeled models of Xiaopeng's other old models, such as the P5 and G3, can help Xiaopeng's sales quickly pick up, thereby regaining the attention of the market and consumers is a top priority for Xiaopeng to return to its peak next.

2. Forced to face a price war, Xiaopeng's gross margin space was extremely compressed

As a result of being forced to face a price war in the first quarter, Xiaopeng's bicycle revenue level fell below the 200,000 yuan mark, reaching 193,000 yuan in the first quarter of this year. The previous plan to raise bike revenue through the new G9, a high-priced model, was obviously not realized. Fortunately, bicycle revenue did not decline in a cliff-style manner due to poor overall sales and poor release of the new model G9. Overall, bicycle revenue has returned to the level of Xiaopeng in the first half of 2020.

In addition to this, Xiaopeng's gross margin level was also affected quite a bit. In the first quarter of this year, Xiaopeng's overall gross margin plummeted to 1.7%, down 10.5 percentage points from the previous year. Continuing to stay below 10%, there was no improvement, while automobile gross margin fell to a negative figure of -2.5%. This is the first time in the past three years that Xiaopeng's gross margin was negative. In other words, a negative car margin meant that Xiaopeng lost money throughout the first quarter.

According to Wall Street news and insight research, the price reduction strategy implemented by Xiaopeng in response to Tesla's price war in the first quarter of this year (guide prices for Xiaopeng's P7, G3, and P5 models ranged from 20,000 yuan to 36,000 yuan respectively) still reduced Xiaopeng's own gross margin space.

Although it is true that the prices of upstream raw materials, especially the price of lithium carbonate, also declined in the first quarter, it is difficult for the cost decline to be as large as the spot price of battery-grade lithium carbonate due to factors such as the price of Changxie. There must have been some delay.

In addition to this, even if you look at the decline in the spot price of battery-grade lithium carbonate (the price of battery-grade lithium carbonate fell from 520,000 yuan/ton at the beginning of the first quarter to 245,000 yuan/ton at the end of the first quarter, a decline of 52.9%), the cost of Xiaopeng's main model, the P7 (80 kilowatt hour), will fall by about 15,000 yuan, which is still lower than the decline in the price of Xiaopeng's own products.

3. Xiaopeng is far from making real money

Xiaopeng's net loss in the first quarter of this year reached 2.34 billion yuan, an increase of 37.4% over the previous year. There is still quite a gap between achieving break-even. At the same time, although Xiaopeng's cash reserves were still in a good state, the rate of money burning increased. In the first quarter of this year, Xiaopeng's cash and cash-like asset reserves were 34.12 billion yuan. In comparison, Xiaopeng's cash reserves for the fourth quarter of last year were 38.25 billion yuan, a decrease of 4.13 billion yuan, while the previous single-quarter level of money burning was around 2 billion yuan to 2.5 billion yuan.

Among them, the main direction of money burning is to increase investment intelligently, while the rapid expansion of the sales network and the reduction in investment in advertising have been reduced. However, these are all rigid expenses, and it is difficult to continue to reduce them in a short period of time. In the first quarter of this year, Xiaopeng's R&D expenses reached 1.3 billion yuan, an increase of 6.1% over the previous year, accounting for 32.3% of total revenue; while sales expenses reached 1.39 billion yuan, a decrease of 15.5% over the previous year, accounting for 34.6% of total revenue.

By the end of the first quarter of this year, Xiaopeng's number of stores reached 425, an increase of 5, and the city coverage reached 145, an increase of 2. Precisely because these rigid expenses are difficult to be quickly amortized and diluted, Xiaopeng's overall profit has also been suppressed to a certain extent.

Editor/jayden