Author: home Appliances team of Tianfeng Securities Research Institute

After the event that the control of Gree Electric Appliances is to be transferred, how many times should the reasonable valuation level of Gree Electric Appliances and Midea become a hot topic in the market? is there a valuation discount when Gree Electric Appliances is more beautiful?

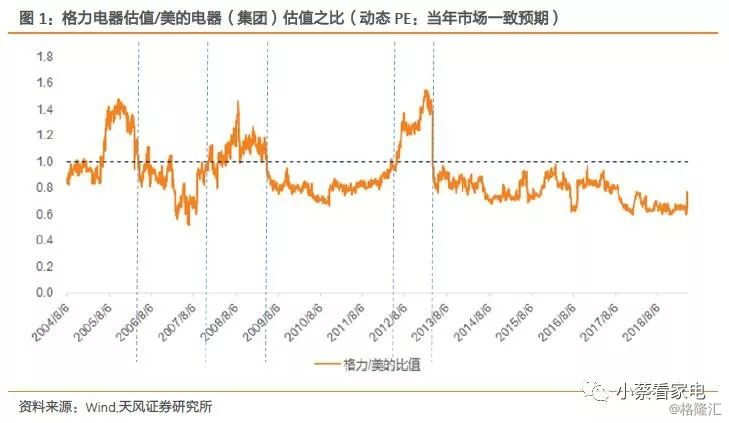

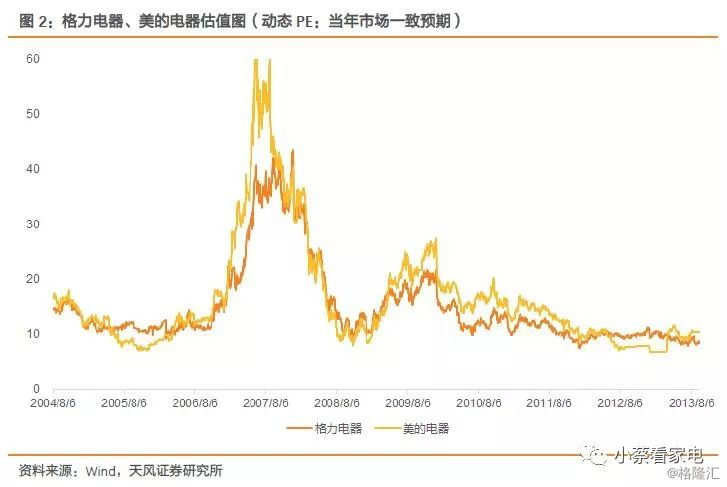

We divide the valuation of Gree Electric Appliances (Group) by the valuation of Midea Electric Appliances (Group) and get a ratio. A value greater than 1 indicates a valuation premium compared to Mei, and a valuation premium less than 1 indicates that there is a valuation premium between Gree and Gree.The most important thing to clarify is thatHistorically, Gree's valuation has not always been discounted compared with Mei's, and Gree's valuation has been higher than Midea's in at least three periods.

According to the relative valuation of Midea and Gree, we divide the period from 2005 to 2019 into six stages.

Phase I May 2005-April 2006:

Gree's high performance growth brings valuation premium

From May 2005 to April 2006, Gree Electric Appliances was valued higher than Midea Electric Appliances. We believe that Gree Electric Appliances has a higher valuation mainly because the market expects the subsequent growth of Gree Electric Appliances to be better than Midea Electric Appliances.

Phase II 2006-2007:Midea's valuation premium

The reason is that the imagination of industrial diversification is better.

We discuss the factors that may affect the valuation of the company during this period. From the perspective of ownership structure, both sides have marginal improvement, and it is difficult for state-owned enterprises and family enterprises to demonstrate which corporate governance structure is more perfect at that time. After all, there are also cases in which major shareholders of family enterprises hollowed out listed companies; from the perspective of management incentives, Gree and Midea both launched management incentive programs. therefore,We believe that at this time, there is a large valuation difference between the two companies, the focus is not on corporate governance, but more onIn the context of the bull market, the market believes that diversified companies in the industry have higher room for growth.

1) ownership structure: Midea does addition and Gree does subtraction, but they are all marginal improvements.

During the non-tradable share structure reform in 2006, both Midea Electric and Gree Electric Appliances changed the shareholding ratio of major shareholders, although the shareholding of the two companies changed in opposite directions.But it can be understood as the further optimization of corporate governance.

Midea increased his stake in Midea Electric Appliances:From March to May 2006, Mei Electric's major shareholders increased their shareholding in Midea Electric Appliances from 24% to 50.2%, ensuring the group's absolute control over Midea Electric Appliances. Midea's interests are more consistent with those of Midea Electric Appliances. At the same time, it also prevents hostile takeovers in the secondary market in the era of full circulation.

Gree Group reduces the holding of Gree Electric Appliances:Gree's stake in Gree Electric Appliances fell from 50.28% disclosed in the 2005 annual report to 42.16% in 2016.

2) introduce new shareholders: each has its own advantages

From 2006 to 2007, both Midea and Gree chose to introduce new shareholders to provide more support for the company's development. Midea chose Goldman Sachs Group (later denied by the CSRC), intended to improve corporate governance and internationalization, Gree chose to introduce dealers, binding deeper interests.

Midea Electric Appliances: try to introduce international shareholders and industrial capital.In late November 2006, the company made great progress in introducing strategic investors and planned to issue new shares to Goldman Sachs Group, accounting for 10.71% of the total share capital, which is not only conducive to the internationalization of the company's capital. the more important significance is to introduce the advanced governance concepts and management experience of multinational corporations. On August 29th, the issuance Review Committee of China Securities Regulatory Commission examined and approved Midea Electric Appliance to The Goldman Sachs Group, Inc. The non-public offering plan of wholly-owned subsidiary GS Capital Partners Aurum Holdings, but the plan was not approved in the end.

At this time, Midea Electric Appliances has introduced Toshiba Kaili as an external shareholder in the air conditioning and compressor business, and the refrigerator and washing machine business has introduced Rongshida Group as an external shareholder. The introduction of external shareholders not only achieves the purpose of introducing technology, but also optimizes the shareholder structure of subordinate companies through external checks and balances, so as to improve corporate governance.

Gree Electric Appliances: bind the dealer.The company announced in April 2007 that Zhuhai Gree Group, a major shareholder of Gree Electric Appliances, transferred 10% of the total share capital to Hebei Jinghai guarantee Investment Co., Ltd., which is controlled by dealers, and tied up the interests of dealers with equity. The major shareholders of the company transferred part of their shares to dealers, and the property right structure was improved to a certain extent.

3) incentive mechanism: both parties provide equity incentives to the management.

In the context of the non-tradable share structure reform, the management of Gree Electric Appliances and Midea Electric Appliances began to obtain equity incentives, and both made clear goals for the company's performance assessment, which means that the interests of shareholders and management of the two companies have become more unified.

Management shareholding of Gree Electric Appliances

In December 2005, Gree Electric Appliance's share reform plan proposed that Gree Group should allocate 26.39 million shares from the shares held by Gree Group as the stock source of Gree's management equity incentive plan.In any year of 2005, 2006 and 2007, if the audited net profit of the company reaches the promised value for that year (the corresponding net profit for the above three years is 504.936 million yuan, 555.4296 million yuan and 610.9726 million yuan respectively), within 10 trading days after the announcement of the annual report for that year, Gree Group will sell 7.13 million shares to the management of the company based on the audited net asset value per share at the end of that year as the selling price. If the promised net profit is achieved in the above three years, the total number of shares sold to the management of the company is 21.39 million shares. The incentive plan for the remaining 5 million shares shall be formulated separately by the board of directors. The specific implementation plan of the management equity incentive plan shall be formulated by the Gree Electric Appliance Board in accordance with the relevant laws and regulations.

The 2005 annual results were announced on April 11, 2006. relying on an increase of more than 21.11% in net profit, its management incentive plan was realized in the first step. Zhuhai Gree Group sold 7.13 million shares to the company's management as promised.

Midea Electric Appliance put forward the draft equity incentive plan in November 2006.

In mid-November, the company launched a stock option incentive plan to issue 50 million additional shares to management, accounting for 7.93% of the total share capital. The exercise condition is that the growth rate of net profit is not less than 15%, and the weighted ROE in 2007 is not less than 12%, which demonstrates the company's confidence in the future. This measure aims to optimize the internal incentive and restraint mechanism, promote the management compensation system to be in line with international standards, and achieve the consistency of management interests with the interests of the company and shareholders.

4) the management level is the biggest difference between the two: the marginal change of beauty is greater than that of Gree.

First of all, Midea's air-conditioning field began to learn from Gree's sales company model.

Gree Electric Appliances established a regional sales company in Hubei as early as 1997, and later showed strong control ability in the "Gree Gome Breaking case" in 2004 with its perfect self-built channels.

When the bargaining power of home appliance chains is increasing day by day, Midea began to consider learning Gree's self-built channel model in the field of air conditioning in 2006. Midea air conditioners have set up joint venture sales companies, including Beijing, Shanghai, Hangzhou, Chongqing, Changsha, Wuhu and other cities. These joint venture sales companies have been in operation since September 2006.

More importantly, in addition to air conditioning, ice washing is injected into listed companies.

In November 2006, Midea intends to acquire the assets of Midea, a major shareholder:At a total price of 127 million yuan, Midea Electric Appliances intends to transfer 50% of the shares held directly or indirectly by Midea Co., Ltd. in Hefei Rongshida Laundry equipment Manufacturing Co., Ltd., Hefei Rongshida refrigerator Co., Ltd. And Hefei Rongshida Electrical Appliances Marketing Co., Ltd.; Midea's Rongshida ice washing assets were officially injected into the listed company in January 2007.

The market believes that in the next two to three years, Midea will continue to integrate household appliance assets and will become the focus of the capital market. Hualing refrigerators and air conditioners, large central air conditioners, motors, the remaining equity of Rongshida ice washing assets and small household appliances will all be potential integration targets.

Sure enough, in November 2007, Midea Electrical Appliances acquired shares in three major operating entities of Hualing Group from Midea:That is, Hefei Hualing, Guangzhou Hualing, China refrigerator. The purpose of the acquisition of Chongqing Meitong is to improve the central air conditioning product structure of listed companies and reduce the scale of daily related transactions.

In a bull market, the market prefers companies with room for growth.After the acquisition of major shareholders' ice-washing assets, the proportion of air-conditioning business in Midea's business structure fell from 85% in 2006 to 73% in 2007. The increase in the business of household appliances other than air-conditioning undoubtedly makes the market feel that there is more room for imagination in category expansion and growth than a single Gree appliance.

Phase III 2008-first half of 2009:

Gree operates more steadily, and the market gives a valuation premium.

The stock market in 2008 has opened the way to decline from the bull market, and the market focus has begun to change from the company's growth space to the company's healthy growth and anti-risk ability.

At this time, in February 2008, Mei Electric Appliances announced that it planned to transfer 87.67 million Little Swan A shares at 1.68 billion yuan, accounting for 24.01% of the total share capital of Little Swan. Since Midea had already bought 4.93% of B shares in the secondary market, it would hold 28.94% of Little Swan and become the largest shareholder.However, the general reaction of the market is that the purchase price is on the high side.The purchase price corresponds to the market capitalization of Little Swan in 7 billion, 31 times of PE in 2007, and more than 5 times of PB in 2007, with a premium of 400%. The diversification of the next city has not made the market willing to pay more premium for Midea.

In the market environment in 2008, Gree's profit growth appears to be healthier than Midea's. Affected by the financial crisis, Midea Appliances showed negative growth in the third quarter of 2008, and even a profit loss in the fourth quarter.Under the differences in fundamentals, the market has certainly given Gree, which is growing faster and more robust, a higher valuation premium.

In addition to Gree's better fundamentals, in early 2009, the cooperation between Gree and Daijin made Gree favored by the market.

In February 2009, Gree and Daijin announced the establishment of a joint venture, with a total investment of 800 million yuan, with Gree holding 51% and Daijin 49%. The joint venture company mainly produces frequency conversion compressors, circuit boards and moulds with a production capacity of 1.5 million units, 1.5 million pieces and 200 million yuan respectively. The important significance of this cooperation to Gree is that frequency conversion air conditioners are beginning to be recognized by the market, and Daijin's technical accumulation in frequency conversion air conditioners will bring great help to Gree's competitiveness in the field of frequency conversion.

Phase IV from April 2009 to 2012

First half of the year:Who is more flexible when home appliances go to the countryside?

At this stage, Gree's relatively beautiful valuation discount is due to Gree's announcement of a 136 million yuan reduction in 2008 net profit due to changes in income tax rates while disclosing the first quarterly report of 2009, opening Gree's relative beautiful valuation discount.

We believe that the valuation premium of Midea over Gree at this stage mainly comes from the policy of home appliances going to the countryside, which was extended to the country in 2009.Among the white electricity products, refrigerators and washing machines are the main products, while air conditioning is only one of the options everywhere.The elasticity is lower than that of ice washing.The number of ice washing per 100 households in rural areas increased rapidly between 2009 and 2011, while Midea's ice washing business has begun to take shape through acquisitions.

Since February 1, 2009, home appliances going to the countryside has been promoted to the whole country on the basis of the original 14 provinces and cities, and the number of products has also increased from four in the past to eight. In addition to the previous launch of "color TV sets, refrigerators, mobile phones, washing machines", motorcycles, computers, water heaters and air conditioners have been added to the countryside this time. They enjoy 13% of the state subsidy as well as products such as color TV sets. Each province and city can choose two of the four products to promote according to the different needs of each region.

From the financial data, during the period of home appliances going to the countryside, the profit growth of Midea Electric Appliances is indeed faster than that of Gree Electric Appliances.

Phase V 2012:The year of turning point of beauty

Gree operates steadilyThe market gives Gree more premium.

In 2012, Midea's operating revenue fell 26.89%, net profit fell 6.25%, and quarterly revenue fell by 41.78%.

What happened to the beauty of 2012?

From the perspective of the macro environment, the overall domestic economic growth slowed down in 2012, the original home appliances promotion policy withdrew, and real estate was also under regulation.

From the point of view of the company, Midea needs to be changed. Before 2011, Midea was still scale first. Although the scale of Midea Appliances came up, the profit margin was very low. After Fang Hongbo became chairman, the company took the initiative to promote the strategic transformation of quality growth, greatly reduced product categories, paid attention to the improvement and optimization of product structure, and took the initiative to give up the sales of some low-margin products. The company has formulated three strategic axes of "product leadership, efficiency drive and global operation" with the goal of continuously improving the quality of growth.

Gree in 2012 is still sound.

Gree also completed the transfer of power that year: in May 2012, the board of directors held a general election to elect a new board headed by Chairman Dong Mingzhu. In 2012, Gree achieved high performance growth, in sharp contrast to the decline of the United States.

Phase 6 from 2013 to now:

Factors other than performance give Mei more imagination.

1) Capital operation level

Midea went public as a whole in 2013, restarting the valuation premium for Gree Electric Appliances.

Midea went public as a whole in 2013, sorting out the related transactions between Homei Electric Appliances and Mei Electric Appliances, loading small household appliance business, motor business and logistics business into listed companies, creating "one beauty, one system, one standard", which is conducive to the integration of industrial resources and enhance synergy. With reference to the general premium for the listing of new shares, the valuation of Midea at this time appears at a premium relative to Gree.

The beauty of 2014 is closer to the tuyere than Gree.

The first is the release of the smart home strategy:March 11, 2014-Midea held a press conference on M-Smart smart home strategy. Relying on advanced technologies such as the Internet of things and cloud computing, Midea will change from a traditional home appliance manufacturer to a smart home enterprise. Complete sets of household appliances and systematization are more likely to win in smart homes than single-category companies.

The second is to cooperate with XIAOMI's business and equity in the tuyere:Midea announced in December 2014 that it had reached a strategic cooperation with XIAOMI to carry out multi-mode cooperation in the areas of smart home and its ecological chain and mobile Internet business. At the same time, the company will issue 55 million additional shares to XIAOMI Technology at a price of 23.01 yuan per share, raising no more than 1.266 billion. Upon completion of the offering, XIAOMI will hold 1.29% of Midea's shares and can nominate a core executive as a director of Midea. In 2014, the market preferred light assets and flexibility, XIAOMI is more favored by the capital, this cooperation is seen as the traditional home appliance manufacturing enterprises have been highly recognized by Internet enterprises.

2) Professional manager system and incentive plan continue to bind the interests of management and employees.

Fang Hongbo became chairman of Midea in 2012, and he Xiangjian withdrew from day-to-day management, officially opening Midea's professional manager system.

The core of the professional manager system is incentive and restraint. Since the beginning of 14 years, Midea has launched a series of equity incentive plans, including five periods of equity incentives for middle-level management and business backbone of headquarters and business departments; restricted stock plan for key executives of operating units; equity plan for core executive team.

3) Gree's operation fluctuates relatively.

In the previous report. "The riddle of valuation discount of Gree Electric ApplianceWe believe that under Gree's state-owned enterprise system, the change of management every three years may lead to increased volatility of the management pace in order to achieve short-term goals. As the air conditioning industry will still be affected by uncertain factors such as the weather, superimposing the regulation cycle of the real estate industry, Gree channel inventory has gradually accumulated after 2014, and Gree, together with the industry, ushered in a more painful inventory cycle in 2015. Gree Electric Appliances' revenue fell by 28.17% that year.

In additionMidea's acquisition of Kuka opens up a second runway besides home appliances. After Gree's acquisition of Zhuhai Yinlong, the development direction of diversification is not clear, and the market is more optimistic about the diversified track and future prospects of the United States.There has been a shift in the preferences of foreign and domestic institutions, and Midea has acquired more shares than Gree, which has also helped Midea continue to gain higher valuations.

To sum up:We think from 2005 to 2013,Although Gree and Midea have their own premiums at different stages of valuation, the core factor still lies in the changes in the company's fundamentals.After 2013, Gree's relatively beautiful depreciation comes more from a variety of problems caused by imperfect corporate governance, which makes the market more worried about the uncertainty of Gree.

Reviewing the valuation history of Gree and Midea, we can see two clear phenomena:

1) Gree's valuation is not natural but relatively beautiful and has a discount. When Gree is superior to beauty in some core factors, the market does not hesitate to give Gree a valuation premium. At the same time, the diversification of Midea is only one of the factors that affect the valuation.

2) the influence of corporate governance on Gree's valuation is becoming more and more important. Therefore, we believe that if the most important corporate governance issues restricting Gree's valuation can be improved, Gree's valuation is expected to be close to Midea.

Risk Tips:The influencing factors of historical valuation do not represent the future; real estate policy brings fluctuations in industry demand.

Source of report: Tianfeng Securities Research Institute

Date of release: April 23, 2019