Source: Wall Street News

Driven by global policies and measures, the field of electric vehicle batteries is ushering in unprecedented development prospects.

Currently, countries around the world have enacted separate laws and measures to promote the development of the electric vehicle industry in an effort to expand the development of the electric vehicle industry and supply chain in their own regions. Stimulated by the policy, Nomura Securities analysts Cindy Park, Yu Okazaki and others pointed out in a report published on March 21,In the next five years, global demand for electric vehicle batteries will grow at an annual rate of 18%, reaching 1647 GWh in 2028 and 2107 GWh in 2030.

Nomura Securities said that with the gradual withdrawal of China's electric vehicle subsidies and the removal of inventory from the supply chain in the first quarter of this year, China's electric vehicle industry will be in a moderate growth environment this year.

At the same time, as industry leaders such as the Ningde Era adopt strategic price cuts, competition in the battery market may intensify, and prices in the domestic market will drop further.

Nomura Securities predicts,The average selling price of power batteries in 2030 will be $136/kWh, down 9% year on year, mainly due to falling raw material prices.Nomura Securities believes that as cost reduction actions advance,Starting in 2024, the price of power batteries will drop by 3% every year until 2030.

Furthermore, lithium carbonate prices entering a downward channel will also help ease the profit pressure on battery manufacturers.

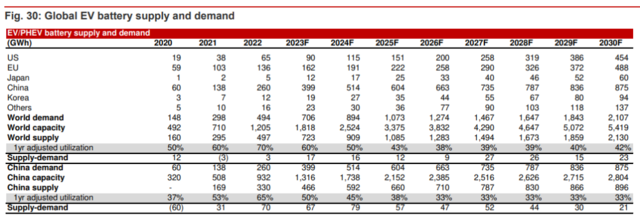

Global demand for power batteries will reach 2107 GWh in 2030

Nomura predicts,In 2023-2030, global battery demand for electric vehicles (including pure electric/plug-in hybrid vehicles) will grow at an annual rate of 17%; by 2030, demand for power batteries will reach 2107 GWh.This is estimated based on the fact that the penetration rate of electric vehicles will reach 34.6% by 2030:

We forecast that demand for electric vehicle batteries will increase 43% year-on-year to 706 GWh in 2023, average annual growth rates of 18% and 17% in 2023-2028 and 2023-2030, respectively, and reach 1647 GWh and 2107 GWh by 2028 and 2030, respectively.

This is based on global electric vehicle penetration rates of 15.8%, 29.8%, and 34.6% in 2023, 2028, and 2030 (11.8% in 2022), or 13.7 million electric vehicle shipments in 2023.

From January to February 2023, shipments of electric vehicles to 15 countries increased 24% year on year to 1.4 million units. Among them, China, the US, and 10 European countries increased 19%, 94%, and 5% year on year. China, the US, and ten European countries account for 59%, 16%, and 21% of global electric vehicle shipments.

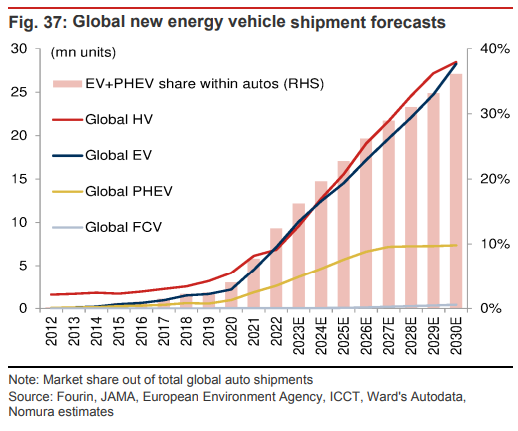

Specifically, Nomura Securities anticipates,Global sales of new energy vehicles (including hybrid vehicles, pure electric vehicles, plug-in hybrids, and fuel cell vehicles) will reach 64.5 million units by 2030, and sales of electric vehicles (including pure electric/plug-in hybrid vehicles) will reach 35.6 million units:

Our global automotive team predicts that sales of new energy vehicles will reach 35.9 million units/64.5 million units in 2025F/30F. The sales volume of electric vehicles will reach 2020 million units/35.6 million units, with a market share of 22.0%/34.6%.

In terms of production capacity, by the end of 2022, the global power battery production capacity will be 1205 GWh and the shipping volume will be 497 GWh. Nomura expectsBy the end of 2030, global production capacity will grow to 5419GWh, which means that between 2022 and 2030F, the capacity growth rate will be 21%At the same time, production capacity between regions will also change:

By region, 2023F China/Asia/North America/Europe other than China should account for 73%/5%/6%/16% of global battery production capacity. According to our estimates, this will change in 2030F to 52%/4%/17%/27%.

Battery prices will start falling in 2023

Nomura Securities said that as the price of raw materials and metals falls, the average price of batteries will fall in 2023, and is expected to fall by 9%:

For the seven battery manufacturers we cover — Panasonic, Ningde Times, LGES, SK On, Samsung SDI, Yiwi Lithium, and Guoxuan Hi-Tech — we forecast an average sales price of $136 per kWh in 2023, down 9% year over year.

According to our estimates, the average price increased 13% in 2022 due to a sharp rise in metal prices. In 2022, the average price of lithium carbonate/nickel carbonate was 71,653 US dollars/ton and 26,187 US dollars/ton, respectively, up 287%/42% from the previous year.

For 2023F, we estimate that ASP (average selling price) will drop 9% because we think the prices of these metals will drop.

However, so far this year, some cathode material manufacturers have indicated that their ASP has risen. Starting with 2024F, we predict,Electric vehicle battery prices will drop 3% per year until 2030F, as part of cost reductions.

Furthermore, Nomura said that since car companies want to reduce costs, all battery manufacturers are also under pressure to reduce costs and average selling prices. For example, Tesla said on Investors Day in March 2023 that it plans to reduce costs by 50% through scale growth, higher productivity/cost efficiency/supplier size, product improvements, engineering changes, and localization.

Nomura Securities believes thatThese goals should be the shared vision of the electric vehicle industry, not just Tesla's related vision.

As far as the seven battery companies covered are concerned, Nomura Securities said,Even if battery prices fall in the future, Chinese battery companies are expected to remain competitive:

The average operating margin for the seven companies in 2022 was 1.6%, and we forecast this figure to rise to 5.1%/7.1% in 2023F/25F, respectively.

We estimateThe average price of the three Korean battery companies (LGES, SDI, SK On) in 2022 was 44% higher than that of Chinese battery manufacturers (Ningde Era, BYD (not covered), Yiwi Lithium Energy, Guoxuan Hi-Tech). Since 50-60% of China's battery production is based on low-cost LFP, the average battery price in China is lower than that of Korea/Japan.

This competitive price and higher than industry average profitability have driven strong battery demand and supply growth.While we expect this price gap to persist across countries, profit margins are likely to subside over the next few years.

Battery technology: higher energy density, longer life, and better thermal stability

As far as the technical route of power batteries is concerned, Nomura Securities believes that power batteries are moving towards higher energy density, longer life, and better thermal stability:

We expect the energy density of NCM/NCMA EV batteries to reach 720-750Wh/L (280-310Wh/kg) in 2023,After 2025, the energy density is expected to shift to 800 Wh/L (320 Wh/kg).

Furthermore, we think the silicon mixture in the anode has the potential to rise to 5-8% (NCM) from around 5% now.

As for lithium iron phosphate batteries, Nomura estimates that the current energy density is about 150 Wh/kg.The goal is to move in the direction of 800 Wh/L (more than 320 Wh/kg) within the next few years,To provide electric vehicles with a driving range of around 600-700 km per charge and a charging time of less than 15 minutes:

To achieve this goal, we estimate that cathodes containing more than 90% nickel, about 10% silicon-graphite, and wet diaphragms less than 9 microns thick are needed.

Lithium/nickel prices: 2023/2024F is expected to decline

Nomura Securities believes that since the increase in lithium supply in recent years has exceeded the increase in demand, the 2023/2024 lithium price is expected to fall 35%/ 20% year-on-year; with a slight increase in nickel supply, prices may also remain flat or rise.

We estimate,Global lithium supply will grow at a compound annual rate of 33% between 2022-2025, driven by the expansion of existing production capacity and the commissioning of new projects, which will exceed our estimated 18% compound annual growth rate of lithium demand over the same period.

A more balanced supply and demand situation will provide more room for lithium prices to decline, which is expected to fall 35%/20% year over year in 2023/24.

We still believe that the trend of electrification will remain strong in the automotive industry, and that the normalization of lithium prices should provide room for further cost optimization in the electric vehicle supply chain.

Driven by a surge in demand for electric vehicle batteries, lithium prices rose significantly from the second half of 2021 to the first half of 2022. By the end of June 2022, the price of lithium reached 71,376 US dollars per ton (up 401% year over year). Lithium prices remained high throughout 2022, reaching a peak of $81,412 per ton in mid-December. Lithium prices fell 7% and 13% month-on-month in January and February 2023, respectively.

Nomura Securities said this was mainly due to increased lithium mining by major miners, easing supply constraints, and falling demand for electric vehicles in early 2023.

Furthermore, the global lithium refining market will become more fragmented, although driven by the electric vehicle boom and the increase in lithium prices in 2021-22. Nomura Securities still believes that leading lithium producers with high-quality mineral resources and lower production costs should maintain their competitive advantage with high-end customers and better profitability.

As a result, Nomura Securities expectsIn 2022-25, global lithium refining capacity will grow at a compound annual growth rate of 26%, from 1,064 million tons of lithium carbonate equivalent in 2022 to 2.12 million tons of lithium carbonate equivalent in 2025.

In terms of nickel prices, since nickel products are classified into different grades according to purity, and grade 1 nickel is the only suitable raw material for producing nickel sulfate used in battery manufacturing, production costs are often high. Nomura Securities expects that there may be a shortage of high-quality nickel supply in the medium term.

In the first half of 2022, due to geological issues, nickel prices skyrocketed, reaching $29,886 per ton at the end of 2022, up 55 percent from July 2022.

However, although nickel prices are still at a high level, nickel prices have fallen to $24,358 as of March 3, 2023 due to weak demand for electric vehicles and increased global production.

Nomura Securities said production of high-purity nickel from subsequent mines in Indonesia will increase due to refining of low-purity nickel.

edit/ruby