Source: Securities Times

Author: Wu Shun

On March 23, China Mobile, another company with “Chinese characters”, released its 2022 report. According to the annual report, China Mobile performed well in 2022, with revenue approaching trillion yuan: 2022 achieved revenue of 937.3 billion yuan, an increase of 10.5% over the previous year; profit attributable to shareholders was 125.5 billion yuan, an increase of 8% over the previous year.

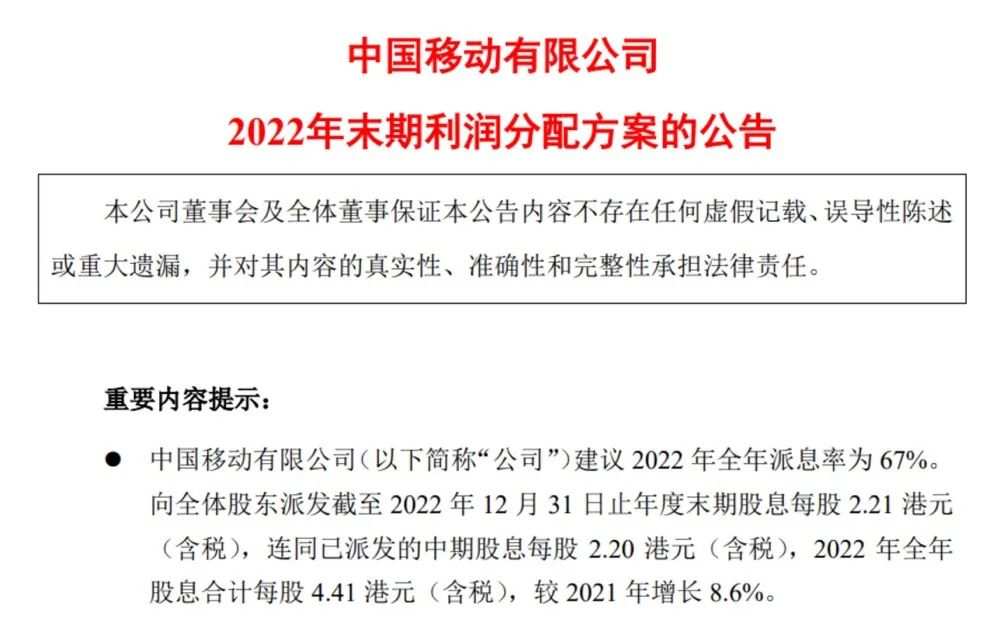

However, what is even more impressive is that China Mobile revealed that it plans to pay out 67% of its 125.5 billion yuan earned in 2022. This amount of capital exceeds 84 billion yuan, and the dividend ratio will exceed 70% in 2023.

On March 23, companies with “Chinese characters” once again rose collectively. Wind market data shows that on the same day, the central enterprise index with the letters in Wind closed up 0.74%, and the total market value of the sector exceeded 13 trillion yuan. Among the constituent stocks, China Weitong stopped rising, while many stocks such as China Industrial International, China Aviation Electric Test, and China Aluminum rose more than 5%. In fact, this is just a microcosm of the recent explosion of “Chinese characters” concept stocks. Since November last year, individual stocks with “Chinese characters” have been rising one after another. Judging from this year's growth alone, China Aviation Telecom, which had the highest increase, measured more than 400%, China Satellite Communications rose more than 100%, and Zhongke Shuguang, China Telecom, COSCO Haike, and China Industrial International rose more than 50%. At the same time, quite a few “Chinese leading” companies are already on their way to increasing their dividend ratio.

With the large increase that has already been accumulated and the larger dividend ratio, can companies with “Chinese characters” catch up?

The dividend ratio of many “Chinese leading” companies will reach 70%

According to the announcement, China Mobile has previously paid an interim dividend of HK$2.20 per share (tax included), and this time it will pay a final dividend of HK$2.21 per share (tax included). The total annual dividend is HK$4.41 (tax included) per share, an increase of 8.6% over 2021.

As of December 31, 2022, China Mobile's profit attributable to shareholders at the end of the period was RMB 125.459 billion. China Mobile stated in its profit distribution plan that it is recommended that the dividend rate for the full year of 2022 be 67%. If calculated on this basis, China Mobile's 2022 dividend amount will exceed 84 billion yuan.

However, the 67% dividend ratio is not the end of China Mobile. China Mobile also said that in order to better give back to shareholders and share development results, the company fully considered profitability, cash flow conditions and future development needs. The profit distributed in cash in 2023 increased to more than 70% of the company's shareholders' profit that year, and continued to create greater value for shareholders.

In fact, the Securities Times reporter noticed that not only is China Mobile increasing its dividend ratio; quite a few “Chinese character” companies are already on their way to increasing their dividend ratio.

On March 22, China Telecom announced that it would distribute a final dividend of RMB 0.076 (tax included). Based on the total share capital at the end of 2022, the total amount was RMB 6.955 billion. The dividend was derived from the net profit realized during the period. In addition to the dividend already distributed in mid-2022 of RMB 0.120 per share (tax included), the dividend for the full year of 2022 was RMB 0.196 per share (tax included), totaling RMB 17.935 billion, accounting for 65% of the profit attributable to the company's shareholders in 2022.

Earlier, China Telecom also stated that the company attaches great importance to shareholders' returns, actively fulfills profit distribution promises, announces interim dividends starting in 2022, and will gradually increase the profit distributed in cash every year to more than 70% of the profit that the company's shareholders should account for more than 70% of the profit that year within three years after the issuance and listing of A-shares, continuously creating value for the majority of shareholders.

According to China Unicom's annual report, the board of directors recommended a final dividend of RMB 0.0427 per share (tax included), along with the interim dividend already distributed of 0.0663 yuan per share (tax included). It is estimated that the annual dividend per share will reach 0.1090 yuan (tax included), an increase of 24% over the previous year. The total dividend amount accounts for 76.2% of net profit in 2022.

The China Ping An Annual Report announcement also stated that due to the continued growth in the company's operating profit and full confidence in Ping An's future prospects, the board of directors recommended a cash dividend of RMB 1.50 per share (tax included) for the end of 2022, plus the interim dividend of RMB 0.92 per share in cash (tax included), and the annual dividend of RMB 2.42 per share (tax included), up 1.7% year on year, accounting for 53.6% of Fumo's net profit in 2022.

In fact, “Chinese leading” companies have paid more and more attention to shareholder dividend ratios in recent years, and some have even distributed all of their profits throughout the year. For example, China Shenhua's net profit in 2021 was 50.2 billion yuan, and the total dividend for 2021 was 50.4 billion yuan, accounting for 100.4% of the net profit attributable to the company's shareholders under the 2021 China Enterprise Accounting Standards. In other words, China Shenhua distributed every profit earned in 2021 to shareholders.

As to why companies with “Chinese letters” have frequently increased their dividend ratios and increased shareholder returns in recent years, Yu Dingheng, chairman of Maverick Investment, said in an interview with the Securities Times reporter, “The biggest highlight of this round of changes in the central state-owned enterprise assessment system is unifying the interests of management and shareholders, introducing market-based incentive mechanisms for equity incentives to activate management, while increasing the dividend ratio to balance shareholders' rights. In the future, growing industries will pay more and more attention to equity incentives, while leading value industries will continue to increase dividend payments to enhance shareholders' actual returns and share the value of enterprise growth together will become an important market trend.”

Shares of “Chinese characters” companies have soared

According to information, since the “valuation system with Chinese characteristics” was introduced in November last year, the stock prices of many “Chinese characters” companies have soared, with many companies' stock prices rising by more than 30% or even 100%.

The Bosch Fund Index and Quantitative Investment Department believe there are three main reasons for the sharp rise in “Chinese characters” stock prices. First, procyclical and broad-market value styles prevail. Since 2023, economic recovery expectations have fermented ahead of schedule, and procyclical sectors and general market value styles that are more linked to domestic demand have begun to dominate, and blue-chip stocks with “medium letters” have taken advantage of the momentum. Second, the market is gradually focusing on the “valuation system with Chinese characteristics” and the reshaping of valuations of “Chinese characters” companies, so the “Chinese character” stock prices, which are cost-effective in valuations, have been catalyzed to rise. Third, the strengthening of operators has led to a rise in the “middle letter” stock prices. Under the joint catalysis of digital China and the revaluation of central state-owned enterprises, operators have strengthened, further boosting market sentiment about “Chinese leading” stock prices.

“The rise in 'Chinese letters' stock prices stemmed from the introduction of a valuation system with Chinese characteristics in November last year. 2022 is the final year of the three-year action to reform state-owned enterprises. Driven by the dividends of state-owned enterprise reform policies, the 'Chinese letter' ushered in a double increase in policy and performance fundamentals. Under the current market pattern, the overall valuation of the 'Chinese letter' is undervalued, and there is plenty of room for reshaping. The entry of large amounts of institutional capital has also been the driving force behind the rise in China's leading stock prices.” Yu Dingheng said.

According to Yu Dingheng, the investment value of companies with “Chinese characters” simply comes from Davis's double click on policy and performance fundamentals. The first policy aspect is that the revaluation of state-owned enterprises is expected to become an important foothold in building a valuation system with Chinese characteristics. State-owned enterprises, as the “ballast stone” of stable economic development, have obvious policy dividends; the second is the reform of state-owned enterprises, deepening the market-based assessment of the State Assets Administration Commission, speeding up specialized integration, unifying the interests of management and shareholders, and further harmonizing the interests of state-owned enterprises with market-based mechanisms; in terms of fundamentals, industrial upgrading brought about by the market-based transformation of central enterprises is expected to be profitable in the context of favorable policies and increased efficiency of their own industrial upgrading. Speeding up, while China Against the backdrop of economic recovery, the performance of “Chinese leading” companies is expected to improve further. There will be an increase on the valuation side in the short term, and an improvement on the performance side in the medium term. As ETFs enter the market, they may bring further incremental capital to the “medium valuation” sector.

Research by CITIC Securities also points out that state-owned enterprises currently have high investment value: 1) State-owned enterprises are an important pillar of the national economic system. Listed state-owned enterprises account for a relatively high proportion of industries related to national security and the lifeblood of the national economy, especially traditional industries; 2) the profits of state-owned enterprises are stable and growing. Benefiting from the reform of state-owned enterprises, the revenue growth rate of listed state-owned enterprises is now on a par with that of private enterprises. Under policy guidance, the number of state-owned enterprises and the amount of dividends paid by central enterprises is increasing year by year; 3) State-owned enterprises, especially central enterprises, have a significant valuation of private enterprises;, as of the end of 2022, there are approximately 17.86% of state-owned enterprises are in a state of bankruptcy; 4) State-owned enterprises will enjoy reform dividends for a long time. The number of state-owned enterprises that have issued equity incentive plans has risen markedly in recent years, the R&D expenses of state-owned enterprises have increased steadily, and scientific and technological innovation capabilities are expected to continue to improve.

Can the popularity of “Chinese lettering” companies continue?

However, it is important to note that the “Chinese first” stock price has accumulated a high increase since November of last year. Recently, China Mobile and China Telecom, both benchmark individual stocks, have been drastically adjusted. In particular, on March 20, China Mobile and China Telecom's A-shares both came to a standstill.

In response, Yu Dingheng said, “One reason for the recent adjustment is that it has risen too much and is under pressure from internal adjustment. In the market environment of capital stock games, the short-term rise was too fast, and the fragility of the overcrowded sector increased. Under the scenario of rapid sector rotation, capital switched tracks and ushered in a phased recession. Looking at the long term, the revaluation of state-owned enterprises is expected to become an important foothold in building a valuation system with Chinese characteristics. The trend is improving, but sustainability still needs to be observed. Currently, domestic investors need to slowly establish their investment beliefs about 'Chinese' companies, which must be measured in the long term by combining comprehensive factors such as policy orientation, corporate fundamentals, and shareholder returns.”

The Bosch Fund Index and Quantitative Investment Department said that improvements in the profitability and corporate governance of central state-owned enterprises were not achieved overnight; improvements in profitability were a necessary condition for the subsequent valuation ceiling to open up further. At the current stage of the market, many central state-owned enterprises have clearly increased, and the further interpretation of future market conditions depends on the subsequent release of profits by central state-owned enterprises. The improvement in profits and cash flow of central state-owned enterprises will mainly come from three aspects: one is to optimize operating efficiency through reforms; the second is to make full use of the advantages of capital resources to improve the return on investment; and the third is to increase the net profit conversion rate of cash flow. Subsequent, with the establishment of rules for the revaluation of state-owned enterprises and the actual improvement in the quality of central state-owned enterprise companies, there is more room for the valuation of companies in industries that can release profits in the next stage to increase, and it can also bring about a sustainable market. Therefore, it is worth focusing on following up and observing the improvement in the operating efficiency and quality of operation of central state-owned enterprises in the future.

Editor/jayden