Source: Wall Street News

The US regional banking crisis is putting pressure on commercial real estate debt maturing close to trillion dollars this year and next two years. Since small and medium-sized local and regional banks surpassed the largest banks last year and became the biggest lenders for commercial real estate loans, this may in turn exacerbate the current regional banking crisis, which is “only affected by liquidity shocks.” The time bomb, the repayment crisis in the commercial real estate sector, is counting down.

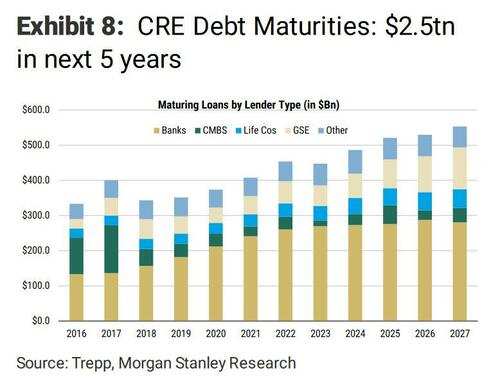

A few days ago, Wall Street news mentioned that the US banking industry, particularly small and medium-sized banks that are experiencing a liquidity crisis, is facing the “next nuclear bomb” — commercial real estate loans. Over the next five years, this major risk exposure test is imminent: $2.5 trillion in loans will expire.

Research reports from the Real Assets department of MSCI (MSCI) show that US commercial real estate debt of 400 billion US dollars will expire in 2023, another nearly 500 billion US dollars of loans will expire in 2024, and a total of 25,000 US dollars of debt will expire within the next five years.

Since the second half of last year, the largest banks in the US have successively shrunk their exposure to commercial real estate loans, and small and medium-sized banks have risen to prominence and become the main force in issuing new commercial real estate loans,Recent bank turmoil in these regions has increased pressure on commercial real estate debt.

Research reports say that, on the one hand, lenders may reduce the size of loans after the collapse of regional banks. At the same time, higher borrowing costs and falling real estate values in an environment of interest rate hikes have made it more difficult for commercial property owners to refinance (refinance) existing mortgages.

This has formed a vicious cycle,That is, as the US banking crisis spreads, smaller banks may further retract the scale of commercial real estate loans, and private debt funds may participate to fill the gaps, but the financing costs they require will be higher, and they are unlikely to reach the required scale, causing a credit crunch situation.

Coupled with the new business and telecommuting models in the post-pandemic era, this in turn will increase the risk of commercial real estate defaults, and even threaten the solvency of the entire small banking sector. It may have a devastating impact on small banks because small banks are too exposed to risks in the industry.

Furthermore, this will continue to exacerbate market fears. Wall Street News mentioned last week that office properties in commercial real estate are the next “thunderstorm” for small banks in the US, and the harm could quickly spread to large banks:

The biggest firepower of the bears was focused on real estate in office buildings and corresponding REITs. If it ignited a debt repayment crisis, once the small banks fell, the big banks would not be far away.

Jim Costello, an economist at MSCI Real Assets, said that last week's turmoil in the US banking industry hit the lender group that supported the most commercial real estate mortgage loans in 2022 — small and medium-sized regional banks:

It's like punching another person when they fall, which will undoubtedly speed up the process of falling. The point is that this is happening.

According to MSCI's research report, given higher interest rates and uncertain prospects, the volume of commercial real estate transactions in the US fell 51% year-on-year to 26.9 billion US dollars in February, that is, the scale was severely undermined. In the 12 months up to February this year, transaction prices fell 6.9%, with apartment prices falling 8.7%.

All of this happened before the US regional bank liquidity crisis in March caused the suspension of new loan issuance activities:

The trend in commercial real estate transaction activity, pricing, and credit availability was already pointing downward before the banking industry faced recent challenges. The turmoil of recent weeks may be seen as a driving force that has accelerated the changes that have taken place.

The financial blogger Zerohedge, which has always been famous for its poisonous tongue, commented,The plight described above shows that the time bomb is counting down.

In the Markit CMBX index, which tracks 25 types of commercial real estate mortgage-backed securities, only the BBB-grade with the lowest rating (which also best reflects market speculative sentiment), the prices of all other “series” have plummeted, with the exception of “Series 15,” which has the greatest exposure to office building loans, which fell to a record low.

In fact, almost all of CMBX's “series” products that can be traded fell at the fastest rate since the collapse of risky assets caused by the COVID-19 pandemic in Europe and the US. The previous collapse occurred when Lehman Brothers went bankrupt in 2008.

Meanwhile, starting last week, holding premiums for highest-rated commercial real estate mortgage-backed securities (CMBS) have also risen, close to the high level in late October last year, second only to the impact of the 2020 pandemic and the 2008 global financial crisis.

In other words, in the field of asset securitization products for commercial real estate debt, investors have almost nowhere to escape. “As the broader risk market is sold off, no place in the CMBS sector is safe.”

In terms of specific data:

In the commercial office real estate sector, MSCI believes that nearly 40 billion US dollars of real estate is more likely to be in trouble, which means that banks and other lenders will face pressure to repay this batch of debt.

Property holders received about 27% of commercial real estate financing from local and regional banks in the US last year, the biggest source of new debt issued in this sector.

J.P. Morgan and Goldman Sachs pointed out that as of February of this year, before the regional banking crisis, the commercial real estate loan exposure of small and medium-sized banks in the US reached an astonishing 70%-80%.

Jim Costello, an economist at MSCI Real Assets, said that in a typical chain dilemma, if small and medium-sized local and regional banks slow down lending due to deposit crowding, it will hit small enterprises with few other sources of financing in the market.

Editor/jayden