Source: Wall Street News

Author: Han Xuyang

High returns are often accompanied by high risks, and there are no free lunches in the world.

On Sunday, March 19, local time, just before the Asian market opened on Monday, UBS announced that it would buy Credit Suisse for 3 billion Swiss francs under the “coordination” of the Swiss government.

The Swiss Federal Government and the Domestic Financial Markets Supervisory Authority (FINMA) said on Sunday that after the Swiss government supports UBS's acquisition of Credit Suisse, Credit Suisse Additional Tier 1 bonds with a face value of about 16 billion Swiss francs (about 17.2 billion US dollars) will be completely written down. This means that to ensure that private investors can help cover the costs, these face value bonds will become worthless.

This will also be the biggest value write-off event in Europe's $275 billion AT1 market. Generally speaking, bonds have higher priority than stocks, which means that shareholders generally return their losses to zero before taking the bond's turn. However, in this transaction, AT1 bonds returned to zero before stocks, which angered AT1 bond holders. Institutions that still hold these bonds are furious, believing that this is a decision that ignores market practices and may even be illegal.

UBS CEO Ralph Hamers told analysts that the decision to reduce AT1 bonds to zero was made by FINMA, so there would be no liability for UBS. Although European financial regulators also expressed concern about this approach by the Swiss authorities, they also reiterated that common equity tier 1 capital (CET1) bears losses before AT1 bonds, and that equity is cleared before AT1. Credit Suisse may only be an exception.

However, analysts believe that this move may have a more profound impact on the European bond market, leading to a sell-off of other banks' bonds.

So what exactly is this Credit Suisse Additional Tier 1 (AT1)? And why does it continue to have an impact on the precarious bond market?

What is AT1?

Additional Tier 1, or additional tier 1 capital bond, is a product of the European regulatory framework after the global financial crisis, and is a type of subordinated debt that can be included in banks' supervisory capital. In addition to holding more common share capital, large banks are also forced to issue “contingent convertible bonds” (Contingent Convertible Bonds, or Cocos Bonds).The most common form of these Cocos bonds is AT1.

“Convertible” is because they can be converted from bonds to equity (or full write-down), while “maybe” is because this conversion only occurs when certain trigger conditions are met, such as the issuing bank's capital strength being lower than a pre-determined trigger level.

CoCOs are mainly issued by banks, but also by insurance companies and non-bank financial institutions. Banks must comply with regulatory requirements such as the Basel Agreement and maintain a minimum required amount of common equity tier 1 capital (CET1) as a percentage of their risk-weighted assets (RWA).

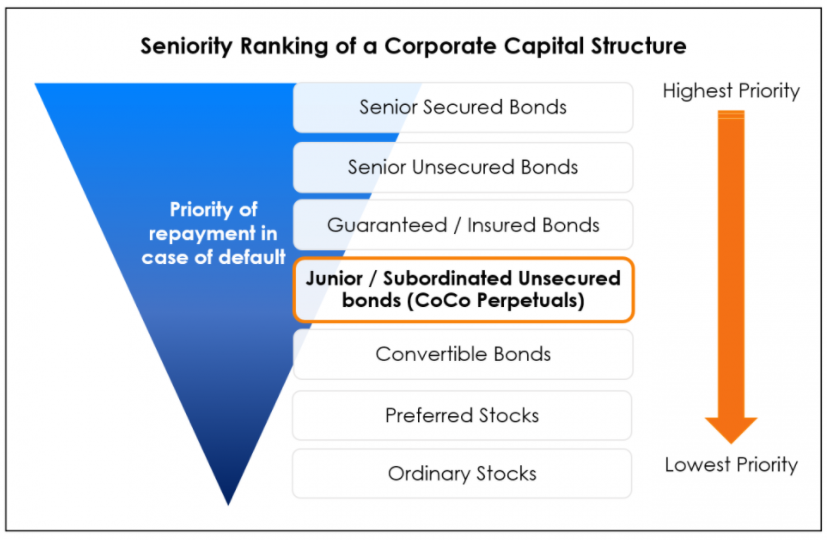

In order of capital structure prioritization, Cocos and AT1 have lower priority than all other debt, and are therefore only higher than common stock, preferred stock, and convertible debt.Considering that COCoS is ranked lower in the capital structure, the ticket interest they pay is higher than that of traditional bonds, and the yield is also higher; in addition, since COCoS has call options, the yield will also be higher to make up for the risk of issuers redeeming the bonds.

This means that AT1 bonds are generally the highest-yielding bank bonds investors can buy because the bond holder wants to be compensated for the additional risk.

Lloyds Bank of England issued the first batch of COCOs (then known as enhanced credit notes or ECNs) in November 2009, totaling £8.5 billion. If the core capital falls below 5%, these bonds will be converted into equity.

What are the characteristics of AT1? Why are banks issuing AT1?

After the government and taxpayers were asked to bail out some large banks during the 2008 global financial crisis, regulators took action to improve the quantity and quality of capital held by the entire banking system. For European banks, AT1 is a key component of this new system.

Under the new global regulatory framework after the introduction of Basel III in 2010, the core capital (common stock) adequacy ratio of commercial banks was raised to 4.5%, and the total capital adequacy ratio was raised to 8%. Notably, national regulators often set separate minimum capital requirements for each major bank, which are often far higher than these global minimum standards.

AT1 has three basic characteristics,The most important characteristic is the “loss absorption mechanism”, which is the key difference between AT1 bonds and ordinary bonds. The mechanism is triggered when the bank's CET1 capital ratio falls below a pre-determined threshold.This trigger point is usually 5.125% or 7% of CET1, depending on the country's regulators. Once this trigger level is reached, these bonds will automatically be converted to equity or written down completely, depending on the terms of the individual bond documents.

Losses are absorbed in two ways, converted to equity or principal write-down. Converting to equity is the function of converting a bond into equity at a pre-determined conversion rate, which will be detailed in the prospectus. This conversion rate may be a pre-defined price, a market price, or both.

HSBC's pre-determined conversion rate is 6.25%. The new conversion uses the new conversion price (NCP) mentioned in its prospectus, and the formula is as follows:

The write-down of principal reduced the book value of the debt, harmed the interests of CoCo investors, and saved the company and its equity holders. A write-down can be permanent or temporary, partial, or full.

Second, regulators require bank capital to be permanent (that is, perpetual), so AT1 bonds do not have a final maturity period, but can be redeemed if approved by the regulator. AT1 usually has a “non-redemption” period of 5 to 10 years, after which investors usually expect issuers to redeem and replace these AT1s with newly issued AT1. If the bond is not redeemed, then the coupon interest rate will be reset to the relevant swap rate or the equivalent interest rate of the government bond.

Third, AT1's coupon payments are non-cumulative and can also be freely disposed of. Late payments do not become an expense for the bank, and non-payment is not considered a default or credit event.

Overall,Banks issued AT1 to support their balance sheets with sufficient capital. In this way, in the event of financial stress, losses can be absorbed without the need for taxpayers to bail out, thereby reducing the financial burden on the government and taxpayers.

What are the risks of AT1?

First, the most obvious risk is,When a bank's capital situation worsens to the point where the CET1 ratio falls below the trigger level, it means that AT1 bond holders either lose their principal completely or can only hold shares in undercapitalized banks.

Normally, Europe's largest banks (and therefore the largest AT1 issuers) need very sufficient capital. In the first quarter of 2022, the average CET1 ratio for the banking industry as a whole was 14.98%, which means banks usually have large buffers above the AT1 trigger level, and these buffers will only be broken when there are really huge losses.

Second, like most perpetual bonds, Cocos usually has redemption options, which are in the hands of the issuer rather than the holder of the bond. In theory, banks can choose not to redeem the bonds and keep the capital forever. This is an equity-like characteristic of AT1.At this point, there is a “risk of bond rollover”, that is, the risk that the maturity of securities will be extended due to a slowdown in advance payments.

In theory, if banks decide not to redeem their bonds, investors will always only receive returns in the form of interest notes, or try to sell these perpetual bonds in the secondary market to recover the principal amount based on market liquidity.

However, like all large bond issuers, banks rely on continuing relationships with investors to enter the bond market regularly. Choosing not to redeem AT1 bonds as expected will almost certainly seriously damage the bank's reputation among investors and may cause borrowing costs to continue to rise in the future, creating a vicious cycle.

Third, regulators can stop issuing AT1 bonds.According to a regulation called “Maximum Distributable Amount” (MDA for short), if the bank's CET1 capital ratio falls below a certain level, the regulator can restrict the bank's issuance. However, just like AT1's trigger level, European banks usually maintain large buffers above a given MDA threshold.

Regulators can also suspend allocations to trap capital within the banking system as a precautionary measure in the face of pressure or increasing losses. However, based on historical experience, for example, in response to the pandemic crisis in 2020, regulators are more inclined to suspend other allocations such as stock dividends and bonus pools until they stop issuing AT1 bonds.

Investors also need to consider another important regulatory factor: a bank's solvency is ultimately determined by its national regulator (the European Central Bank in the case of EU banks). If a bank is in serious trouble, regulators can declare a “point of non-living” (point of non-living) to protect savers, contain losses, and prevent the crisis from spreading.

Analysts believe that the CET1 ratio of European banks is generally around 15%. It takes too long for a bank's CET1 ratio to drop to 7% or even 5.125%. It is unlikely that any regulator will allow this bad situation to continue for too long. Therefore, in reality, a bank's “non-viability point” may be higher than the trigger level implied by AT1. Investors must pay attention to the individual capital requirements set by national regulators for each bank.

Editor/Somer