Source: Wechat official account Sweet clover and her oil and gas partner author: Zhang Xilan team

Original title: logic of valuation and repair of energy central enterprises

The valuation of central enterprises repaired the scarcity of superimposed oil products assets, helping to push up the share price of three barrels of oil.

This week, the market paid more attention to the central enterprises, and the share prices of three barrels of oil companies rose. Since the beginning of the year, Hong Kong shares of three barrels of oil have risen an average of more than 25 per cent; A-shares China Petroleum & Chemical and CNOOC are both up more than 20 per cent, and Petrochina is up nearly 14 per cent.

Guotai Junan Securities also issued a research report saying that the crude oil price center will be better than market expectations, oil stocks are in the booming stage in 2023, and upstream enterprises have better investment value in the long run.

Why are three barrels of oil, whose valuations have long been lower than those of overseas oil companies, soaring? The following is an analysis from the Zhang Xilan team of Tianfeng Securities.

Core viewpoints

The addition of the central enterprise assessment index "return on net assets" index is a major change.For energy central enterprises, we believe that energy central enterprises may usher in a round of valuation repair if the top-down market environment is improved and the competitiveness is enhanced from the bottom up.

Logic one: double carbon promotes the center of energy prices.We judge that the oil price center has risen from about 50-60 US dollars per barrel in previous years to about 70-80 US dollars per barrel; China's coal price has risen from about 500,600 yuan per ton in previous years to about 1000 yuan per ton, and the market has basically formed a consistent expectation.

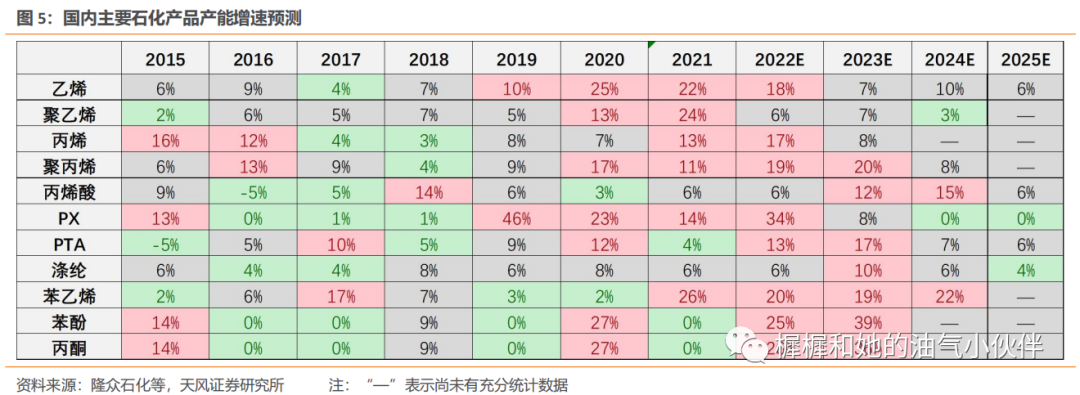

Logic 2: improve the pattern of domestic refining and chemical market and enhance the scarcity of assets.The notice of the carbon Dafeng Action Plan by 2030 clearly requires that by 2025, the primary processing capacity of domestic crude oil will be controlled within 1 billion tons. In the next three years, we expect domestic aromatics production capacity to stagnate, olefin growth to slow, and even slightly negative production capacity of oil products.

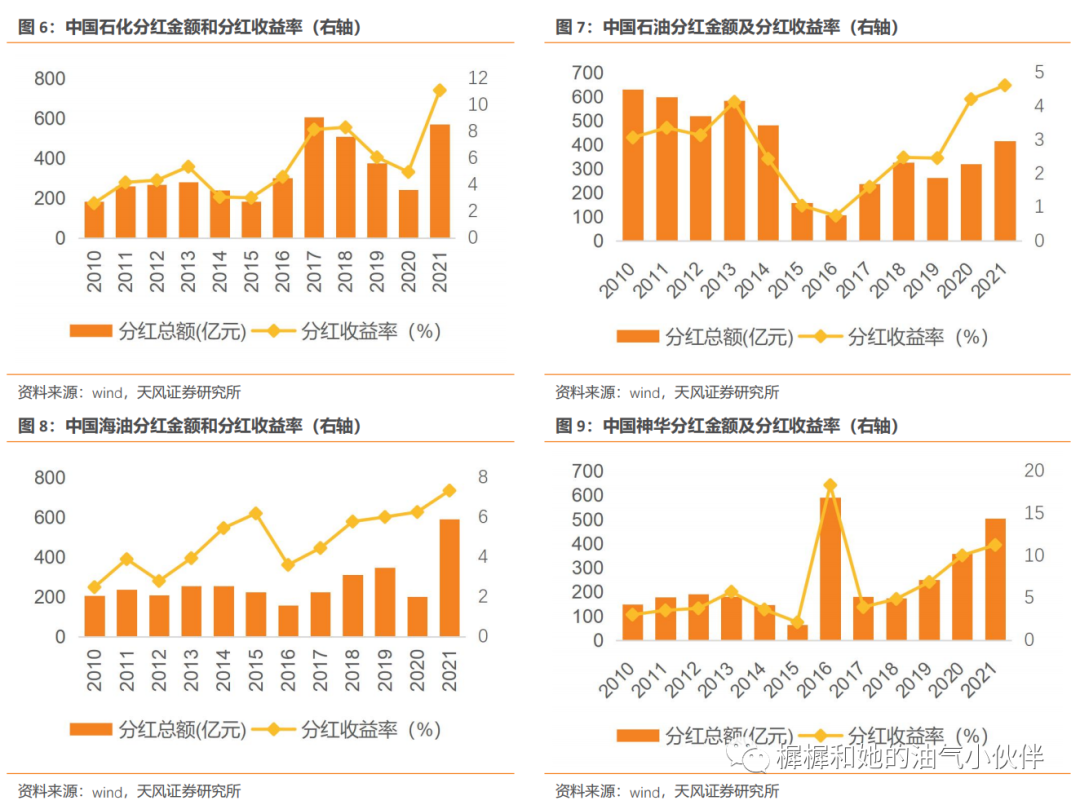

Logic 3: attach importance to dividend repurchase.In terms of dividends, we expect the future dividend yields of several central energy enterprises (China Petroleum & Chemical, China Shenhua Energy, CNOOC, Petrochina) to be around 6-10%. And China Petroleum & Chemical (Ajuh) and CNOOC Limited (H) have repurchase and dividend behavior respectively.

The assessment of the return on net assets is expected to promote the efforts of central energy enterprises to improve ROE and promote valuation repair.We believe that among the central energy enterprises, CNOOC and China Shenhua Energy, which have relatively high ROE, have been repaired to about 1.5 times the valuation of PB, but there may be some room for repair compared with international oil companies. At present, the PB valuations of China Petroleum & Chemical and Petrochina are still significantly lower than 1, and the valuations of the two companies are expected to usher in a round of repair in recent years as the business environment improves, as well as bottom-up efforts to reduce costs, and pay more attention to dividend repurchase.

On March 3, the SASAC of the State Council held a meeting to mobilize and deploy state-owned enterprises to carry out world-class enterprise value creation actions. It is necessary to highlight efficiency, speed up the transformation of the mode of development, focus on indicators such as total labor productivity, the rate of return on net assets, and the rate of economic value added, improve quality, increase efficiency and stabilize growth, and effectively improve the level of return on assets. The addition of the "return on equity" index is a major change.

Specific to the energy central enterprises, we believe that the top-down market environment improvement, bottom-up competitiveness, energy central enterprises may usher in a round of valuation repair.

Logic 1: double carbon promotes the price center of energy products

Carbon neutralization suppresses the willingness to invest and enhances the oil price hub.International oil companies have put forward their own goals of carbon neutralization, especially European companies are relatively active. Shell, for example, proposed in its 2021 energy transformation strategy that crude oil production peaked in 2019 and fell by 1-2pct a year thereafter.

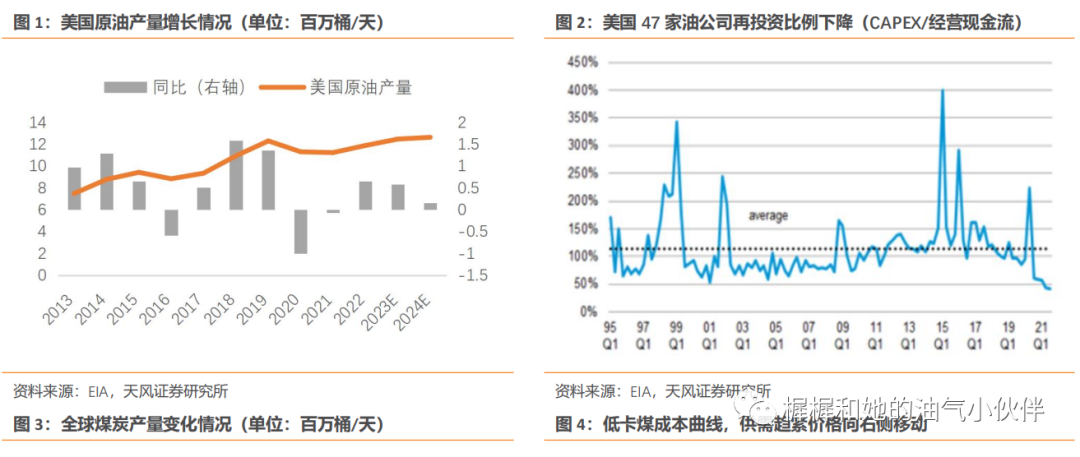

In the United States, shale oil has been the main source of growth in global crude oil supply over the past decade, and we believe that with the return of the United States to the Paris Agreement in 2021, it may bring about changes in investor will and policy environment, it may restrict the growth of shale oil production. According to the EIA, the growth rate of US crude oil production is expected to maintain at about 500000 barrels per day in the past two years, although it has maintained a certain growth, but it is incomparable to the annual growth rate of more than 1 million barrels per day in some previous years.

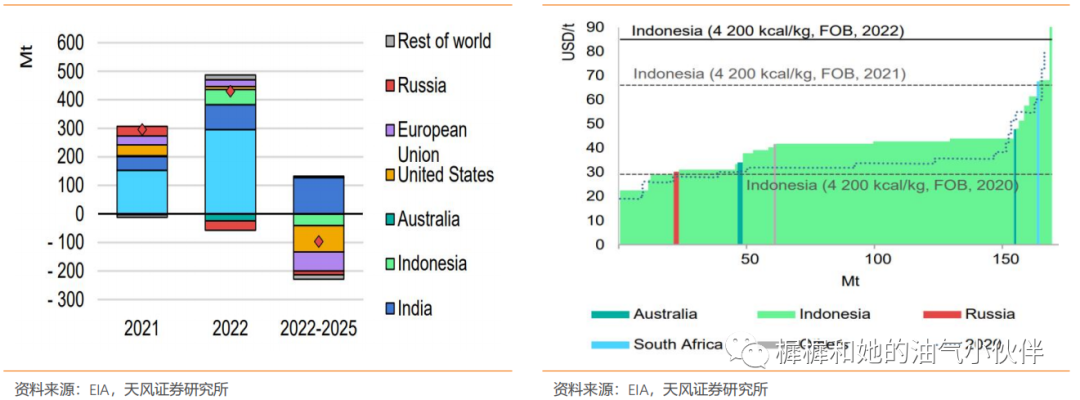

Coal prices are also affected by carbon neutralization factors.Overseas, according to the IEA forecast, coal production in the United States, the European Union, Indonesia and Russia will decline from 2022 to 2025, and there will be a net reduction in global coal supply. Although high coal prices have stimulated some maintenance capital expenditure, there is no sign of acceleration of green space projects. However, there was a counterattack in demand, as the war between Russia and Ukraine forced Europe to switch from gas to coal to boost coal demand. Domestically, although the National Development and Reform Commission has asked for an increase in production and guaranteed supply, enterprises are not willing to spend capital at the micro level.

We judge that the oil price center has risen from about 50-60 US dollars per barrel in previous years to about 70-80 US dollars per barrel; China's coal price has risen from about 500,600 yuan per ton in previous years to about 1000 yuan per ton, and the market has basically formed a consistent expectation.

Logic 2: the pattern of domestic refining and chemical market is improved, and double carbon enhances the scarcity of assets.

Under the influence of the policy, in the next three years, we expect domestic aromatics production capacity to stagnate, olefin growth to slow, and even slightly negative production capacity of refined oil products.

The notice of the carbon Dafeng Action Plan by 2030 clearly requires that by 2025, the primary processing capacity of domestic crude oil will be limited to less than 1 billion tons, and the capacity utilization rate of major products will be raised to more than 80 percent. Since 2021, no new refinery projects have been approved in China, which means that the growth of domestic aromatic PX capacity will enter a stagnant period and the supply pressure will be significantly alleviated.

In terms of ethylene, there is still some new production capacity to be put into operation, and the speed has slowed down significantly. After the energy consumption of raw materials is not included in the double-control assessment of energy consumption, the approval margin of ethylene project is relaxed, and the pressure of ethylene supply still needs some time to be alleviated.

In terms of oil products, considering that the overall crude oil processing capacity does not increase, the new ethylene projects are oil conversion, which may lead to a slight negative increase in oil production capacity. As the recovery of the epidemic brings about the recovery of travel demand, the relationship between supply and demand of oil products may tighten.

Rectify the consumption tax and improve the competitive environment of the oil products market.

The state began to strengthen the rectification of the consumption tax issue since 2021. "starting from June 12, 2021, import consumption tax will be levied on some refined oil products as naphtha or fuel oil. Light circulating oil, mixed aromatics and diluted asphalt usually contain more aromatics or bitumen and are generally not used as fuel. In recent years, a small number of enterprises import a large number of fuel, processing and production is not in line with national standards, flowing to illegal operating channels, endangering the fairness of the refined oil market, there are greater hidden dangers of social security, resulting in environmental pollution. In order to solve these problems, the relevant products have been included in the scope of consumption tax. "

The investigation and rectification of individual enterprises has also been significantly increased. In early 2022, the Liaoning Provincial Taxation Bureau investigated and dealt with the case of Bora and other enterprises evading consumption tax on refined oil products.

Specifically, we think that the rectification of the refined oil market may be beneficial to the refineries and sales sectors of China Petroleum & Chemical Corp and Petrochina Company Limited, and may improve the refined oil processing price difference and the terminal price arrival rate.

Logic 3: attach importance to dividend repurchase

In terms of dividends, central energy enterprises have strengthened their dividends in recent years.As far as oil and gas companies are concerned, the dividend yield in 2021 is significantly higher than that in 2016. In 2021, 56% of CNOOC's operating cash flow was spent on capital expenditure and 40% on dividends, accounting for the highest share of dividends, mainly due to special dividends on the 20th anniversary of listing, with a dividend yield of 7.4%. China Petroleum & Chemical spends 64 per cent on capital expenditure and 25 per cent on dividends, but China Petroleum & Chemical has the highest dividend yield, reaching 11.1 per cent in 2021. Petrochina spends 78 per cent on capital expenditure and only 12 per cent on dividends. The amount and yield of dividends have risen steadily in recent years, reaching 4.6 per cent in 2021.

On the other hand, the operating cash flow of coal companies uses a higher proportion of dividends (compared with oil and gas companies). In 2021, China Shenhua Energy had the highest share of cash dividends, accounting for 53 per cent of his operating cash flow and used 25 per cent of his cash flow for capital expenditure, with a dividend yield of 11.3 per cent.

In terms of dividends, we expect the future dividend yields of several central energy enterprises (China Petroleum & Chemical, China Shenhua Energy, CNOOC, Petrochina) to be around 6-10%. And China Petroleum & Chemical (Ajuh) and CNOOC Limited (H) have repurchase and dividend behavior respectively.

In terms of share buybacks, CNOOC Limited (H) began to buy back Hong Kong shares on September 13, 2022, with a total of 70.692 million shares, totaling HK $694 million, with an average repurchase price of HK $9.82 per share. China Petroleum & Chemical (A) has completed the repurchase and cancellation of 442.3 million shares with an average repurchase price of 4.27 yuan per share, which was cancelled on December 30, 2022; China Petroleum & Chemical (H) began repurchase on September 21, with a total repurchase of 732.5 million shares in 2022, totaling about HK $2.5 billion, with an average repurchase price of about HK $3.40 per share.

Conclusion:Central energy enterprises, ROE relatively high CNOOC, China Shenhua Energy, PB valuation has been repaired to about 1.5 times, but compared with international oil companies may have some room for repair. At present, the PB valuations of China Petroleum & Chemical and Petrochina are still significantly lower than 1, and the valuations of the two companies are expected to usher in a round of repair in recent years as the business environment improves, as well as bottom-up efforts to reduce costs, and pay more attention to dividend repurchase.

Edit / lambor