Source: CICC Research

On the evening of February 17, Beijing time, the website of the China Securities Regulatory Commission published the "trial measures for the Administration of overseas issuance and listing of Securities by domestic Enterprises" (hereinafter referred to as the "Management trial measures"), and simultaneously issued relevant supporting regulatory guidelines. On the whole, on the basis of nearly 30 years' development experience, this new regulation is a further systematic optimization of the relevant rules issued in 1994 and 1997 respectively, especially in response to the new changes and new situation of the domestic and foreign capital market environment in recent years, which is of positive significance for Chinese enterprises to integrate into the global market and make full use of the two markets and two kinds of resources. Based on the latest developments, we sort out the important contents of the "Management trial measures" and interpret the possible impact.

Details of the new regulations: unified supervision to fill in the gaps, negative list to increase inclusiveness, record management optimization process

► scope: implement unified filing management for overseas listing and issuance activities and fill in the gaps.

Unified management of overseas issuance and listing activities, including direct and indirect overseas listing of domestic enterprises, will help to fill the previous regulatory gaps and deficiencies. The trial measures for Administration unify the management of direct and indirect overseas issuance and listing activities, including 1) overseas issuance and listing of joint stock limited companies registered in China ("H-share listing"), and 2) enterprises whose main business activities are in China, in the name of enterprises registered abroad, overseas issuance and listing based on the equity, assets, income or other similar rights and interests of domestic enterprises ("red chip listing"). At the same time, make clear the identification standard of indirect overseas issuance.Follow the principle that substance is more important than form.To judge based on the operating indicators such as revenue and profit within the enterprise and the place of operation (for example, more than 50% of assets, income or profits are in China, senior managers are in China, etc.).

The new rules cover various types of transactions, such as refinancing and secondary listing of listed and listed companies. In addition to the initial public offering, the new rules also include the subsequent issuance of listed companies (convertible bonds, exchangeable bonds, preferred shares, etc.), overseas issuance and listing after delisting, and after overseas issuance and listing. Secondary listing or major listing in other overseas markets, conversion of listing status after overseas listing (such as secondary listing to dual major listing), conversion of listing plate, issuance of securities to purchase assets, etc. However, it does not include the issuance of securities for the implementation of equity incentives, the conversion of provident fund to increase the company's capital, the distribution of stock rights, the subdivision of shares, and so on.

► form: strengthen domestic and foreign regulatory cooperation, clear regulatory boundaries

Strengthen the supervision after the event, strengthen the coordination of inter-agency supervision and coordination at home and abroad. The record management system as a whole adheres to the principles of supervision according to law, scientific supervision and moderate supervision. Domestic supervision reform mainly includes: 1) defining supervision responsibilities and strengthening supervision coordination mechanism.We will implement a regulatory system dominated by the CSRC, and at the same time strengthen the convergence of policy rules, regulatory coordination and information sharing among various agencies.2) improve the regulatory means, measures and legal responsibilities, and clarify the reporting requirements for major issues after overseas listing and issuance. In addition, we will improve cross-border securities regulatory cooperation arrangements, strengthen cross-border securities regulatory and law enforcement cooperation with overseas securities regulatory agencies, and jointly crack down on cross-border violations through mechanisms such as filing and communication.

We believe that this institutional reform has the following significance: 1) improve the regulatory system to ensure that domestic securities supervision is neither "absent", nor "offside" or "misplaced", improve regulatory efficiency, ensure regulatory "reign", and avoid regulatory generalization. 2) problems such as the unsmooth flow of information and the complexity of cross-border regulatory cooperation have previously caused great obstacles to the supervision of overseas enterprises in China, and improving cross-border regulatory cooperation will help to improve the difficult problem of cross-border supervision. 3) improving the regulatory rules does not mean tightening the overseas listing policy; on the contrary, it provides enterprises with more flexible and independent choices under the premise of regulation, such as explicitly allowing overseas listing of VIE framework enterprises that meet the compliance requirements, and giving enterprises more flexibility in refinancing, full circulation and currency management.

► mode: implement the record management system and set up the negative list

Change the license management to record management, clarify the record requirements, and embody the management principle of "release management and service". Previously, the approval system was adopted for the direct overseas listing of domestic enterprises, and the "Management trial measures" cancelled the pre-examination and approval process of the CSRC and changed it to a post-filing management system. at the same time, domestic enterprises that are indirectly listed overseas will be brought into the filing system for supervision. The use of ex post filing system will help to optimize the process and help enterprises to complete the listing process more efficiently. In addition, the new regulations unified and standardized filing management, so that filing materials will be more focused on compliance, but also more concise and transparent.

The negative list and other systems explicitly prohibit the situation, but at the same time relax the restrictions on the issuing object. The new rules follow the principle of minimum and necessity, and clearly define the circumstances in which overseas listing and financing are prohibited and security review procedures need to be carried out before applying, such as those explicitly prohibited by laws and regulations or by the state, or which may endanger national security, involve crimes or major violations of laws and regulations, or where there are major disputes, it is stipulated that overseas listing shall not be allowed. In addition, documents such as the "Special Management measures for Foreign Investment access (negative list) 2021 Edition" jointly issued by the National Development and Reform Commission and the Ministry of Commerce should be followed. However, in addition to this, it does not set additional thresholds and conditions for overseas listing, and relaxes it at a certain level after fully considering the different development needs of enterprises. For example, under specific circumstances such as equity incentives and issuing securities to purchase assets, domestic enterprises are allowed to issue securities to specific domestic objects when they are issued and listed abroad directly; allow domestic unlisted non-tradable shares to be converted into overseas listed shares and circulate on overseas exchanges ("full circulation"); relax currency restrictions and allow funds to be raised in RMB, dividends and so on.

► process: unified process, standardized communication, smooth transition of stock increment.

Unifying and streamlining the filing process of overseas issuance and listing will help enterprises to reasonably manage expectations and arrange time windows. According to the new regulations, domestic enterprises issued and listed abroad are required to put on record with the CSRC in accordance with the guidelines of the new regulations, and submit filing reports, legal opinions and other relevant materials. The domestic supervision part of the overseas listing process includes: 1) preparation and communication in advance (examination and approval by industry competent departments, safety assessment review by relevant departments); 2) filing with China Securities Regulatory Commission within 3 working days after submitting overseas listing application documents; 3) CSRC approves and responds to relevant opinions, and issuers submit supplementary materials. 4) if there is no problem, the CSRC shall complete the filing and publicize it within 20 working days from the date of receipt of the materials. At the same time, after the red chips submitted the A1 listing application process to the Hong Kong Stock Exchange, the China Securities Regulatory Commission filing process was added, while H shares cancelled the declaration and acceptance process to the China Securities Regulatory Commission, and were unified into the same China Securities Regulatory Commission filing process as red chips. In addition, the No. 2 and No. 3 guidance documents of the new regulations standardize the content and format of enterprise filing materials.

Ensure the steady and orderly progress of filing management, and put forward filing arrangements for stock and incremental enterprises. For the stock enterprises that have been issued and listed abroad, it is not required to put on record immediately, but can be put on record as required if the subsequent filing matters such as refinancing are involved. For domestic enterprises that have been approved by overseas regulatory authorities or overseas stock exchanges, but have not completed indirect overseas issuance and listing, a six-month transitional period shall be granted. A company that completes overseas issuance and listing within 6 months shall still be regarded as a stock enterprise. If the above-mentioned domestic enterprises need to re-complete the issuance and listing procedures within 6 months or fail to complete overseas issuance and listing within 6 months, they shall put on record as required.The establishment of a communication mechanism for the filing of overseas issuance and listing will help to improve the efficiency of filing.The No. 4 guidance document of the new regulations draws lessons from Hong Kong's pre-listing consultation and communication system to a certain extent, clarifying the contents and methods that can be communicated at all stages of filing, including various issues such as the regulatory policy of the issuer's industry and the ownership of the scope of filing, and stipulates that the filing management department will not accept communication applications during the quiet period. The establishment of the filing communication mechanism can not only standardize the filing communication behavior, but also help to improve the overall filing efficiency.

Hot issue of ►: can companies with VIE structure still be listed overseas?

The new regulations on overseas listing do not prohibit overseas listing of VIE-based enterprises, and new verification requirements are added. In view of the overseas issuance and listing of enterprises under the VIE framework, record management adheres to the principles of marketization and the rule of law, and strengthens the coordination of supervision. In response to a reporter's question, the person in charge of the relevant departments of the CSRC clearly stated that "the CSRC will solicit the opinions of the relevant competent departments and put on record the overseas listing of VIE-based enterprises that meet the compliance requirements." At the same time, the verification requirements for the ownership structure and control structure in the No. 2 guidance document states that if the issuer has an agreement control structure, it should be verified and explained in the following aspects: 1) the participation of foreign investors in the operation and management of the issuer, for example, sending directors, etc.; 2) whether there are domestic laws, administrative regulations and relevant provisions that no agreement or contractual arrangements can be used to control business, license, qualification, etc. 3) whether the domestic operators controlled by the agreement control framework arrangement fall within the scope of foreign investment security review, and whether they involve the areas of foreign investment restrictions or prohibition.

The significance of the new rules: make clear the rules to reduce policy uncertainty, strengthen multi-party regulatory cooperation, dredge enterprise financing channels, and promote the further opening of the capital market.

► makes clear rules to reduce policy uncertainty: the new rules regulate all types of offerings and trading behaviors of domestic enterprises listed abroad, and specify relevant rules, procedures and communication arrangements. Further improvement and detailed requirements have been made from the aspects of regulatory scope of issuance and listing, pre-listing filing, post-disclosure of information, subsequent refinancing dividends and share changes, as well as cross-border regulatory cooperation. So that enterprises have evidence to rely on in the process of overseas listing. It helps to avoid all kinds of chaos from the source, greatly reduce the uncertainty at the policy level, and maximize the protection of the interests of issuers, investors and other market participants.

The improvement of cross-border regulatory cooperation arrangements by ► may be conducive to further cooperation between China and the United States in audit supervision. The new regulations mention that it will improve cross-border securities regulatory cooperation arrangements and strengthen cross-border securities regulatory law enforcement cooperation with overseas securities regulatory agencies. On August 26 last year, China and the United States signed an agreement on cooperation in audit supervision, and on December 15 last year, the Accounting Supervisory Board of listed companies (PCAOB) confirmed that they could obtain unfettered review authority for accounting firms in mainland China and Hong Kong. The new rules define future regulatory cooperation arrangements, which may lay the foundation for further regulatory cooperation between China and the United States, thereby reducing the risk of delisting of Chinese-listed companies in the future.

Overseas issuance of ► may gradually return to the right track and dredge overseas financing channels for enterprises. Since mid-2021, the pace of domestic companies listing in the United States has slowed down significantly. We believe that the landing of the new regulations and the relevant regulatory details will help enterprises get back on track for overseas issuance. At the same time, the new rules follow the principle of minimum and necessity, which not only provides enterprises with more flexible and independent choices under the premise of norms, but also helps domestic enterprises to dredge overseas financing channels.

► promotes the further opening of the capital market at a high level. The report of the 20th CPC National Congress proposed to "promote a high level of opening up to the outside world." at the end of last year, the Central Economic work Conference stressed that "greater efforts should be made to attract and utilize foreign capital." the opening up of the capital market is an important part of it. In recent years, China has continuously strengthened the two-way circulation of the capital market through the mechanisms of interconnection, QFII/RQFII and QDII/RQDII. By standardizing the overseas listing of domestic enterprises, it is beneficial for Chinese enterprises to go to overseas financing more directly, and help China's capital market to further open, which also means that global investors have more opportunities to share the dividend of China's economic development.

► 's position as a Hong Kong financial center and RMB bridgehead is expected to be further consolidated. Hong Kong has developed into an international financial center around China's economy and assets, and Hong Kong stocks have formed a unique "Chinese assets + foreign capital" model. In the current new international situation, listing in the United States is still a major option, but the attractiveness of the Hong Kong market is also increasing, and we expect that more and more Chinese companies will also choose to return to Hong Kong stocks through secondary listing or dual major listing. In the future, the listing of more Chinese enterprises in Hong Kong will help to optimize the structure of the Hong Kong stock market, attract more capital precipitation, form positive feedback from high-quality companies and funds, and further consolidate Hong Kong stocks' position as a global financial center. At the same time, the new rules also mention relaxing currency restrictions to help internationalize the renminbi. At present, Hong Kong has the largest pool of RMB funds outside mainland China, and its status as a bridgehead for RMB internationalization is expected to be further strengthened.

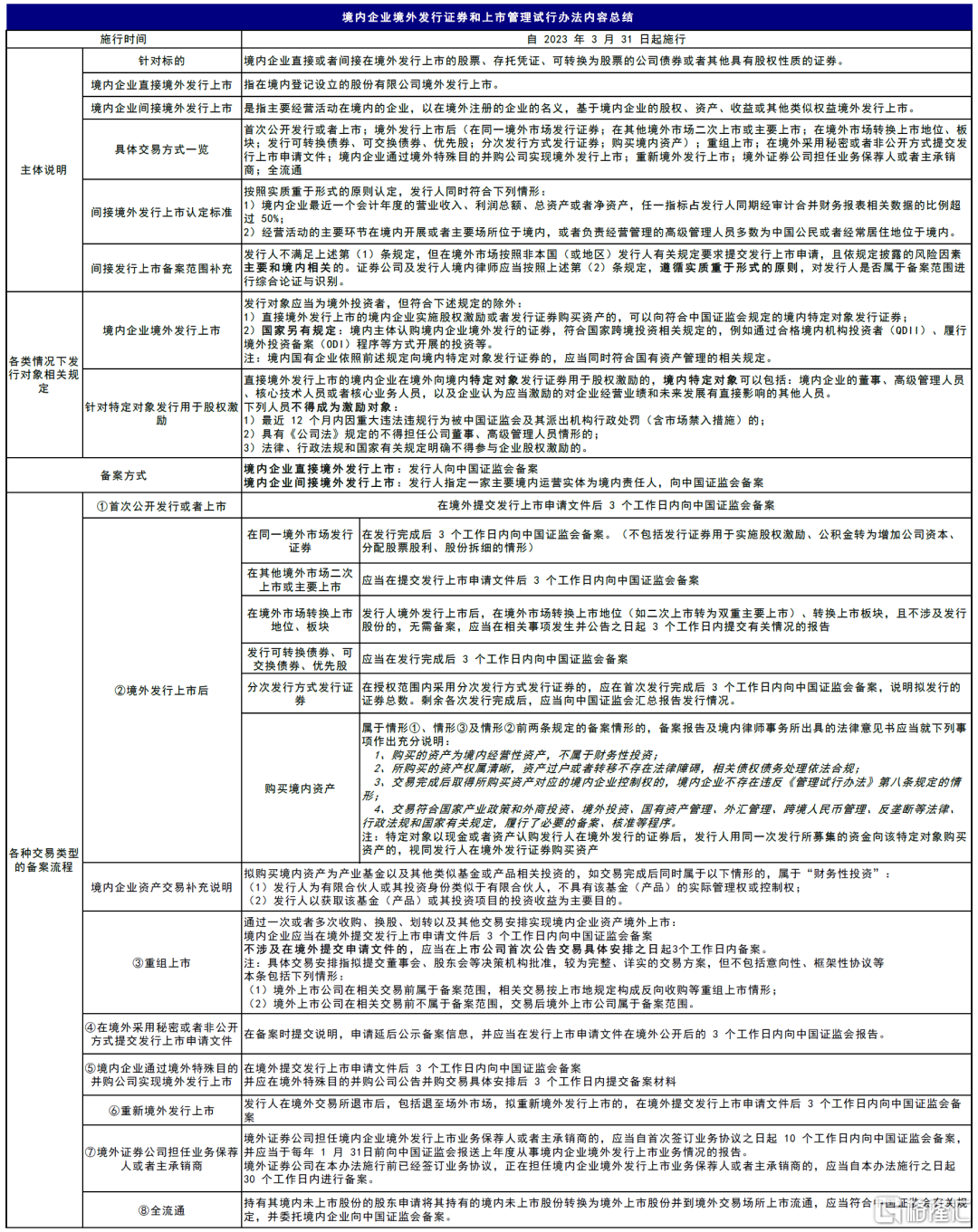

Chart 1: summary of the contents of the trial measures for the Administration of overseas issuance and listing of domestic Enterprises (1jump 2)

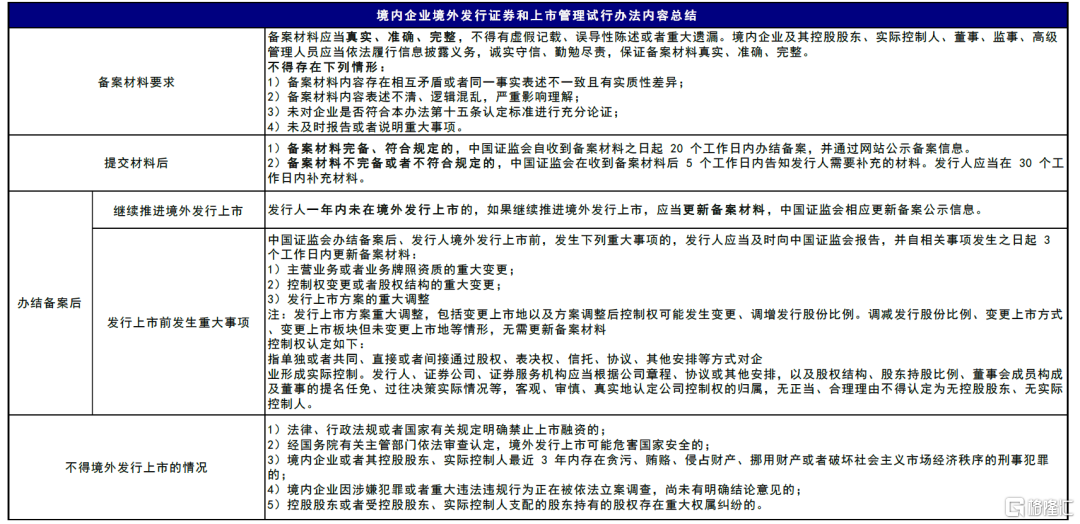

Chart 2: summary of the contents of the trial measures for the Administration of overseas issuance and listing of domestic Enterprises (2jump 2)

Figure 3: key points for verification of special legal opinions

Figure 4: verification requirements for ownership structure and control structure

Figure 5: record communication mechanism

Edit / ruby