Authors: pan Xiangdong, Liu Juanxiu, Xing Shuguang, Chen Yunyang

Source: new era Macro

Text

After the Lantern Festival, ushered in the peak season of construction, electricity demand increased, industrial production in March or reverse the downward trend to achieve expansion. In addition, affected by the dislocation of the Spring Festival, export growth in March may pick up significantly compared with January-February, which will also support industrial production to a certain extent, but this is not sustainable. Domestic demand remains weak in March, although the growth rate of infrastructure investment is likely to continue to pick up, but the growth rate of new real estate starts slows and the growth rate of real estate investment may fall at a high level; due to the slowdown in the profits of early industrial enterprises and weak terminal demand, manufacturing investment growth is also likely to decline. In addition, the growth rate of automobile consumption may slow down, coupled with the weakening year-on-year growth rate of commercial housing sales area in the early period, which is a drag on the consumption related to the production chain, and the social zero growth rate may decline. The prices of vegetables and pork have risen sharply since March, and the year-on-year growth rate of CPI may pick up significantly with the start of the pig cycle. The economy has not yet stabilized, broad credit is still on its way, and with seasonal effects, credit and social finance are expected to pick up sharply.

A Review of the Economic situation in March

1.1 supply expanded but demand weak in the start season

The Lantern Festival is followed by a peak start season. According to high-frequency data, supply expanded in March, but demand was weak.

The upstream supply is expanding.After the enterprises returned to work, the demand for electricity increased, and the coal consumption for power generation increased by 33.7% month-on-month in March (as of March 22), which was significantly higher than that in February (- 30%). Although the heating season ended on March 15, areas such as Tangshan were severely criticized by environmental protection officials, causing the average blast furnace operating rate to fall from 65.72% in February to 63.61% in March. On the whole, the supply of upstream industry is expanding.

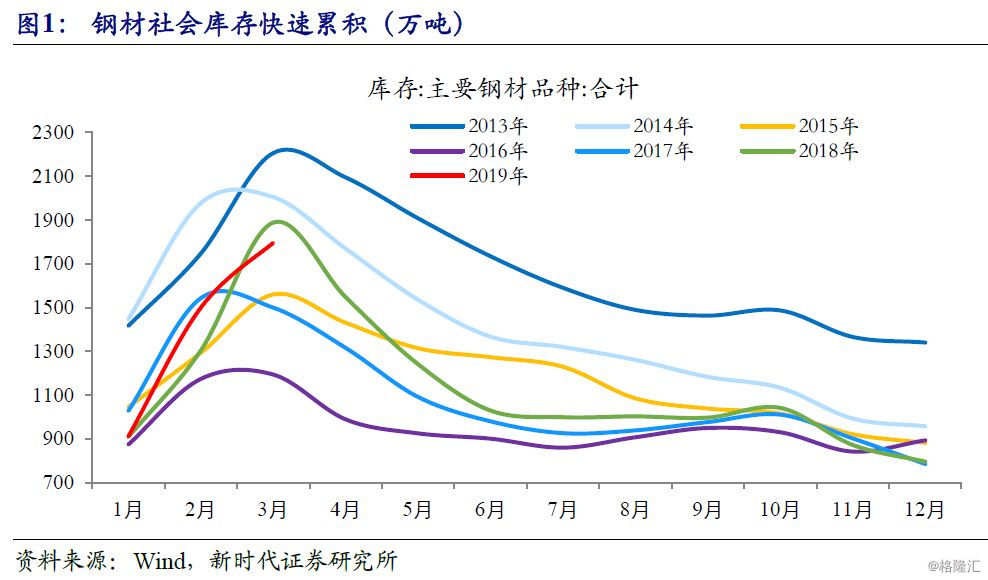

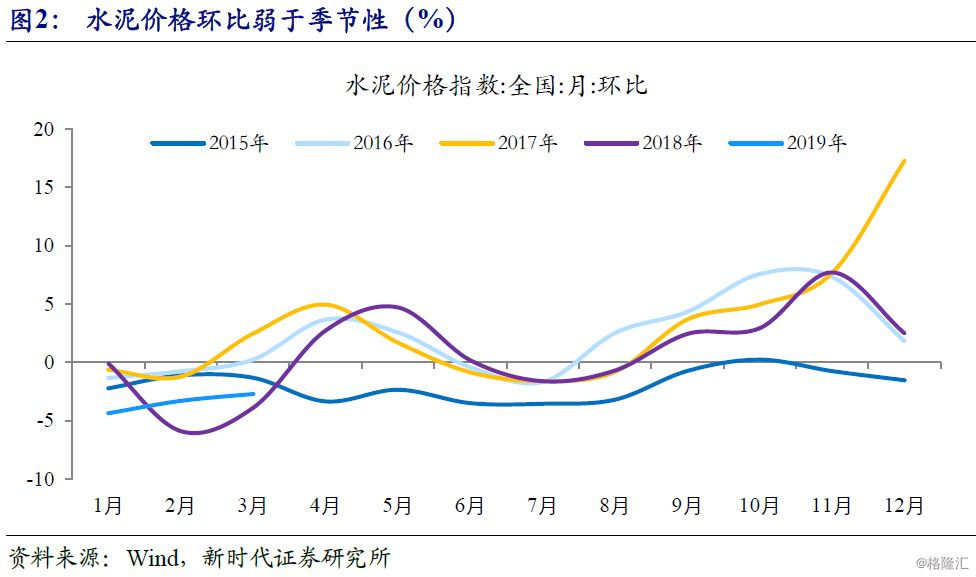

The rapid accumulation of steel stocks in the middle reaches and the weaker than seasonal cement prices mean that demand is not strong.Since 2019, the social inventory of steel has accumulated rapidly, and in recent years, the accumulation rate is only slower than that in 2018, and the trend of rebar prices is weakly fluctuating. At the same time, the month-on-month growth rate of cement prices in March is weaker than seasonal, which means that demand may not be strong.

Downstream demand differentiation.Since March (as of March 15), passenger car retail has fallen 21% from a year earlier, expanding from January to February (- 9.7%), and the growth rate of car consumption may slow. The area of commercial housing sales rebounded seasonally, and the month-on-month growth rate was basically seasonal, but affected by the dislocation of the Spring Festival, the year-on-year growth rate rose from 8.3% to 14%.

1.2 funds have been tightened

Since March 2019, the maturity of reverse repurchase is 300 billion yuan, and the maturity of MLF is 431.5 billion yuan. Affected by the tax period and other factors, the total liquidity of the banking system has declined but is still at a reasonable and adequate level. The central bank has reduced the amount of open market investment, with a total net return of 582.5 billion yuan (including treasury cash). The interest rate centre of the money market rose in March from February, with the DR007 average rising from 2.43 per cent to 2.53 per cent. The average score of R007 rose from 2.58 per cent to 2.6 per cent, and the 1W average rose from 2.5 per cent to 2.57 per cent.

1.3 the repair of risk preference in capital markets is coming to an end.

Global market risk appetite has been repaired since the beginning of the year, and risk assets have overfallen and rebounded, but asset price volatility has intensified as the risk appetite repair comes to an end.

Stock market range volatility:Since March (as of March 22), the Shanghai Composite Index has closed up 5.55%, but basically fluctuated in the range of (3000yuan 3100). The implied risk premium of Shanghai A-shares fell from its peak in early January, accelerated in February and narrowed in March. Risk appetite repair or near the end.

Bond market picks up:At the end of the data vacuum, China's economy has not yet stabilized, at the same time, policies from overseas central banks have turned loose, the Fed's FOMC meeting in March is partial to pigeon, and US bond yields have fallen sharply, taking the lead in breaking through the horizontal market situation. China's monetary policy space has further opened up, the bond market has warmed up, and the yield on 10-year Treasury bonds has returned to around 3.1%.

RMB exchange rate is stable:The spot exchange rate of RMB against the US dollar was 6.7183 on February 22nd, little changed from 6.7105 at the end of January, and the RMB exchange rate was stable. The monetary policy of the global central bank has turned loose, the PMI of developed economic systems such as Europe, the United States and Japan has been declining, the world has entered the "gap link", the rising resistance of the US dollar has increased, and the pressure of RMB depreciation has been alleviated.

Forecast of economic data in March

2.1 Export-led supply expansion

The growth rate of industrial value added rebounded from the same period last year:According to the high-frequency data of production indicators, the year-on-year growth rate of coal consumption for power generation increased from-10.4% in January to February to 3.17% in March 2019, while the growth rate of blast furnace operation decreased from 2.3% to 0.81%. At the same time, affected by the Spring Festival effect, export growth in March is likely to pick up significantly compared with January-February, which will lead to an increase in manufacturing value-added growth compared with the same period last year. Taken together, the growth rate of industrial production is expected to pick up to 6.4% year-on-year in March.

2.2 weak domestic demand

Cumulative decline in investment in fixed assets compared with the same period last year:In terms of infrastructure investment, the cumulative growth rate of newly signed contracts in China's construction industry rebounded sharply to 13.5% from January to February 2019, and the project approval of the National Development and Reform Commission accelerated, and the growth rate of infrastructure investment is expected to continue to pick up from January to March. In terms of real estate investment, the previous land transaction slowed down, and the growth rate of land purchase fees may continue to decline. The recovery in the growth rate of construction area from January to February is related to the low completed area in 2018, and the subsequent growth rate may slow down with the new construction. As a result, the growth rate of investment in Jian'an project is lowered, and the high growth rate of real estate investment from January to March is expected to decline. In terms of manufacturing investment, due to the slowdown in the profits of industrial enterprises and weak terminal demand, the growth rate of manufacturing investment is likely to decline from January to March. Taken together, the growth rate of fixed asset investment from January to March may drop slightly to 5.9%.

The total volume of retail sales of consumer goods decreased compared with the same period last year:Since March (as of March 15), passenger car retail has fallen 21% from a year earlier, expanding from January to February (- 9.7%), and the growth rate of car consumption may slow. The growth rate of the sales area of commercial housing in the early period was weaker than the same period last year, which was a drag on the consumption related to the production chain. However, CPI growth is likely to pick up significantly in March, with price factors supporting zero growth. Taken together, zero growth is expected to fall to 7.8% in March.

Exports rebounded year-on-year:The Spring Festival of 2018 falls on February 16, and the effect of reducing exports after the festival is shared in March, driving down the amount of exports in March 2018. While the Spring Festival in 2019 falls in early February, the effect of reducing exports after the festival basically falls in February, and the amount of exports in March may pick up significantly, superimposing the impact of a low base, and exports are expected to increase by 15% in March compared with the same period last year.

Year-on-year decline in imports:After the festival, enterprises replenish inventory and increase imports, and the misalignment of Spring Festival may lead to a weaker import volume in March 2019 than in the same period in 2018. Judging from the start season, demand is relatively weak, while the continued decline in the growth rate of South Korean exports to China may indicate weak domestic demand in China, but the rebound in commodity prices supports the amount of imports and increases in volume and prices. Import growth is expected to be-13% in February.

2.3 the economy has not yet stabilized

Year-on-year growth rate of GDP goes down:The supply and demand of economic data from January to February are both weak. According to the above forecast, domestic demand in the peak season of work in March is still weak, reflecting that the economy has not yet stabilized, but it also rules out the possibility of a short-term rapid decline. GDP growth in the first quarter is expected to slow slightly to 6.2%. 6.3%.

2.4 Pig cycle starts and inflation goes up

CPI rebounded year-on-year:The prices of vegetables and pork rose more than 15 percent year-on-year in March, driving up CPI growth by about 0.8 percent. Pork prices are likely to rise sharply in the last week of March as the pig cycle begins, superimposed from a low base, and CPI growth may significantly rebound to 2.7 percent.

PPI rose year-on-year:The month-on-month growth rate of the commodity price index (BPI) rose from-0.16% to 0.13% in March. The Commodity supply and demand Index (BCI) of the Business Society rose 0.69 per cent to 0.18 in February, and the PPI growth rate is expected to continue to rise to 0.02 per cent in March. According to the possible year-on-year error (the error in the latest February is about 0.2 percentage points), the PPI is expected to grow 0.3 per cent year-on-year in March.

2.5 Social integration and super-seasonal expansion of credit

M2 year-on-year decline:Although in the context of broad credit, RMB loans and corporate bond financing may increase more than the same period last year, thus driving up the growth rate of M2 compared with the same period last year, the scale of local special bond issuance rebounded in March compared with February, which may lead to the conversion of general deposits into fiscal deposits, thus slowing down the growth rate of M2 compared with the same period last year.

New RMB loans increased compared with the same period last year:Under the influence of the Spring Festival, credit increased less seasonally in February, and the amount of new credit in March will rise seasonally. According to the data of the Stock Exchange, the acceptance and discount of bills in March (as of March 22) increased slightly compared with February. Taking into account the wide credit background, new RMB loans are expected to increase by about 1.3 trillion yuan in March.

New social integration increased compared with the same period last year:Affected by the seasonal effect, the scale of credit expanded in March, and the data of the Stock Exchange showed the expansion of off-balance sheet bill financing. Wind data showed that the issuance of local special bonds rebounded in March compared with February, and the increase in social finance was expected to be 1.45 trillion yuan in March.

Prospect of capital market in April

3.1 overseas market risk off, A shares fluctuate or aggravate

March 22, March manufacturing PMI in Europe and the United States were significantly lower than expected, triggering 10-year and three-month Treasury yields upside down, which is the first time since the financial crisis, US stocks have plummeted and are likely to continue to weaken for some time to come. The weakness of US stocks may mean that overseas markets have converted from risk on to risk off since the beginning of the year, and the volatility VIX will rise, which may have an impact on A-shares. At the same time, A-share valuations have been repaired, with the end of the data vacuum, A-share logic returned to fundamentals, the data show that the economy has not yet stabilized. As a result, short-term A-shares may change from a general rally to a structural market, but short-term fluctuations may not change the long-term upward trend.

3.2 the bond market is expected to break through its previous lows

The bond market is expected to break through its previous lows.First, overseas market risk off, US debt is popular, US debt long-end interest rate is down, Chinese Treasury bond long-end interest rate may follow; second, the world has entered the "gap link", China's monetary policy space is open, while monetary policy gives priority to employment, short-term monetary policy will continue to be loose, liquidity is reasonable and abundant. Third, the main body of this round of wide credit is private enterprises, which does not stimulate real estate and infrastructure as much as before, the process of wide credit is long, and the pattern of liquidity trap remains unchanged; fourth, the economic downward pressure brought about by exports and real estate investment still exists.

There may be two obstacles for the bond market to break through its previous lows.First, soaring piglet prices and the return of "pig inflation" in the future may trigger inflation expectations or even stagflation expectations to rise again; second, 10-year Treasury yields have fallen sharply since 2018, and their absolute yield space is low. Institutions may struggle to enter the market.