Author: Jiang Chao

Source: Jiang Chao Macro Bond Research

Abstract

一、Global easing cycle resumes

Since the beginning of 19 years, there has been a new round of easing in global monetary policy.

The United States suspends raising interest rates.

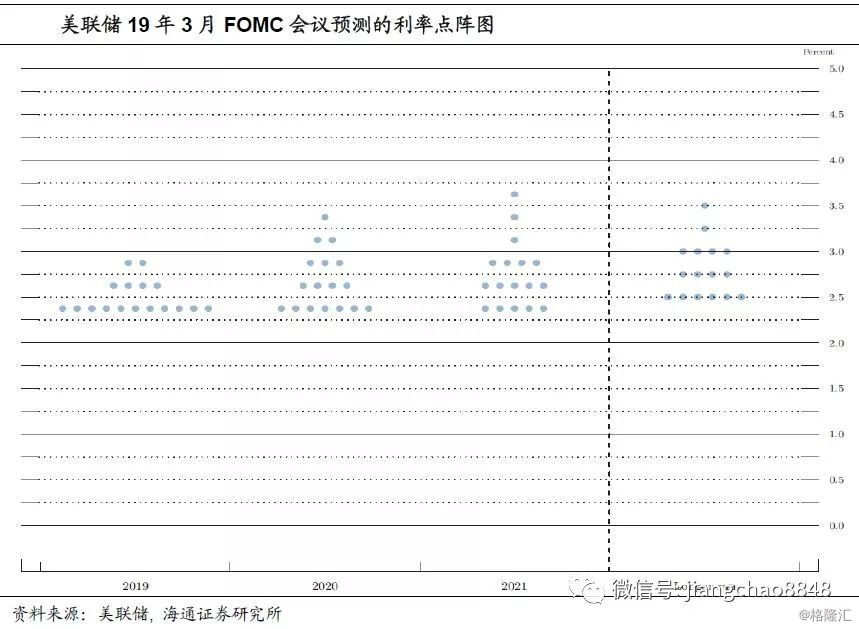

At last week's meeting, the Fed announced a moratorium on raising interest rates, and the bitmap released at the meeting shows that most Fed members believe that the Fed will not raise interest rates in 2019 and that there will be only one increase in 2020. Earlier, at the interest rate meeting in December, most members thought that interest rates would be raised twice in 19 years. At the same time, the Fed announced that it would end the contraction in September.

Interest rate cuts have even been expected in the futures market, and the probability of a December rate cut corresponding to the federal funds rate futures data has exceeded 50%.

ECB restartsTLTRO。

At its interest rate meeting in early March, the ECB announced that it would begin a two-year targeted long-term refinancing operation (TLTRO) in September and revised its forward guidance on interest rate hikes, which is expected to remain unchanged until the end of 2019, a further delay from the previous summer of 2019.

Japan continues to ease.

In the United States and Europe, at least in the past, they have experienced varying degrees of austerity, the United States withdrew from the QE and continued to raise interest rates, and the European Central Bank withdrew from the QE at the end of 18 years. By contrast, Japan left the benchmark interest rate at-0.1 per cent and the 10-year bond rate at 0 per cent at the latest interest rate meeting, and will buy JGBs at a rate of 80 trillion yen a year.

In other words, the Bank of Japan's exit from QE and negative interest rates are a long way off.

India resumes interest rate cuts, with many countries hinting at interest rate cuts.

In 2019, the Reserve Bank of India became the first central bank to announce an interest rate cut, announcing on February 7th that it would cut the benchmark repo rate by 25bp to 6.25%. India has raised interest rates twice in the past year and a half. The Bank of India said headline inflation is expected to remain moderate in the short term, providing room for interest rate cuts.

Subsequently, the Bank of Egypt also announced a cut in interest rates 100bp on February 15th.

In Argentina, after 18 years of currency crisis, its benchmark interest rate soared to 60%, but the 60% floor was removed at the end of 18 years, and interest rates have fallen to about 40% since 19 years.

In addition, a number of central banks have recently hinted at the possibility of cutting interest rates. For example, the Reserve Bank of Australia issued a statement in February that slashed its economic growth forecast and hinted at an increase in the probability of future interest rate cuts, while previous rate-raising statements were more likely to raise interest rates than to cut them.

The market also expects Turkey, Poland, the Philippines and other countries to start cutting interest rates in 19 years.

Since the end of 2014, global monetary policy has entered a tightening cycle as the Fed withdrew from the QE, which in turn launched a cycle of raising interest rates. Now that the US interest rate hike cycle is coming to an end, the global monetary tightening cycle may be over and a new round of easing may be in the future.

Second, what is loose, more money or low interest rates?

However, the talk of a new easing cycle is not true for some economies.

For example, Japan and the euro zone, whose benchmark interest rates have been around zero during the last global tightening cycle, have not gone through the same cycle of rate hikes as the United States, and since they have not tightened, there is no talk of a new round of easing.

The question is? Why do Japan and the euro zone keep interest rates at zero or even negative? Isn't it loose enough that interest rates are all negative? Since it is already very loose, why has it not worked?

The reason is that easing actually has two meanings: low interest rates are only one aspect, and on the other hand, it is the amount of money, which, in popular terms, is also more money.

Japan and Europe: low interest rates but lack of money.

But in Japan and the euro zone, it is precisely the amount of money that is wrong, with low interest rates but no money. In japan, its broad money M3 has grown at an average rate of only 2% over the past 20 years. Although the euro zone is slightly stronger than Japan, its broad money M3 has grown at an average rate of only 3% over the past decade.

In other words, although the money in Japan and the euro zone is very cheap, people still do not want to borrow money, and the money cannot flow, so the money is stored in the hands of the central bank. For example, the total assets of the Bank of Japan have reached 560 trillion yen, exceeding Japan's GDP, but Japan's broad money M3 is 1343 trillion yen, which is only double the total assets of the Bank of Japan, which means that the whole society is actually very short of money.

Emerging markets: high interest rates but a lot of money.

In emerging markets, high interest rates are often the norm. For example, interest rates in Argentina can be as high as 60%, while interest rates in India are still as high as 6.25%, much higher than in the United States, Japan and Europe.

In our impression, high interest rates must mean a shortage of money, but on the contrary, emerging markets tend to have the least shortage of money. In Argentina, for example, its broad money M3 has grown by an average of 36% after 1990, equivalent to doubling its monetary output every two years or so. In more extreme countries such as Venezuela, the total amount of money will increase many times in a year.

In theory, these emerging market countries have so much money, so liquidity should be very loose, but what we see is that Argentina has a currency crisis every few years, often relying on external bailouts such as IMF to survive, which shows that monetary easing cannot necessarily be achieved with a lot of money alone.

Thus, although we feel that global monetary policy has ushered in a new round of easing cycle, the answer varies from country to country, some are loose and tight, and some are tight and tight.

Third, Mingsong was tight in the past: there was a lot of money but high interest rates!

China used to have a lot of money.

After the 2008 financial crisis, China's house prices continued to rise, giving people the impression that there is a lot of money, so the main sign of monetary easing in China in the past is a lot of money.

From 2008 to 17, the total amount of broad money M2 in China rose from 40 trillion to 167 trillion, an increase of more than three times, with an average annual growth rate of 15.4%, far exceeding the nominal growth rate of 11.9% of GDP in the same period.

In fact, the broad money M2 far underestimates the total amount of real money in China, because M2 only includes bank deposits, but since 2011, various kinds of shadow banks such as bank wealth management and trust have developed on a large scale. Most of these currencies are not included in bank deposits, but are reflected in the bank balance sheet as other liabilities of banks.

If China's total currency is measured in terms of total bank liabilities, it was only 55 trillion at the beginning of 2008, but by the end of 17 years it had risen to 250 trillion, with an increase of nearly four times in 10 years, with an average annual growth rate of more than 17%. This may be a more real portrayal of China's currency overissue.

But interest rates are also high at the same time.

Although China has not been short of money in terms of quantity in the past decade, the money is not as loose as it seems in terms of interest rates.

From 2008 to 17, the average interest rate on China's 10-year government bonds was 3.6%, while the peak was close to 5%. Since banks can deduct 25% of the corporate income tax when they buy treasury bonds, the average interest rate on open bonds, which is similar to treasury bonds but subject to tax, is 4.2%, while the peak is close to 6%.

National debt and national development bonds are risk-free interest rates, which can only be enjoyed by the government and policy banks. For the whole society, the only way to borrow money is to find a bank, so the loan interest rate can better represent the cost of capital of the real economy. From 2008 to 17, Bank of China Ltd. 's average lending rate was 6.6 per cent, compared with a peak of 8 per cent.

However, the loan interest rate does not represent the real interest rate in China, because of institutional and regulatory reasons, many financing activities of China's local government financing platforms, real estate enterprises and private enterprises cannot borrow directly through banks, but indirectly find bank loans through shadow banks, while non-standard financing costs such as trusts in shadow banks are usually 8-10% or more.

Fourth, it is now tight and lax: there is not much money but the interest rate is low!

There's not so much money now.

After two years of deleveraging, China's currency growth has fallen sharply.

As of February 19, China's broad money M2 grew by 8%, only about half of the average growth rate of 15.4% over the past decade. In terms of the more representative growth rate of total bank liabilities, the current growth rate is only 7.7%, a fraction of the average growth rate of 17.1% over the past decade.

In terms of new money, M2 has grown by an average of 13.8 trillion a year over the past two years, which is only equivalent to the level of increment in 2009 and down from 15 trillion in 2012. In terms of total bank liabilities, the total liabilities of banks increased by 18 trillion in the past two years, compared with an average annual increase of nearly 30 trillion in 15 / 16.

Therefore, whether in terms of the growth rate of the currency or the new increment of the currency, there is actually not so much money in China compared with the past decade!

But interest rates have fallen sharply.

Although there seems to be less money in terms of quantity, it is looser in terms of interest rates.

After deleveraging, China's risk-free interest rate has fallen sharply. The interest rate on 10-year government bonds is now only 3.1%, while the interest rate on 10-year bonds has fallen to 3.6%, which is well below the average level of the past decade and is not far from the lowest level in history.

From the perspective of lending rates, the bank lending rate has fallen to 5.91% at the end of 18 years, and we estimate that it may have fallen to about 5.7% in March 19, which is also much lower than the average of the past 10 years.

More importantly, with the landing of the new rules on asset management, the growth of shadow banks has been restrained, and after blocking the partial door of financing, we have reopened the main door of financing. it has increased the issuance of local government special bonds, replaced the new hidden liabilities of the financing platform, increased the issuance of corporate bonds, replaced the shadow banking financing of real estate enterprises and private enterprises, and whether it is local government bonds or corporate bonds. Their interest rates are much lower than the funding costs of shadow banks.

Therefore, on the whole, the real interest rate in China has dropped significantly, and it is not only reflected in the decline in the interest rate of treasury bonds, but more importantly, the non-standard financing interest rate of shadow banks has dropped sharply.

Why is it so tight and loose? Because the demand for invalid financing has been reduced!

Many people say that they do not understand why interest rates become lower when there is less money. Isn't it supposed to be upside down?

From the micro experience, our experience is that the poor can only borrow money from usury, while the rich can only borrow money cheaply. It is true that the interest rate is high with less money and the interest rate is low with more money. Microscopically, the amount of money is often reflected in the supply of funds, and there is a negative correlation between the supply of funds and the level of interest rates.

But from a macro point of view, the amount of money is not only reflected in the capital supply of banks, but also reflects the capital demand of the economy, which is positively related to the interest rate. The more important significance of our regulation of shadow banking and government hidden debt is to reduce the ineffective financing demand.

We can imagine that if we allow local governments and real estate enterprises to borrow at will, and with the support of the real estate bubble and land finance, the capital needs of financing platforms and real estate enterprises are almost unlimited, and their ability to bear interest rates is also the highest, and if banks can lend to financing platforms and real estate enterprises through various channels, then banks' loan interest rates for other industries will also rise.

However, after limiting the borrowing demand of local governments and real estate enterprises, banks can not find too many channels for high-interest loans, so they will be willing to lend to other industries with low lending rates, which will actually reduce the financing cost of the whole society.

Therefore, after controlling the shadow banking, China's demand for ineffective financing has fallen sharply, which means that interest rates are bound to fall sharply, and China is expected to formally enter the era of low interest rates in the future.

Fifth, a lot of money is good for the housing market, and low-interest-rate stocks and debt are both bulls!

Therefore, monetary easing actually has two levels of meaning, one is a large number of money, and the other is low monetary interest rates, and the two are not the same thing, but may be opposing states. China's past monetary easing was the first level of quantitative easing, while this round of monetary easing is actually the second level of lower interest rates.

In fact, different conditions of monetary easing will have a completely different impact on asset prices.

A large number of money is conducive to the rise of house prices!

In the past, China was in a state of quantitative monetary easing, with M2 growing at an average annual rate of 15.4%. The total amount of M2 has tripled in 10 years. Over the same period, house prices in China's first-tier cities also increased by an average of about three times, which means that the overissue of money is the most important reason for the rise in house prices.

Not just in China, we have found that the rise in house prices in many countries is accompanied by a surge in currencies. In the United States, for example, the broad money M2 grew by about 2.5 times from 1964 to 1979, while house prices rose by 2.5 times over the same period. Japan's currency increased by 1.5 times in the 1980s, while national land prices rose by 90% over the same period. 6 metropolitan land prices tripled.

On the other hand, if the growth rate of money slows, then house prices will not rise.

For example, the M2 growth rate of broad money in the United States fell from 10% in the 1970s to 6% after the 1980s, while the average annual increase in house prices in the United States fell from 10% to 4%.

Japan's broad money growth rate was as high as 10% in 1980-90, but fell to 2.5% after 1991, and the corresponding increase in Japanese land prices fell from 7% to-4%.

Currency interest rate is low, beneficial to financial assets!

The level of interest rate has an important impact on financial assets.

First of all, the level of interest rates has a direct impact on the bull market of the bond market. when interest rates rise, the bond market goes bad, while when interest rates fall, interest rates in China have fallen sharply over the past 18 years, thus giving rise to a big bull market in bonds.

Secondly, the level of interest rates also has an important impact on the valuation of the stock market.

According to the stock pricing model, there are three main factors that affect the stock valuation, one is the profit growth, the second is the interest rate, and the third is the risk preference, in which the interest rate level has an important impact on the stock market valuation.

Judging from the historical data of the United States over the past 100 years, there is a clear inverse relationship between stock market valuation and interest rates. For example, in the 1970s, when the United States was in an era of high interest rates, the interest rate on government bonds was as high as 10%, while the price-to-earnings ratio of the stock market fell to about 8 times, while interest rates in the United States have continued to fall since 1980, and the current 10-year bond interest rate is less than 3%. The stock market trades at a price-to-earnings ratio of 20 times.

Some people will say, is it because the profits of American companies have improved, so the valuations of US stocks have risen? But in fact, corporate profits in the United States grew at an average annual rate of 10% in the 1970s, compared with 6% after 1980. The only explanation for the sharp decline in profit growth and the sharp rise in stock market valuations is that interest rates have become lower.

In the 1970s, the interest rate on u.s. treasury bonds was as high as 10%, and it took 10 years to buy treasury bonds, so everyone had the same requirement for the stock market, so the price-to-earnings ratio of the stock market was less than 10 times earnings. At present, the interest rate of US treasury bonds is less than 3%, and it takes more than 30 years to pay back the interest to buy treasury bonds, so the stock market valuation of 20 times is not expensive.

In China, the stock market fell by half from 2007 to 18, but the main reason was a sharp fall in valuations, with the price-to-earnings ratio of the Shanghai index falling from a peak of 55 times in 2007 to about 10 times at the end of 18 years.

But in fact, the decline in the price-to-earnings ratio is not due to the decline in profits of listed companies. We estimate that the profits of listed companies have increased by 1.8 times over the same period, with an annual profit growth rate of 11%. In fact, the profit growth rate is much higher than that of the US stock market. but the price-to-earnings ratio of A-shares has fallen from much higher than US stocks to much lower than US stocks.

We think the key reason is that China has overissued its currency in the past decade and is in an era of high interest rates, which have suppressed stock market valuations. With the great development of shadow banking after 2012, the capital of the whole society has been concentrated to shadow banks with high interest rates, so the market also uses the same high interest rate standard to demand the stock market, which makes the stock market valuation drop sharply.

But after controlling shadow banking, interest rates in China have fallen sharply, which means that stock market valuations are also expected to be repaired. The stock market rally over the past 19 years has been accompanied by the repair of valuations, against the backdrop of a sharp drop in interest rates in China.

Deleveraging plus tax cuts is expected to give birth to stock and debt bulls!

Over the past 40 years, us stocks have returned an average of 10 per cent a year, with about 2 per cent coming from dividends and buybacks, 6 per cent from increased corporate profits and 2 per cent from higher valuations.

China's shanghai index has achieved an average annual return of-4% over the past decade, with a dividend yield of 2%, corporate profits growing at 11%, and valuations falling by 15% a year, mainly due to falling valuations.

But if the valuation of the Chinese stock market does not fall in the future, if the current dividend yield is maintained at 2% and corporate profit growth can be maintained at 7%, of which 4-5% comes from economic growth, and the other 2-3% comes from rising inflation, then it can provide an annual return of about 9%, which is very close to that of US stocks over the past 40 years.

If we agree that after the contraction of the currency, China has officially entered an era of low interest rates, the valuation of the stock market has bottomed out, and heavy tax cuts and fee cuts are expected to unleash the potential of household consumption and corporate innovation, so that China's economy and corporate profits will maintain moderate growth, which means that China's stock market is expected to enter a long-term slow bull.

To sum up, the quantitative easing of money over the past decade has given rise to a big bull market in real estate, and if we enter an era of low interest rates, coupled with tax cuts and fee cuts, it is expected to support both stock and debt bulls!

I. economy: improvement of industrial production

1) Industrial production has improved.In the first 22 days of March, the growth rate of coal consumption for power generation in the six major groups increased by 4.7% compared with the same period last year, which is significantly better than the negative growth in the previous two months, which means that industrial production may improve in March.

2) demand is still weak.In the first 22 days of March, real estate production and sales in four major first-tier cities increased 38% year-on-year, while real estate sales in 12 second-tier cities increased by 14% year-on-year, while real estate sales in 18 third-and fourth-tier cities fell 13% year-on-year. Real estate sales in third-and fourth-tier cities are still weak. In the first two weeks of March, the retail and wholesale growth rates of passenger cars in the first two weeks of March were-21% and-25% respectively, narrowing down from the first week, but still by more than 20%.

3) inventories are high and falling.Last week, steel stocks in major cities across the country fell to 16.81 million tons, and rebar stocks fell to 9.17 million tons, a sharp decline for three consecutive weeks. The coal stocks of the six major groups also fell to about 15.6 million tons from the previous high of 17 million tons, while Qinhuangdao coal stocks rose to 6.3 million tons from a low of 5.1 million tons during the Spring Festival.

Second, prices: focus on the rebound in inflation

1(food prices rebounded.Last week, pork prices rose sharply, vegetable prices rose slightly, aquatic products and food prices fell, and food prices rose 1.6% month-on-month.

2) forecasting3月CPIBig liter.Vegetable prices have fallen slightly since March, while pig prices have risen sharply, and given the sharp month-on-month decline in CPI in the same period last year, we expect CPI to rise sharply to 2.4 per cent in March.

3) forecasting3月PPIPick up.Since March, domestic oil prices have risen, steel prices have rebounded slightly, coal prices have risen first and then declined, and the prices of means of production have risen as a whole. Port futures raw capital prices have risen 0.7% month-on-month so far. PPI is expected to rise 0.4% month-on-month in March, and PPI has rebounded to 0.7% in March.

4Pay attention to the rebound in inflation.Although prices were depressed in the first two months of this year, CPI fell to 1.5 per cent in February and PPI remained low at 0.1 per cent. However, with the sharp rise in pig prices since March, coupled with significant increases in oil and steel prices, we expect a significant rebound in both CPI and PPI in March, while CPI may rise to around 3 per cent in April. The short-term rapid rise in inflation is of concern.

Third, liquidity: it is difficult to relax in the short term.

1) currency interest rates continue to rise.Monetary interest rates rebounded sharply last week, with the R007 average rising 31bp to 2.89% Magi R001 average rising 39bp to 2.75%. DR007 uplink 17bp to 2.71% dr 001 uplink 39bp to 2.69%.

2) the central bank has come back again.Last week, the central bank issued 110 billion of reverse repurchase, the reverse repurchase expired at 20 billion, the net reverse repurchase reached 90 billion, the MLF expired at 327 billion, and the open market withdrew 237 billion.

3) the exchange rate remains stable.Last week, the dollar index fluctuated and the RMB remained stable against the dollar, with the onshore and offshore renminbi stable at 6.71 and 6.72 respectively.

4) it is difficult to be more relaxed in the short term.A questionnaire survey released by the central bank last week showed that the macroeconomic heat index and order index at the entrepreneur level in the first quarter were lower than those in the fourth quarter of last year; residents' income perception and employment perception index rebounded, but price expectations fell; and bankers' macroeconomic confidence index and loan demand index rebounded. Although the current economy and prices are still weak, the sharp rise in pig prices will push up short-term inflation, and liquidity will be more relaxed in the short term.

Policy: to ensure that the tax burden is reduced but not increased.

1) to ensure the achievement of the annual development goals.The Premier of the State Council presided over an executive meeting of the State Council on March 20, which determined the division of responsibilities in the Government work report, emphasized the implementation of the task of ensuring the completion of the development goals for the whole year, and clearly defined the supporting measures for value-added tax reduction. It was decided to extend some expired tax preferential policies and give tax concessions to third-party enterprises for poverty alleviation donations and pollution prevention and control.

2The value-added tax reduction has been formally implemented.The Ministry of Finance, the State Administration of Taxation and the General Administration of Customs jointly issued the notice on deepening the Reform of value-added Taxation. Starting from April 1, the tax rate of 16% is originally applicable to the taxable sales of VAT or imported goods by the general taxpayers of VAT. If the tax rate is 13%, if the tax rate is 10%, the tax rate will be adjusted to 9%.

3Make sure that the tax burden is reduced but not increased.The Premier of the State Council visited the Ministry of Finance and the State Administration of Taxation to conduct an in-depth study on the latest progress of tax reduction on a larger scale. During the inspection of the Ministry of Finance, it is pointed out that finance is the mother of the general government, and the enterprise is the foundation of finance. We should be good at using tax leverage to pry economic transformation, improve people's livelihood, and increase consumption. In the process of deepening the VAT reform, it is necessary to ensure that the tax burden of major industries is significantly reduced, that the tax burden of some industries is reduced, and that the tax burden of all industries is reduced but not increased. Let the real money and money of tax cuts fall into the pockets of enterprises.

V. overseas: the Fed's interest rate meeting is loud, euro zone3月PMISet a new low

1) Federal Reserve3There was a loud sound of doves at the monthly meeting.Last Wednesday, the Fed decided to keep the target rate for federal funds unchanged at its March meeting. The bitmap shows that most members believe that interest rates will not be raised in 2019, or once in 2020, and that the Fed announced a shrinking plan to reduce the maximum amount of monthly Treasury holdings from $30 billion to $15 billion starting in May, and to end the contraction by the end of September this year. Powell still expects a positive outlook for the US economy this year, but acknowledges that some data have slowed and has been patient with interest rate hikes. On Friday, yields on three-month and 10-year Treasuries were inverted for the first time since 2007, with all three major indexes falling more than 1.5 per cent and international oil prices down more than 1 per cent, amid fears of an economic slowdown.

2) Euro area3Monthly manufacturing industryPMIHit a new low.The euro zone's manufacturing PMI fell further in March, with an initial reading of 47.6, a 69-month low, announced on Friday. On the same day, Germany's manufacturing PMI in March reached a 79-month low of 44.7, the third month in a row below the rise and fall line, while the French manufacturing PMI in March was also lower than expected. German 10-year bond yields fell below zero on Friday for the first time in 16 years in October, driven by weak economic data and expectations of global monetary easing.

3The European Union has agreed to postpone the Brexit deadline.On Thursday, the EU agreed to postpone the deadline for Brexit to April 12. According to the preliminary draft of the EU, if the British Parliament approves the government's Brexit agreement next week, the EU will agree to postpone Brexit Day, which was originally scheduled for March 29, to May 22. Otherwise, Britain will have to decide by April 12 whether to leave the EU without an agreement or to request a further extension.

4South Korea's foreign trade remains in the doldrums.On Thursday, South Korea reported that exports fell 4.9% from March 1 to 20 from a year earlier, the fourth consecutive month of recession, but the decline was narrower than the previous month, while imports fell 3.4% from a year earlier. In the year to March 20, South Korean imports and exports fell 6.0% and 7.8% year-on-year, compared with 15.2% and 11.5% respectively in the same period last year. South Korea's export contraction in March was mainly dragged down by exports to the Middle East, Japan and China, with chip exports down 25% year-on-year and petroleum products exports down 11.8%.