The main point of this paper comes from China Merchants's Investment Prospect of Ten Industrial Trends in 2023, by Zhang Xia and Chen Gang

Power battery, energy storage, photovoltaic, wind power, high-end manufacturing and other future prospects.

Under the disturbance of the Fed's interest rate hike, geopolitical crisis, epidemic and other factors, A shares have experienced ups and downs in a year, but the coal sector has stepped out of the super market against the trend. In 2023, under the prospect of a slowing global economy and weaker demand, A shares may face a more complex situation. Which assets are expected to stand out then?

China Merchants and Zhang Xia's analyst team released a report on the Investment Outlook of the Top Ten Industrial Trends in 2023 last week, which summarized the two major logic of industrial trend investment next year: looking for low-permeability industries from popular tracks, looking for industrial investment opportunities from the top 20 reports, and predicting ten major industrial trends with the themes of green low-carbon, domestic substitution and digital economy.

Green and low carbon

It has become a global consensus to deal with climate change and low-carbon transformation of energy, and countries around the world have introduced carbon neutralization roads. Among them, China's 14th five-year Plan clearly puts forward "promoting the energy revolution and building a clean, low-carbon, safe and efficient energy system", and emphasizes that "non-fossil energy accounts for about 20% of the total energy consumption." promote the development direction of replacing coal with electricity.

This means that new energy is still the future of the transformation of global energy structure. China Merchants pointed out that in 2023, more attention needs to be paid to low-permeability industries in new energy, especially technological advances, such as composite current collectors in power cells, large and similar storage in energy storage, perovskite cells in photovoltaic cells, and sodium ion batteries.

Trend 1: the upgrading trend of power battery material technology continues.

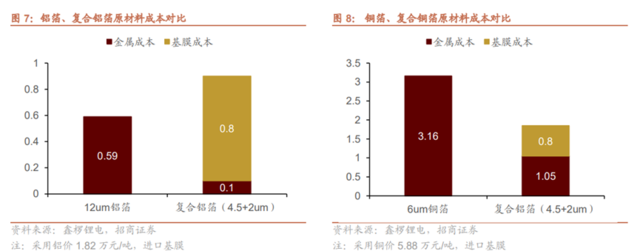

China Merchants believes that the composite collector is greatly optimized in safety, performance and cost, which is expected to partially replace the traditional collector.

At present, due to the more complex preparation process of composite current collector and the lack of equipment maturity, the production yield is low, and its comprehensive cost is higher than that of traditional current collector. However, if we consider the process progress, large-scale mass production, and the localization of the equipment, the yield and efficiency will be greatly improved. Ideally, the cost of composite copper foil is expected to be 20-30% lower than that of traditional copper foil, and the cost of composite aluminum foil may be slightly higher, but the advantage of safety performance may be obvious.

China Merchants said that at present, the composite collector has initial mass production capacity, and with the increase of downstream battery and terminal investment, mass production application may begin in 2023.

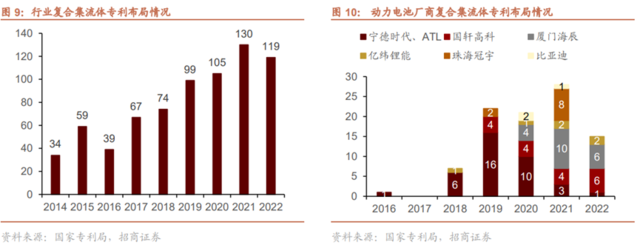

In the battery enterprises represented by Ningde era, the number of patents related to composite current collector has increased rapidly after 2018-2019. According to industry feedback, leading battery companies may already have mass production capacity, while most of the other major battery companies hope to solve key equipment issues such as preparation process and roll welding in the coming year. According to public information, some European car companies may start loading applications next year. Due to the advantages of safety, energy density and low cost (post-production) of composite current collector, it has also attracted a number of consumer digital battery and energy storage battery enterprises to actively try, and it is possible to start preliminary mass production application next year.

Trend 2: large-scale energy storage and similar energy storage will usher in the first year of the outbreak.

China Merchants concluded in the report that large-scale energy storage is currently the main force of domestic energy storage, independent energy storage to participate in the power spot market to further improve the business model of large energy storage, the upstream price correction will also promote a significant reduction in energy storage costs.

Independent energy storage breaks the classification criteria and income boundaries of the original power supply, power grid, user side, etc. it is a business model in line with the operation characteristics and actual needs of the power grid, and it is also the direction encouraged by the government, and the growth may be faster. At the same time, it may lead the energy storage investors to pay more attention to the quality of the energy storage system from giving priority to cost.

For every 10,000 per ton price of silicon material, the corresponding terminal price can be reduced by about 2.5-3 cents / W, and part of the income space formed may be used for the configuration of energy storage. The tight supply and demand of lithium carbonate, silicon and chips in 2023 is expected to ease this year, and the cost of energy storage system is expected to decline.

In addition, energy storage is an efficient and economic way to solve the problem of new energy consumption, which has more cost advantages than energy storage. Flexible transformation, gas power generation and other energy storage business is expected to develop rapidly.

In terms of cost, the additional cost of flexible transformation based on the investment of a single thermal power plant is mostly about tens of millions, and the flexible scheduling space is increased by 10-30%, with an investment of 50-1000 yuan per kilowatt and a gas investment intensity of 2000-3000 yuan per kilowatt. And from the energy point of view, the marginal cost is only the cost of coal and gas storage, which is far lower than other energy storage schemes, and the economy has more advantages.

In November 2021, the National Development and Reform Commission and the Energy Bureau issued the notice on carrying out the transformation and upgrading of national coal-fired power units. During the 14th five-year Plan period, all new units are planned to achieve flexible manufacturing, and the existing units in service should be changed to complete 200 million kW retrofit, increasing the system regulation capacity by 3000-40 million kW, realizing the flexible scale of 150 million kW, and requiring all newly-built units to achieve flexible retrofit. According to the new team of China Merchants, the market space for flexibility transformation of thermal power is 500-80 billion.

Trend 3: the photovoltaic efficient route has a stronger beta.

China Merchants pointed out that the theoretical limit of conversion efficiency and laboratory data of perovskite battery are higher than that of crystalline silicon battery, which is more economical and cost-effective than silicon battery production process.

At this stage, with the support of a number of top-level policies, the construction and planned number of 100 megawatt production lines of perovskite single junction batteries have increased significantly, and perovskite laminated batteries are mostly in the stage of research and development.

Trend 4: the industrialization of sodium ion battery is accelerated in an all-round way.

China Merchants pointed out that at present, the price of lithium carbonate remains high, the cost of lithium electricity has risen sharply, and the advantages of raw materials for sodium ion batteries are prominent. compared with lithium resources, sodium resources are abundant, cheap and easy to extract. At present, domestic start-up sodium electricity enterprises and lithium power enterprises are actively laying out the sodium battery industry chain, including cathode materials, negative electrode materials, electrolytes, sodium batteries and so on, and the industrialization is accelerated in an all-round way.

Domestic substitution

The 20th CPC National Congress stressed that it is necessary to strengthen the resilience and safety level of the industrial chain supply chain, strengthen the ability of scientific and technological self-reliance, speed up to make up for shortcomings in areas related to security development, and establish a new national system to strengthen the national strategic scientific and technological strength.

In China Merchants's view, this marks a period of time in the future, industrial chain supply chain security thinking will be in all aspects of macro industrial policy, from the policy, macro level to consider the direction of investment in the next five years, industrial chain supply chain security will be one of the important clues.

Trend 5: under the trend of large-scale wind power, the field of short board components will usher in an outbreak.

China Merchants believes that the trend of large-scale wind turbines in China is obvious in recent years, and the large-scale wind turbines put forward higher technical requirements for wind power main bearings, and wind power bearings are the last link of complete localization of wind turbines.

At present, the global wind power bearing market has long been monopolized by overseas bearing manufacturers. Due to the technological gap between the domestic bearing industry and international enterprises, China needs to import a large number of high-end bearings. However, as the domestic bearing industry speeds up independent research and development, China Merchants believes that Luo shaft and other domestic bearing manufacturers are gradually filling the gap of domestic large megawatt spindle bearings.

Trend 6: the replacement of high-end manufacturing key components such as CNC machine tools and industrial robots has entered a critical stage.

At present, the upstream functional components of China's high-end CNC machine tools have not yet formed a good industrial matching, and most of the functional components are monopolized by companies in Japan, Germany and the United States. The localization rate of China's high-end CNC machine tools is only 6% as of 2018, and domestic supply mainly depends on outsourcing.

While Germany and Japan firmly occupy the dominant position in the industrial robot market, domestic robot companies are frantically catching up.

In 2021, domestic industrial robot brands accounted for 32.8% of the domestic market, an increase of 4.2% over the same period last year. The main reasons include, on the one hand, foreign-funded enterprises are affected by the epidemic in many aspects, such as production, delivery and after-sales service, and their comprehensive competitiveness is reduced. In the face of the opportunities brought by the epidemic, domestic robot manufacturers rely on their strong technology and service capabilities. Rapidly seize the original foreign market, the process of localization has been further accelerated, and the share of core industrial control products is expected to continue to accelerate. On the other hand, domestic head robot manufacturers have a good momentum of development.

In terms of spare parts, 85% of China's reducer market, 90% of the servo motor market and more than 80% of the control system market are occupied by overseas brands.

Trend 7: the development of domestic neck software has entered an acceleration period.

In a dominant field of basic software in the United States, domestic basic software, especially the weakest operating system, has made some breakthroughs in China, such as Kirin Software, Uni-Credit Software, and Euler and Hongmeng launched by Huawei.

In the field of industrial software, Europe and the United States occupy most of the country, domestic industrial software is gradually rising, but the comprehensive strength is still weak.

However, the huge market is expected to spur domestic software to speed up the pace of catch-up. In 2020, the size of China's industrial software market is 197.4 billion yuan. From 2012 to 2020, the growth rate of China's industrial software market is basically more than 10%, and 14.8% in 2020, much higher than the global growth rate (6.1%), with great potential for development.

Digital economy

According to the Digital economy Development Plan of the 14th five-year Plan, by 2025, the digital economy will enter a period of comprehensive expansion, the added value of the core industries of the digital economy will account for 10% of GDP from 7.8% in 2020, the ability of digital innovation to lead development has been greatly enhanced, the level of intelligence has been significantly enhanced, the integration of digital technology and real economy has achieved remarkable results, and the governance system of digital economy has become more perfect. The competitiveness and influence of China's digital economy have improved steadily.

In this regard, China Merchants pointed out that the direction of the digital economy needs to focus on the current policy support of the car-road coordination and meta-universe of the two major industrial trends.

Trend 8: car-road coordination will usher in the first year of the outbreak.

China Merchants said that vehicle-road coordination is the main development direction of intelligent driving in the future, and vehicle-road coordination has both cost and practical advantages compared with bicycle intelligence.

From the cost point of view, bicycle intelligence needs powerful on-board chips and software, and the perception and computing power of vehicle-road coordination is mainly at the road end, and the same set of roadside equipment can be used continuously by multiple vehicles, which can greatly reduce the cost. From a practical point of view, bicycle intelligence is easily affected by environmental conditions and difficult to deal with emergencies. In contrast, the accuracy of vehicle-road collaborative information exchange and judging the key target state is higher. With the further expansion of the scale of the self-driving market, vehicle-road coordination is expected to replace bicycle intelligence as the main development direction of self-driving.

The high penetration of 5G and intelligent network connected vehicles is the basis of vehicle-road collaborative development. At present, China has a complete vehicle-road collaborative industry chain. Under the promotion of policy, China's vehicle-road coordination is expected to enter a period of rapid development.

According to the forecast of Yiou think tank, the scale of China's car-road coordination market is expected to reach 496 billion yuan in 2030, and CAGR is expected to reach 27% in 2021-2030.

Trend 9: meta-cosmic applications will be densely landed.

Domestic policies help to promote the orderly development of metacosmos industry, the overall policy takes into account supervision and development, and local policies focus on technological R & D breakthroughs and industrial integration applications to build an omni-directional meta-universe ecological development system.

As the infrastructure of meta-universe hardware equipment, VR equipment is the key entrance of meta-universe from concept to commercialization. With the release of a number of new VR products, hardware technology continues to upgrade, which accelerates the development of meta-universe.

The rise of traditional Chinese medicine

Trend 10: traditional Chinese medicine formula granule plate will usher in Davis double-click.

As a derivative and innovation of traditional Chinese medicine, traditional Chinese medicine formula granules have the advantages of high degree of standardization, convenient hygiene, clear quantity, easy preservation, not easy to deteriorate and so on.

China Merchants said that although the price of traditional Chinese medicine formula granules is generally higher than 30% Mel 40% of traditional Chinese medicine slices, its portability makes consumers willing to pay a premium for it. In addition, the introduction of the national standard for traditional Chinese medicine formula granules has broadened the sales scope, and the expansion of the number of traditional Chinese medicine medical institutions has enhanced the demand for traditional Chinese medicine formula granules. The price of traditional Chinese medicine formula granules is open and transparent. With the inclusion of traditional Chinese medicine formula granules into health insurance, the reimbursement ratio is expected to increase, and the market size of traditional Chinese medicine formula granules is expected to double.

According to the report, the market size is expected to reach 53.218 billion yuan in 2025, and CAGR is expected to reach 20.5% in 2021-2025.

Multi-channel funds to join the sing long Hong Kong stocks camp, the agency said the investment window has been opened. Tuyere now, I do not know how to choose individual stocks? Give it to professional fund managers > >Click to learn more about Greater China-themed funds