Enviro-Hub Holdings Ltd. (SGX:L23) shareholders have had their patience rewarded with a 29% share price jump in the last month. But not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 21% in the last twelve months.

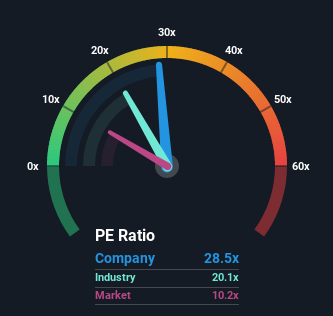

Since its price has surged higher, given close to half the companies in Singapore have price-to-earnings ratios (or "P/E's") below 10x, you may consider Enviro-Hub Holdings as a stock to avoid entirely with its 28.5x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings growth that's exceedingly strong of late, Enviro-Hub Holdings has been doing very well. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Enviro-Hub Holdings

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Enviro-Hub Holdings would need to produce outstanding growth well in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 106% last year. EPS has also lifted 28% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to decline by 1.1% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

With this information, we can see why Enviro-Hub Holdings is trading at a high P/E compared to the market. Investors are willing to pay more for a stock they hope will buck the trend of the broader market going backwards. Nonetheless, with most other businesses facing an uphill battle, staying on its current earnings path is no certainty.

The Key Takeaway

The strong share price surge has got Enviro-Hub Holdings' P/E rushing to great heights as well. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Enviro-Hub Holdings maintains its high P/E on the strength of its recentthree-year growth beating forecasts for a struggling market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. We still remain cautious about the company's ability to stay its recent course and swim against the current of the broader market turmoil. Although, if the company's relative performance doesn't change it will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Enviro-Hub Holdings (of which 1 is significant!) you should know about.

If P/E ratios interest you, you may wish to see this free collection of other companies that have grown earnings strongly and trade on P/E's below 20x.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.