Source: Wall Street

Author: Zhao Ying

The use of "final loans" has surged to its highest level since June 2020, suggesting that some banks are already facing greater liquidity pressures.

The liquidity shock triggered by the Fed's tightening policy has forced banks to seek "last resort" instruments.

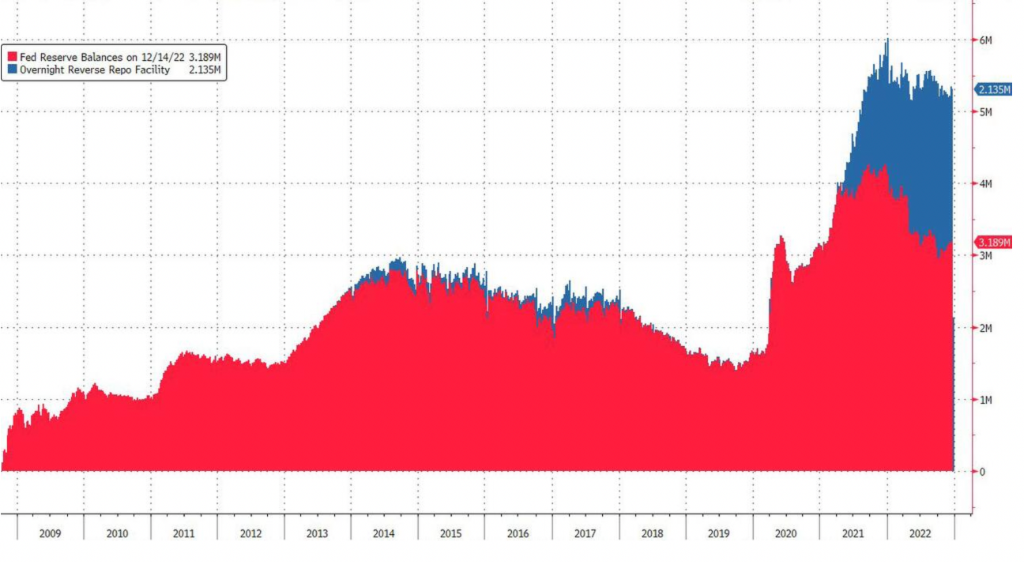

On Tuesday, market participants observed that the Fed's balance sheet shrank by more than $400 billion six months after it began shrinking. Judging from the Fed's debt structure, the Fed's reserves are currently about $3.1 trillion, while reverse repos are $2.13 trillion.

In the past year, Fed reserves have decreased by $1 trillion, while reverse repurchase has increased by about $500 billion.。

Further, the Fed's discount window borrowing (the last loan) surged to just over $6.2 billion last week, peaking at $9.1 billion two weeks ago, the highest level since June 2020.

This is a wake-up call to the market, indicating that some banks have begun to face greater liquidity pressure. JPMorgan Chase & Co analysis pointed out that with the gradual rise of financing pressure, there are as many as 30 small banks "insolvent".

"Last loan"

The Fed discount window is a tool for the Fed to provide loans to banks.When banks are short of funds, they turn to the Fed for help, which is used to provide them with short-term financing.

It is worth mentioning that when a bank needs to obtain a loan from the discount window of the central bank, it shows that there are some problems with the market credit of the commercial bank, so the discount rate is often higher than the current market interest rate, with a certain punitive nature.

On the other hand, during the crisis, the discount window was a key tool for the Fed to ensure that banks had access to capital. During the 2008 financial crisis, the Fed extended the maturity of discount window loans to ensure that banks had access to credit and injected more liquidity into the financial system.

As a result, the discount window is also known as the "loan of last resort", through which the Fed acts as the "lender of last resort".

But other types of financial institutions, such as securities brokers, may also face serious problems, including Bear Stearns, Lehman Brothers, Merrill Lynch, Goldman Sachs Group, Morgan Stanley and so on. The Fed provides cash or short-term liquidity support to these companies through mortgages.

What is behind the surge in borrowing in the discount window?

What are the reasons behind the surge in the use of discount windows in the US, which still has a lot of liquidity in the financial system?

According to JPMorgan Chase & Co's analysis, there are three possibilities. The first is reduced liquidity in small banks:

Against the backdrop of continued Fed tightening, funding pressure on small banks has increased. To boost liquidity, some small banks may find discount window rates economically more attractive than entering the federal funds market or borrowing from the Federal Home loan Bank (FHLB).

In fact, the primary credit rate (primary credit rate) was set at 4.0% (before the December FOMC meeting), 17 basis points higher than the effective federal funds rate (effective federal funds rate,EFFR), but 30-70 basis points lower than the $1 million-$3 million FHLB advance. In addition, the increased use of the discount window seems to be related to the cryptocurrency market, especially after the news of the collapse of the cryptocurrency exchange FTX in November.

Second, the second plausible theory is that small banks lose more money:

The Fed's aggressive tightening has led to big losses on banks' securities portfolios this year, with Bank of America Corporation losing about $770 billion, as reflected by AOCI, the change in the market value of bonds in AFS's portfolio, which has greatly reduced banks' equity. In some cases, even tangible common equity has fallen to negative value.

Among them, small banks were particularly affected. According to S & P data, JPMorgan Chase & Co found that as of the third quarter,About 30 banks, most of which have total assets of less than $1 billion, reported negative tangible common equity, up from 11 in the second quarter of 22 and 0 in the first quarter of 22. The implication is that about 30 banks are actually unable to repay their debts and survive only with emergency funding from the Federal Reserve.

Finally, it is worth noting that demand for liquidity defenses at big banks is on the rise:

As a result of the Fed's sharp interest rate hike, large losses on banks' securities portfolios have not only led to asset decline, but also caused potential liquidity problems. As the Fed shrinks, liquidity in the financial system is drying up, deposits are falling (now mainly in large banks), funding pressures are rising and borrowing costs are rising.

Observers say that overall, the surge in the use of the discount window sends an ominous signal, with the weakest link being the "insolvency" of as many as 30 small banks, reminding the market that the implosion of Terra/Luna led to the collapse of FTX and the massive deleveraging of the entire encryption ecosystem, causing pain to the entire US financial system.

Edit / somer