The core concerns of investors over the past six months:

1.iPhoneX repeatedly sends out the information of hacking orders.

2. The price of DRAM rises and the US dollar strengthens, which leads to the decline of gross profit.

Q2 Financial report Information:

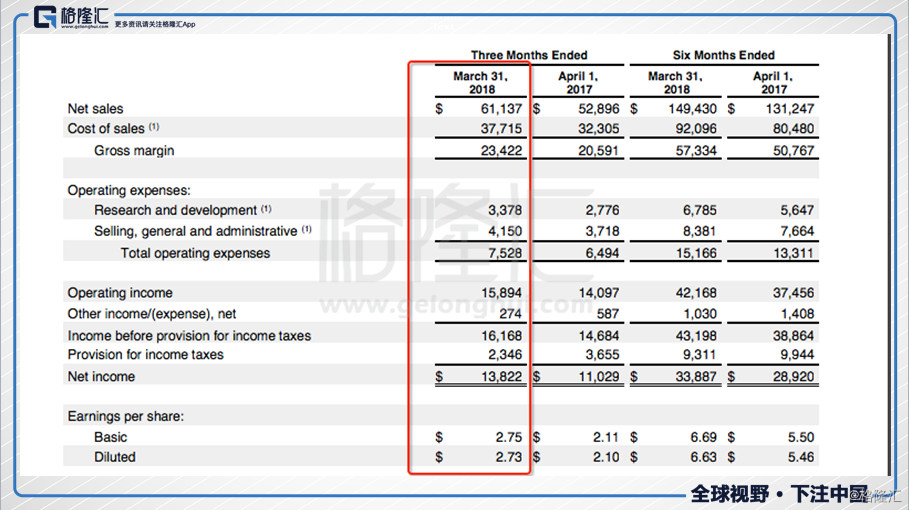

Apple Inc's fiscal year begins in September, so the first quarter of the fiscal year is from September to December and the second quarter is from January to March.

As of March, Apple Inc's Q2 sales were $61.14 billion, up 15.6% from a year earlier. Net profit was $13.82 billion, an increase of 25.3% over the same period last year.

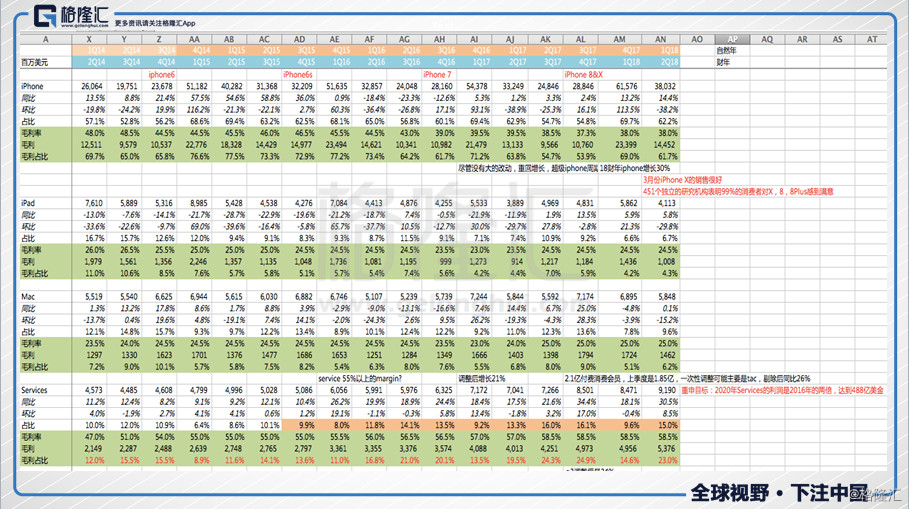

If you break down the sales, you can see the following data (there are these data in the figure above, and some of the gross margin figures here are forecasts, so there will be some deviations):

IPhone's sales were 38.03 billion US dollars, up 14.4% from the same period last year.

IPad's sales were 4.11 billion US dollars, up 5.8% from the same period last year.

Mac's sales were 5.85 billion US dollars, up 0.1% from the same period last year.

Services sales of 9.19 billion US dollars, up 30.5% from the same period last year.

Other business sales were 3.954 billion US dollars, an increase of 37.6% over the same period last year.

IPhone accounts for 61.7% of Apple Inc's total revenue, while other businesses together account for 15.3%.

According to the number of products sold, iPhone Q2 sold 52.217 million units, up 3% on the same period last year and 4.078 million units on the same period last year, up 6% on the previous year, down 3% on the same period last year.

Financial report highlight 1: huge buyback plan

Apple Inc announced a 16% increase in the dividend payout rate and set aside $100 billion to buy back shares.As of May 2, Apple Inc's total market capitalization was 858 billion US dollars. In other words, at the current price, Apple Inc wants to buy back 11.6% of the shares.

Personal point of view: Apple Inc may have gone through the growth stage, so it is very difficult to earn growth money from Apple Inc. For a mature enterprise, one of the ways to maximize the interests of shareholders is to buy back shares and increase dividends. Tim Cook is not Jobs, but it is definitely a CEO that focuses on the interests of shareholders.

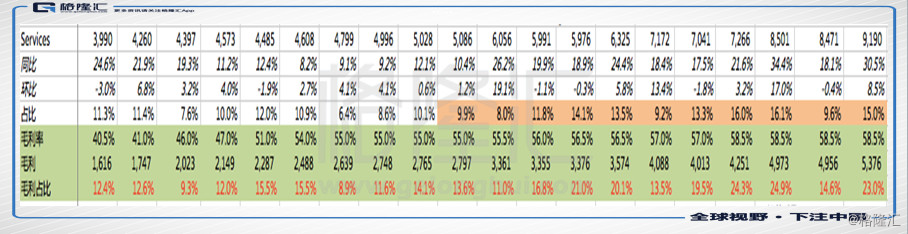

The highlight of the financial report, the growth rate of 2:Services performance is faster than expected.

Sales of Q2Cinema services reached $9.19 billion, up 31% from a year earlier, the highest growth rate in the past three years.

Apple Inc's Services mainly includes iTunes, app store, app music, apple pay and iCloud service business.

At present, Services accounts for 15% of Apple Inc's sales and 23% of Apple Inc's gross profit.

This is mainly due to gross margins of around 38 per cent for iPhone and 60 per cent for services (perhaps even higher because of operating leverage).

Services should account for more than 23% of EBIT (operating profit). My own guess is that the ratio should be around 30%, 35%.

In other words, iPhone may contribute 50%, 60%, and 30% of Apple Inc's operating profit, and 10%, 20% of other businesses.

In addition, in the Q4 conference call, management said Apple Inc's paid subscribers were 270 million, up 100m from last year and 30 million in the past three months. At the same time, the number of Apple Pay active users increased by 100%, and the transaction volume tripled.

Personally, I think this data can reflect that Apple Inc's entire mobile phone ecosystem is still very healthy.

Apple Inc stressed again in the conference call that the goal of the Services business is to generate $48 billion in revenue in 2020 (double that of 2016).

Apple Inc's current main investment logic may have two (personal point of view)The buyback 2.Services of US $100 billion continues to grow at a high rate, and its share of EBIT continues to rise, resulting in an increase in valuation multiples.

Services is a typical highly sticky, non-cyclical business, which is completely normal at a growth rate of 20 times or even 25 times at a growth rate of 15%.

Financial report highlight 3: wearable products grow by 50%

The sales of other products of Q2 and Apple Inc were US $3.954 billion, an increase of 37.6% over the same period last year. During the conference call, management said wearable devices (watches, Beats, and Airpods) were growing at 50 per cent. Among them, Airpods is extremely popular and the demand is very strong.

It is worth emphasizing that iWatch has grown by 50 per cent year-on-year for four consecutive quarters.

Financial reporting question 1:

IPhone gross margin continued to decline slightly.

So far, according to the pre-market increase, the market should reflect the benefits of buybacks and Services, while overall the gross margin of Apple Inc's Q is 38.3%, which is fully in line with the 38% Guidance given earlier.

Careful analysis, in fact, the gross margin of iPhone is still declining, because the proportion of Services is increasing, and Services is a high gross margin business, according to reason, the overall gross margin is to rise. But the figures we have seen so far are slightly lower than expected, indicating that iPhone's gross margin must have fallen a little.

One of the main reasons for the decline is the rise in DRAM prices.Some views on DRAM were given in the management conference call: Cook believes that the price of DRAM will peak by the end of the year, and then iPhone's gross margin will begin to stabilize (Meguiar's share price decline may have something to do with this sentence, this is no longer a Micron share price reflects Apple Inc's conference call).

Financial reporting question 2:

IPhone may be close to saturation.According to the Q2 financial report, Apple Inc's iPhone sales in the past three months were 52.22 million, up 2.8 per cent from a year earlier.

Almost since Q1 in 2016, Apple Inc's overall sales of iPhone has increased by less than 5%. IPhoneX's sales are actually very mediocre, far from reaching the point of popularity.

According to IDG, global mobile phone shipments in 2017 were 1.472 billion, down less than 1 per cent from 2016 (1.474 billion in 2016) and basically the first negative month-on-month growth in mobile phone sales in the past decade.

IPhone2016 shipped 212 million units a year and 216 million in 2017, an increase of 1.9% over the same period last year. In other words, iPhone actually took more market share in the past year.

Cook emphasized one thing on the conference call: iPhone users are much less likely to switch to Android users than Android users to iPhone users.

But in any case, the dividend period of smartphone penetration from 10% to 90% is over.

Personal opinion:

The understanding of industry saturation is all dynamic thinking. The reason why the market is saturated today is directly related to the slower and slower speed of hardware innovation, but thinking about this problem must not be linear thinking.

Take a simple example:

In 2014, the global taxi market in which Uber (UBER TECHNOLOGIES INC) was located was $100 billion, and many people thought that Uber might take 10% of Uber's 20% share, so the possible valuation should be $10 billion to $20 billion, but at the end of 2014, Uber's total market capitalization was $50 billion.

Therefore, many people think that the valuation of Uber is completely unreasonable.

Instead of judging whether it is a bubble or whether it is expensive, I will just mention a question in the above logic: the global size of the taxi industry in 2014 was $100 billion, which is no problem.

But many people ignore a non-linear problem: the emergence of Uber, the emergence of DiDi Global Inc., make the traffic more convenient, so the frequency of taxi hailing is higher, so when this product appears, it will quickly increase the scale of the industry.

I've seen one data before that the size of the entire Los Angeles taxi market has tripled in four years because of Uber, which is a typical example of quality products boosting demand.

So "saturation" is based on this type of "smartphone" at this moment, and if there is a disruptive product, the market space will be opened up quickly.

In my opinion, Apple Inc is already a mature enterprise before the subversive products come out, and the growth rate will continue to slow down. The long-term logic of holding Apple Inc now should be: the repurchase plan of US $100 billion and the increase of Services share lead to higher valuation.