On December 15, US time, the Accounting Supervisory Board of listed companies (PCAOB) released a report on its website saying that it had obtained the audit authority of US-listed companies for the first time. PCAOB said that after nine weeks of on-site review in Hong Kong, ChinaConfirm that it will be able to obtain unfettered examination authority for accountants in mainland China and Hong Kong, China in 2022And then revoke its decision announced at the end of 2021 that it could not review the relevant firms.

The China Securities Regulatory Commission also issued a positive response to the progress on the morning of December 16, Beijing time, saying that since the signing of the audit regulatory cooperation agreement at the end of August, the regulators of both sides have strictly implemented the relevant agreements of their respective laws, regulations and agreements. cooperation has carried out a series of fruitful inspection and investigation activities, and all work is progressing smoothly. We welcome the re-determination made by US regulators based on the professional consideration of supervision. Look forward to continuing to promote annual audit supervision cooperation in the future.

New progress in Sino-US audit regulatory cooperation: substantial breakthroughs, laying the foundation for subsequent continuous cooperation; delisting risk has been reset

On the whole, this progress is a new progress and substantial breakthrough after the signing of an audit supervision cooperation agreement between China and the United States ("tracking of Chinese stocks: the signing of an audit supervision cooperation agreement between China and the United States"). It lays the foundation for the follow-up and continuous annual audit supervision cooperation, and basically eliminates the risk that Chinese stocks will be marked again when they disclose their annual reports early next year (they will face the risk of delisting for three consecutive years. The countdown to potential delisting of companies that have been on the list since early 2022 will also be reset.

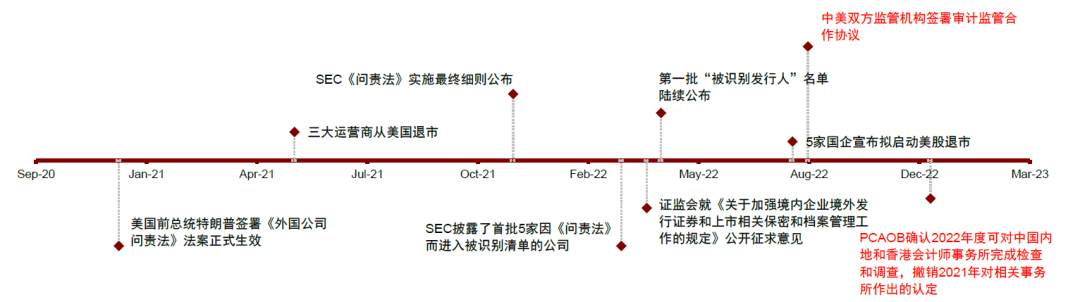

The audit problem of US-listed stocks has existed for a long time, and it is also one of the main factors to suppress the risk preference of US-listed stocks in recent years. The issue was heightened by the signing of the Foreign Company Accountability Act by then-President Donald Trump at the end of 2020. A core element of the bill is to require accounting firms of foreign companies to submit audit papers, which may be delisted if they fail to do so for three consecutive years.

At the end of 2021, the US Securities Regulatory Commission (SEC) issued further detailed rules for the implementation of the Act, and formally implemented it in March this year. Companies that do not meet the requirements have been marked and included in the so-called "identification list". At present, there are more than 170 companies on the list.

China has continuously provided conditions for regulatory cooperation to facilitate substantial progress this time. In December 2021 and April 2022, the State Council and the Securities Regulatory Commission respectively solicited opinions on the drafting of the regulations of the State Council on the Administration of overseas issuance and listing of domestic Enterprises (draft for soliciting opinions) and the revision of the provisions on strengthening the Security and Archives Management of overseas issuance and listing of domestic Enterprises (draft for soliciting opinions), to increase the coverage of domestic enterprises listed in Hong Kong and the United States. Provide institutional guarantee for cross-border regulatory cooperation, which also leaves some room for cooperation between China and the United States.

On the evening of August 26, 2022, the website of the China Securities Regulatory Commission issued a notice that Chinese and US regulators signed an audit cooperation agreement and made a clear agreement on the cooperation between the two sides in carrying out regulatory inspection and investigation activities on relevant accounting firms. to form a cooperation framework in line with the laws and regulations and regulatory requirements of both sides. PCAOB then arrived in Hong Kong, China, in September for its first inspection and investigation, and released the report.

Review details and follow-up progress: determine access to review authority and prepare a follow-up periodic review plan

PCAOB reported that its staff traveled to Hong Kong, China in September and reviewed two accounting firms, KPMG and PricewaterhouseCoopers, which were set up in mainland China and Hong Kong, China within nine weeks. During this period, the regulators of both sides strictly enforced the relevant agreements of their respective laws, regulations and agreements, and finally decided to revoke the decision announced at the end of 2021 that the relevant firms could not be reviewed. And confirmed that a complete inspection and investigation can be carried out in 2022.

PCAOB said that it can 1) choose and decide the company and audit business it inspects, 2) be able to view the complete audit working paper and retain relevant information to complete the follow-up work, and 3) interview people related to the audit and obtain testimony.

In the course of the review, PCAOB initially found some possible problems in the inspected company, which is basically consistent with its findings in its first inspection in other countries and regions. If necessary, further investigations will be made and possible actions will be taken, such as requests for correction within one year.

In addition, PCAOB said the review was just the beginning and was already preparing plans for further audits of US-listed stocks in early 2023 and beyond.

Potential impact and significance: temporarily eliminate the tail risk of delisting of Chinese stocks; improve risk appetite; return to Hong Kong stocks is still the main trend

It will help to eliminate the tail risk of delisting of most Chinese stocks in the short term. As we mentioned earlier, one of the core contents of the Foreign Company Accountability Law is that if the accounting firms of foreign companies fail to submit audit papers for three consecutive years, these foreign companies may face the risk of delisting.

An important significance of this progress is that US regulators have reversed the decision that relevant firms cannot be reviewed at the end of 2021, so we believe that there is a high probability that Chinese companies will no longer be marked on the list when they disclose their annual reports early next year. This means that the three-year countdown will be reset, temporarily eliminating the tail risk of delisting Chinese stocks.

Looking forward, this round of breakthroughs has also laid a realistic foundation for continued regulatory cooperation, as the China Securities Regulatory Commission responded, we also have reason to believe that in the future, China and the United States can continue to promote future audit regulatory cooperation on the basis of previous cooperation experience. In this way, the tail risk of delisting of US-listed companies and decoupling of Sino-US finance can be basically eliminated.

However, whether it is delisted or not, the choice of listing in Hong Kong will still be a major choice and trend for Chinese stocks to hedge against potential uncertainty, which will help to optimize the market structure of Hong Kong stocks, attract capital precipitation, and strengthen Hong Kong's position as a financial center. At present, 28 companies have returned to Hong Kong stocks through secondary listings or dual major listings (of which 19 are secondary listings, 9 are major listings, and 4 of the 19 companies have changed to dual major listings).

Looking ahead, we expect more eligible US-listed companies to return to Hong Kong stocks. Based on the current conditions, we estimate that 27 companies will still be eligible for regression.

In the way of return, considering that the dual major listing can keep its listing status in Hong Kong unaffected when the external listing status changes, and can be included in the scope of Hong Kong Stock Connect, we believe that the adoption or conversion of major listing will become the mainstream. We estimate that if the above-mentioned companies become major listings and are included in the Shanghai-Hong Kong Stock Connect, they are expected to bring about HK $50 billion in capital inflows.

In the medium and long term, the return of more US-listed companies will help to further optimize the structure of the Hong Kong stock market, attract capital precipitation, and then form positive feedback from high-quality companies and capitals. further consolidate the position of the Hong Kong stock market as a regional financial center and China's "new economic bridgehead".

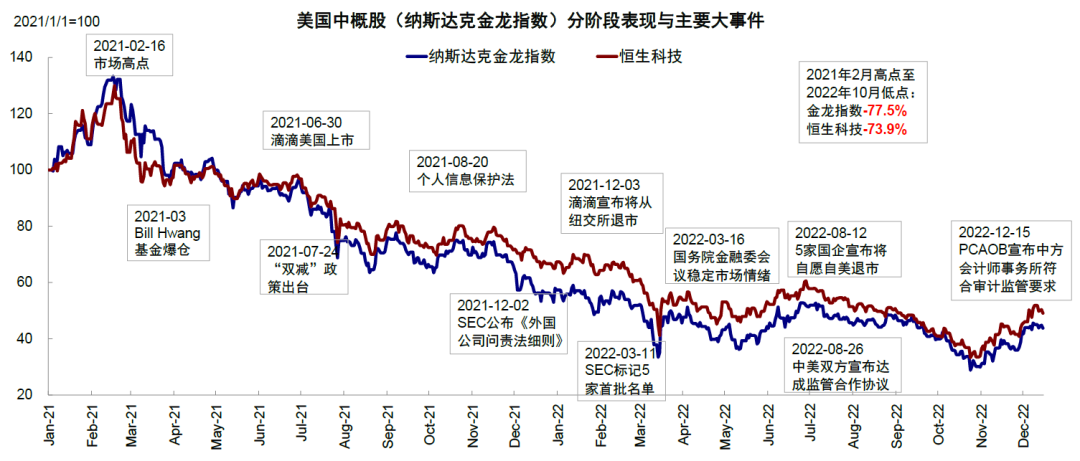

In the short term, current regulatory progress has helped to improve risk appetite and support the current mood and valuation repair for Hong Kong and US-listed stocks. Since the end of October, the Hong Kong stock market has rebounded strongly, the MSCI China Index has rebounded by nearly 40%, and Hang Seng Technology has risen nearly 60%. The main driving force behind this is the "triple pressure" that Hong Kong stocks are facing (Fed policy tightening, China's economic growth and geopolitical tensions) are all expected to improve to varying degrees.

This rebound trend also basically confirms the view we put forward in mid-November that the most difficult time for Hong Kong stocks is gradually passing and turning for the better ("Hong Kong stock market outlook 2023: showers do not last all day"). After the recent rebound, apart from some technical indicators showing short-term overbuying and profit-taking pressure, Hong Kong stocks still outperform the overall global market and their valuations are still low. The positive developments in the regulation of US-listed stocks have provided a "reassurance" to the delisting risk that has lasted for many years, which is expected to continue to promote the repair of investors' risk appetite, thereby supporting valuation repair.

In the current position, we think that it is understandable for the market to have a short break or even consolidation, but it may also be difficult to reverse the repair trend that has been formed, and the market is expected to rise in the twists and turns, but more upside space depends on further profit repair.

Chart 1: the audit problem of Chinese-listed stocks has existed for a long time. After many consultations, China and the United States signed an agreement on cooperation in audit supervision.

Source: China Securities Regulatory Commission, US Securities Regulatory Commission, HKEx, China International Capital Corporation Research Department

Chart 2: overseas Chinese capital stock market performance and major events since 2020

Source: Bloomberg, China Securities Regulatory Commission, US Securities Regulatory Commission, HKEx, China International Capital Corporation Research Department

Chart 3: since the reform of the listing system in 2018, 28 US Chinese stocks have returned to Hong Kong through secondary listings and dual major listings.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Note: data as of December 16, 2022; valuation based on Bloomberg consensus expectations

Figure 4: estimation of potential passive funds if secondary listed companies are included in the eligible target of Hong Kong Stock Exchange.

Source: HKEx, Wind, China International Capital Corporation Research Department

Note: data as of December 16, 2022

Chart 5:27 US Chinese-listed stocks or basically comply with the secondary listing rules of Hong Kong stocks; some high-quality head companies may choose dual major listing

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Note: data as of December 16, 2022; valuation is based on Bloomberg consensus expectations; the blue part is companies that meet the secondary listing criteria based on the average market capitalization at the end of each month in the previous 12 months.

Edit / ping