Source: Caihua Society

Once praised as capable of "subverting all industries"$Amazon (AMZN.US)$The peak occurred in July 2021, when the market capitalization reached $1.9092 trillion, compared with today's $902.4 billion, more than 1 trillion evaporated in a year, equivalent to two$Tesla (TSLA.US)$。

During the same period, large supermarket chains also engaged in retail business$Walmart (WMT.US)$The market capitalization expanded from US $387.8 billion to US $402.1 billion, an increase of US $14.3 billion.

Retail for success and retail for failure

Amazon.Com Inc started selling books, but now it is not just a book retailer, it sells everything from goods to services. Not only sell it for third-party merchants, but also sell it yourself. There are not only online sales, but also offline stores.

Data is the most valuable asset for online retailers.

Amazon.Com Inc became the most influential online retailer with huge transaction data between merchants and users, and improved stickiness by launching his own paid membership service, exempting freight, stimulating user purchase frequency, and optimizing user experience, thus paving the way for the launch of content services such as movies, dramas and so on.

Amazon.Com Inc's membership service certainly provides an opportunity for its massive expansion, but because the membership fee is not too high, the benefits and services available are very considerable. Amazon.Com Inc's retail income continues to slow down with the general environment, while the operating costs of the retail business are rising.

It is worth noting that Amazon.Com Inc's retail business is divided into two categories.$JD.com (JD.US)$Similarly, it provides platform services and proprietary services.

The platform business is to match the transactions between buyers and sellers. Amazon.Com Inc collects transaction commission and can also provide performance and delivery services as needed, and charge corresponding service fees. The income recorded is the service fee income of third-party merchants. Proprietary business refers to Amazon.Com Inc selling his inventory and providing performance, delivery, after-sales services, and the income recorded is the price of goods and services sold.

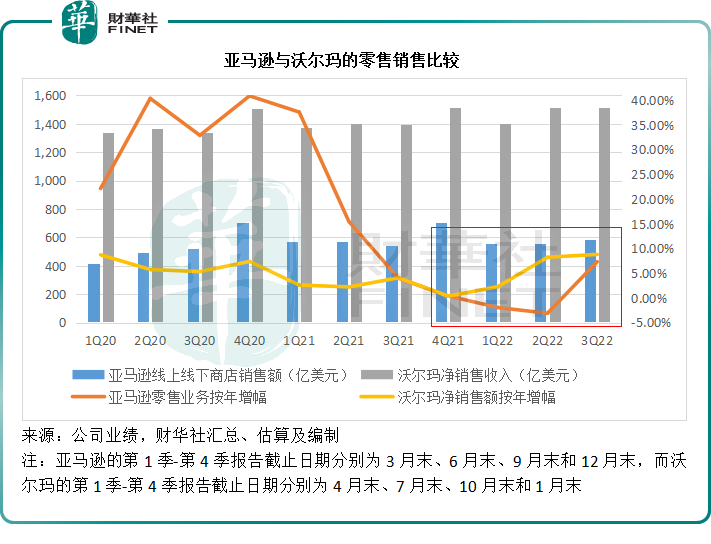

In the fiscal third quarter ended September 30, 2022, net sales in Amazon.Com Inc's online stores rose 7.10 per cent year-on-year to $53.489 billion, while net sales in brick-and-mortar stores rose 9.96 per cent to $4.694 billion.

Taken together, Amazon.Com Inc's self-operated online and offline stores generated $58.183 billion in sales, up 7.33 per cent from a year earlier. By contrast, Walmart Inc's net sales rose 8.81 per cent year-on-year to $151.5 billion in the fiscal third quarter ended October 2022, significantly outperforming Amazon.Com Inc.

See below, at the beginning of 2020, thanks to the sharp increase in online store sales, Amazon.Com Inc's retail sales rose sharply, but with the passing of the epidemic, in the face of the high base of the past two years, Amazon.Com Inc obviously felt the pressure of growth in the first three quarters of this year, with annual growth rates of-1.94%,-3.10% and 7.33% respectively (at a fixed exchange rate). In contrast, Walmart Inc's annual growth rate in the first three quarters was 2.28%, 8.23% and 8.81% respectively, obviously better than Amazon.Com Inc.

As can be seen from the picture, Walmart Inc's annual growth rate has remained stable. With the improvement of the epidemic this year, its retail sales have shown an upward trend, in contrast to Amazon.Com Inc's declining trend.

In order to please paying members, Amazon.Com Inc has invested heavily in content and implementation infrastructure in recent years.

In the first three quarters of 2022, Amazon.Com Inc's user service revenue rose 10.08% year-on-year to $26.029 billion, while its implementation cost rose 16.20% year-on-year to $61.196 billion, while technology and content expenditure rose 28.62% year-on-year to $29.42 billion. The increase in these two costs is significantly higher than the growth rate of user fees.

Retail-related revenue per unit of performance cost was only $4.52 in the first three quarters of 2022, compared with $5.03 in the same period last year. See the chart below, which shows that its cost efficiency is declining as compliance expenditure rises.

In the third quarter of 2022, Amazon.Com Inc opened several new compliance centers around the world, located in the United States, Mexico, Canada, Ireland and Turkey. Andy Gassi, CEO, said that steady progress has been made in reducing the online cost of compliance, and the cost structure will be strengthened in the future.

Obviously, even if Amazon.Com Inc cuts staff and costs, the growth in investment in compliance, marketing, technology and content will continue, but whether it can produce an effective effect of retail revenue growth is another matter.

More importantly, Amazon.Com Inc's retail business is not very optimistic in the foreseeable future.

The Fed's interest rate hike is aimed at curbing high inflation rarely seen in history. Hot retail consumption has driven the Fed to raise interest rates aggressively. In order to suppress consumption, narrow the gap between supply and demand, and thus keep prices down.

Simply put, the Fed's aggressive rate hike will have a negative impact on America's willingness to spend.

As a result, it can be foreseen that as the impact of the Fed's interest rate hike is gradually experienced in consumption, Amazon.Com Inc's retail business growth prospects in the next few quarters are not optimistic.

On the other hand, the strong dollar brought about by higher interest rates is not conducive to the trade advantage of US companies, which is why Amazon.Com Inc's international business sales fell 5 per cent in the third quarter of 2022 compared with the same period a year earlier. Excluding exchange losses, its international business actually grew by 12 per cent year-on-year in the third quarter.

In addition, Amazon.Com Inc also expects the impact of the exchange rate on its quarterly net sales growth of about 4.6 percentage points in the fourth quarter of 2022.

It can be seen that, whether at home or abroad, the growth prospect of Amazon.Com Inc's retail business is not very ideal.

Cloud Business: still dominant

As the world's most influential cloud computing service provider, Amazon.Com Inc's AWS business is a major factor in ensuring its profitability in the third quarter of 2022.

In the fiscal quarter at the end of September 2022, Amazon.Com Inc's cloud technology business revenue rose 27.49% year-on-year to US $20.538 billion, or 28% year-on-year in real terms, excluding exchange losses.

by contrast,$Microsoft (MSFT.US)$Revenue from Azure and other cloud services grew 35% year-on-year, excluding exchange rates, 42% year-on-year.$Alphabet-C (GOOG.US)$Cloud revenue rose 37.64% year-on-year to $6.868 billion.

The cloud computing business of these two technology companies is growing faster than Amazon.Com Inc, but in terms of revenue scale, Amazon.Com Inc's cloud business still occupies a large advantage and achieves stable profits.

Despite Microsoft Corp and Google's rapid revenue growth, their profitability does not seem to be a threat. Microsoft Corp's Azure business is usually less profitable, so the increased revenue contribution of the business has also dragged down the overall profit margin of its cloud and server-related business. Google's segment loss in the third quarter of 2022 increased by 8.54% year-on-year to $699 million, with a loss rate of 10.18%, an improvement from 12.91% in the same period last year.

In the third quarter of 2022, Amazon.Com Inc's cloud business division's operating profit increased by 10.65% year-on-year to US $5.403 billion, completely offsetting the operating losses of its North American business and international business of US $412 million and US $2.466 billion respectively, while Amazon.Com Inc continued to achieve a quarterly operating profit of US $2.525 billion.

Amazon.Com Inc's cloud business operating profit margin reached 26.31% in September 2022, down 4 percentage points from the same period last year and 2.65 percentage points from the previous quarter.

In the nine months ended September 30, 2022, Amazon cloud revenue rose 32.18% year-on-year to $58.718 billion, operating profit increased 33.21% year-on-year to $17.636 billion, and segment operating margin rose 0.2% year-on-year to 30.04%.

See below, Amazon.Com Inc's cloud technology business (AWS) does not account for the largest share of his overall revenue.

However, the operating profit of the cloud business is the highest, offsetting the negative impact of Amazon.Com Inc's poor retail business performance, as shown in the chart below.

At present, the concern of the market for Amazon.Com Inc's cloud technology business is that its superior operating profitability is sustainable.

As can be seen from the chart below, the operating profit margin of Amazon's cloud technology business does not seem to have changed much in the past three years. As other large technology companies use their own technology to promote the growth of cloud computing business, it is unknown how long Amazon.Com Inc's cloud technology business can maintain its profitability.

Gartner, a research firm, predicts that the trend of companies going to the cloud will not end, but in the short term, companies may cut back on IT due to inflationary pressures and an uncertain macro outlook. Since cloud computing usually accounts for the majority of IT expenditure, it also means that capital expenditure on cloud computing is likely to decline in the short term.

Summary

In the face of uncertain short-term prospects, Amazon.Com Inc is not very optimistic about the growth space of both retail business and cloud technology business. It is based on this that the market pushes it.

In terms of valuation, Amazon.Com Inc's price-to-sales ratio is higher than that of traditional retailer Walmart Inc and Chinese counterpart JD.com, or reflects the premium advantage of its cloud technology business.

Amazon.Com Inc expects fourth-quarter net sales to range from $140 billion to $148 billion, an increase of between 2% and 8%, with exchange rate effects of about 4.6%. This means that income growth will slow further in the fourth quarter-14.70 per cent in the third quarter; the operating profit in the fourth quarter is expected to be 0-4 billion US dollars, compared with 3.5 billion US dollars in the same period last year.

The impact of the Fed's rate hike is likely to be reflected in consumer sentiment from next year, as Amazon.Com Inc's retail business lags behind Walmart Inc's performance and the cold winter of technology companies is approaching, while the impact on its cloud technology business will put pressure on its valuation. On the other hand, if the attitude of the Federal Reserve turns, Amazon.Com Inc is more likely to rebound due to a large cumulative decline.

All in all, Amazon.Com Inc's current risk coefficient is relatively higher than other technology stocks, which is the main reason why he is out of favor with investors.

Edit / Viola