As the Federal Reserve and other central banks around the world continue to raise interest rates this year, interest rates in many countries have reached high levels. The huge impact on the economy, high inflation and so on make a number of commodity prices lower this year, so how to invest in commodities next year?

Global bulk performance this year

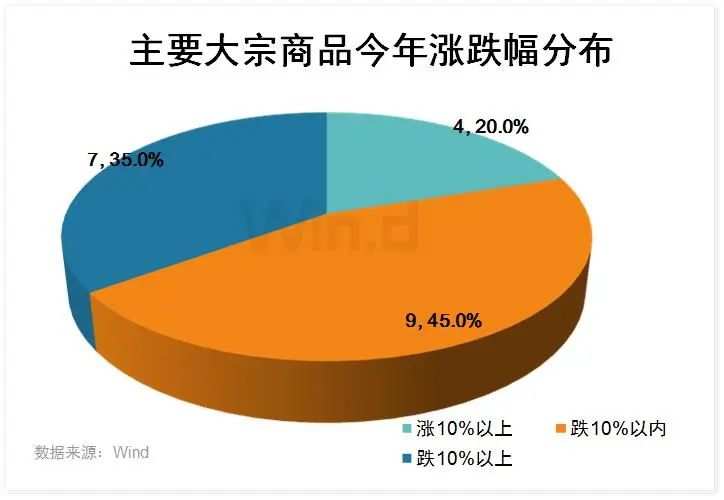

Affected by the global economy and demand, the vast majority of commodities have fallen this year. In terms of 20 major commodities, only natural gas, nickel, iron ore and soyabeans have risen so far this year, all by more than 10 per cent, according to Wind. The other 16 commodities fell, with metal tin falling by as much as 37%. In addition, coking coal, copper and rubber also fell by more than 10%. On the whole, commodities have risen less and fallen more this year, but a few varieties have risen sharply.

A list of specific performances:

Prospects for the direction of bulk investment next year

Analysis of Citic Futures qu Tao believes that there are two main lines of commodities in 2023:

1. Overseas recession is inevitable and aggregate demand is falling, so we are bearish on overseas macroscopically priced commodities (crude oil, copper).

2. The economic cycle mismatch between China and the United States, under the pessimistic expectation of "low inventory + low profit", it is more cost-effective to find a low point to do more domestic black rebound, but it needs to be verified by micro data constantly.

Energy:It is recommended to focus on short opportunities in crude oil prices, while coal may only be in a state of volatility. First, we predict that the probability of a future US recession is close to 100 per cent; in addition, the Fed's long-term inflation expectations are related to high WTI oil prices, falling back to 2 per cent corresponding to WTI oil prices in the range of 46-77 US dollars per barrel, while the fiscal break-even oil price of the major OPEC producing countries is around 65.80 US dollars per barrel (equivalent to WTI oil prices of 70 US dollars per barrel). Against the backdrop of all-out efforts by the US government and the Federal Reserve to control inflation, it may be difficult for US crude oil prices to exceed $80 a barrel for a long time next year.

Colored:The overall supply of non-ferrous metals is expected to be loose, and global economic growth is slowing, putting overall prices under pressure. However, the possible bright spots on the demand side are the expectation of domestic real estate regulation, the resilience of infrastructure, the construction of new energy industry or restricting the downward space of varieties. The opportunity for copper prices to fall in the first half of the year is recommended here.

Precious metals:Monetary tightening stops in the middle of next year, superimposed recession expectations, precious metals may rise. Silver may perform better than gold. Gold is at a low of $1700 an ounce and silver is at a low of $20.40 an ounce.

Black:Under the background of "low inventory + low profit", the black of domestic pricing is better than the expected rebound at the very low bottom, which is consistent with the direction of domestic policy, but needs the support of micro data.

Minsheng Securities Mou Yiling and Hu Yue thinkIn the coming year, gold is most directly supported by currency valuation attributes, considering that the copper-to-gold ratio and oil-to-gold ratio are still undervalued relative to US debt interest rates, the positive contribution of copper and oil to the weakening dollar will not be significantly weaker than gold.

From a supply and demand perspective, oil now has a stronger reality (supply and demand is relatively tight) and a moderate marginal change; copper has a relatively weak reality (demand is weak and supply will still increase in 2023). But there is a greater marginal possibility (energy release of European demand, domestic economic recovery, and lack of new capacity after 2024 is good for equity asset pricing).

Edit / lydia