Source: Gronghui column: Fu Yifu; author: Fu Yifu

The situation is changing.

Recently, news about the optimization of epidemic prevention and control programs has been heard from different regions almost every day: first, on November 30, various districts in Guangzhou adjusted their epidemic prevention and control measures to remove temporary control zones; then, similar marginal relaxation policies have occurred in Beijing, Shenzhen, Chongqing, Shanghai and other regions. And the Xinhua News Agency even published an article saying"the most difficult period of fighting the epidemic has passed," and "China's epidemic prevention and control is facing a new situation and new tasks."Let more and more people really feel that it is really getting closer and closer to getting back to normal life.

Affected by this, the A-share consumer sector has strengthened collectively recently, and under its "assists", the Shanghai Composite Index has regained its 3200 points after a lapse of nearly three months, and there have been more arguments about the "starting point of the bull market" in the market.

So can the big consumer sector continue to be strong in the coming 2023?

I. Review of the market of large consumer sectors in 2022

Looking back at the consumer market in 2022, the epidemic must be an unavoidable factor.

In fact, since the outbreak of the COVID-19 epidemic in 2020, the disturbance to the consumer market has never stopped. This year, the Omicron mutant blossoms repeatedly in China. Due to the shortening of the incubation period and the rapid spread of the virus, the domestic epidemic situation is widespread and frequent, which greatly increases the difficulty of prevention and control. Under the objective requirements of the general policy of "dynamic zero clearance", strong closure and control measures have been taken repeatedly in many places, resulting in the hindrance of human flow and logistics, and the reduction of many offline service consumption scenes with the attributes of travel and crowding. some enterprises continue to encounter resistance.

At the same time, under the effect of the long tail effect of the epidemic and uncertainty in the future, the stability of work income of many people has been affected, especially the low-and middle-income groups with wages as the main source of income are more cautious about their expectations for the future, resulting in a significant decline in consumer confidence and weak willingness to spend.

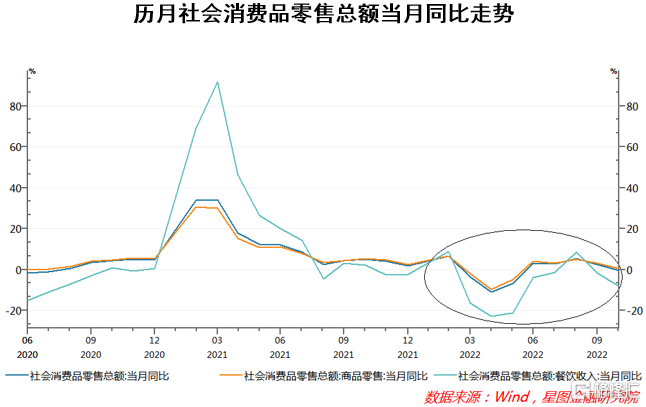

Reflected in the data, it is the unsatisfactory performance of the total retail sales of consumer goods. Wind data show that from January to October this year, the cumulative growth rate of retail sales of consumer goods across the country was only 0.6% year-on-year, far lower than the 8.1% growth rate in the same period in 2019 before the epidemic. According to monthly data, four of the first 10 months of this year were negative compared with the same period last year, and the catering sector, which was heavily affected by the epidemic, had seven months of negative income growth.

At the same time, the recurrence of the epidemic has also seriously suppressed people's travel, causing a heavy blow to the tourism industry. According to the survey results of domestic tourism sampling conducted by the Ministry of Culture and Tourism in the first three quarters of 2022, the total number of domestic tourists in the first three quarters of 2022 was 2.094 billion, down 22.1% from the same period last year, and only 45.6% in the same period in 2019, less than 50% of that before the epidemic. Domestic tourism revenue in the first three quarters of 2022 was 1.72 trillion yuan, down 27.2 percent from the same period last year, and only returned to 39.48 percent in the same period in 2019, less than Chengdu.

It is precisely because of the above reasons, the overall performance of the A-share consumer sector is relatively weak so far this year. If you only look at the trend from January to October, major sectors such as trade and retail, food and beverage, beauty care, and social services have all fallen by more than 20%, with food and beverages falling by nearly 35%.

It is worth mentioning that in addition to the sluggish consumer demand caused by repeated epidemics, some companies have also faced the problem of rising prices of raw materials in the upper reaches of the consumer goods industry, such as commodities, agricultural products, and packaging materials, in the past two years, which has put continuous pressure on business performance and the company's share price has gone from bad to worse. Typical "soy sauce grass" Haitian flavor industry, since last year, the company's performance began to "stall", 2021 revenue and net profit growth of only 9.71% and 4.18% respectively in the first three quarters of 2022 fell to 6.11% and-0.86%, of which the net profit of home showed negative growth, which is surprising. This led to the "Davis double kill" effect of earnings and valuation, and the share price fell all the way.

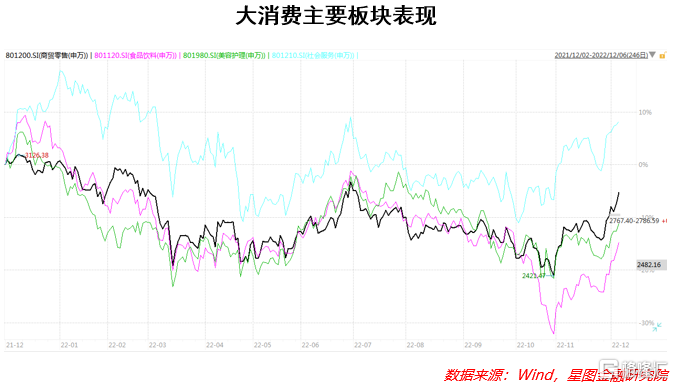

However, since November, with the continuous optimization and improvement of epidemic prevention and control measures in various parts of the country, the market's expectations for the follow-up consumption trend are quietly changing, and as a result, the large consumer sector has rebounded strongly in the past month or so. among them, the maximum rebound in food and beverages is close to 30%, and trade, retail, beauty care and other segments have also performed well.

II. Consumer Market and Market Prospect in 2023

Looking forward to 2023, will the big consumer sector continue its recent rally?

From a fundamental point of view, with the continuous optimization and improvement of epidemic prevention measures in our country, the unfavorable factors that once disturbed the operation of various industries will be weakened day by day. At the same time, the just-concluded meeting of the political Bureau of the CPC Central Committee stressed the need to "do a good job in economic work next year,"better co-ordinate epidemic prevention and control and economic and social development, better co-ordinate development and security, comprehensively deepen reform and opening up, and vigorously boost market confidence." this fully demonstrates the determination of the senior level to resume the operation of the national economy in 2023.

Considering China's solid economic foundation, complete industrial system and strong economic resilience for a long time, the strong rebound of the economy next year should be a deterministic event. According to Goldman Sachs Group's forecast, China's GDP growth rate will increase from 3.0% this year to 4.5% in 2023, while Morgan Stanley, Citibank, UBS and other institutions claim that China's GDP growth rate can reach 5% or higher in 2023, which is enough to show market confidence and expectations for our economy.

In this way, consumption with strong pro-cyclical attributes is also expected to hit bottom and rebound.

In fact, from a macroeconomic perspective, China's export momentum is weakening as the world's major economies fall into recession. In November 2022, China's dollar-denominated exports fell 8.7% year-on-year, while imports fell 10.6%. At this time, it is necessary to force the policy side to quickly release the space of domestic demand in order to strengthen the driving force of economic growth, and the importance of consumption will be further highlighted. It is expected that a series of policies to promote consumption will continue to be introduced next year, including issuing consumption vouchers, supporting automobile consumption, promoting the consumption of green smart home appliances, and so on, in order to tap the consumption potential of the broad masses of residents.

In addition, the "deregulation" of epidemic prevention and control is a general trend, which also plays a positive role in boosting the consumer market. In theory, the previous strict epidemic prevention measures directly restricted the consumption scene of offline crowds and travel, so after the gradual liberalization, catering, tourism, offline retail and other areas are expected to usher in a strong recovery, which will directly lead to the recovery of the entire consumer market.

However, it should be noted that, referring to the experience of other overseas countries, the accelerated repair of offline consumption mostly occurs in the second quarter after the optimization of the prevention and control policy, rather than immediately; and from the adjustment of the control policy to the basic return to normal consumption, it also needs to go through a cycle of 3 to 4 quarters.

Combined with the current actual situation in China, affected by the inertia of strict epidemic prevention in the early stage, some people have not yet subjectively fully adapted to the latest concept of epidemic prevention, coupled with the fact that the number of new cases across the country is still high, and it is likely to continue to increase, making many people still hold a cautious wait-and-see mentality. Therefore, in the short term, the impact and impact of the epidemic on consumption will continue for some time, and even if the consumer market rebounds, the strength may be limited. If we follow the pace of overseas consumption repair, we may need to wait until the second or third quarter of next year, after all aspects of the situation has really stabilized, the overall boost to the consumer market will really appear.

Based on the above logic, the large consumer sector is expected to become one of the main investment lines throughout the year in 2023, and with the continuous changes in the macroeconomic situation and the impact of the epidemic, the large consumer sector may gradually evolve from the expected drive in the first half of the year to the fundamentals of the second half of the year, and the rising market is also expected to continue.

III. Allocation Strategy of large consumption sector in 2023

At the specific configuration level, investors are advised to focus on following four major directions:

First, the flexible subdivision of the field.

As mentioned earlier, the big consumer sector is expected to usher in a fundamental reversal in 2023, and its valuation is also expected to be repaired. Considering that the focus of valuation repair is on the segments where the valuation discount is serious, we might as well pay attention to those industries that were relatively heavily affected by factors such as the epidemic, including airlines, airports, hotels, catering, tourism and other subdivisions with travel and crowd attributes. In the follow-up, with the further optimization and relaxation of the domestic epidemic prevention and control program, these areas will directly benefit and usher in a reversal of difficulties, and the power of valuation repair is relatively stronger.

Second, the medical supplies needed for family epidemic prevention.

With the increasing popularity of the concept of "being the first responsible person for one's own health", more and more families begin to consciously hoard some household epidemic prevention materials, and the related demand is expected to further increase in the future. and then support the continued upward of the relevant sectors. It is suggested to configure it around cold medicine, traditional Chinese medicine, antigen self-test, as well as related medicine circulation, chain drugstores and other fields.

Third, growth optional consumer goods.

Different from the necessary consumer goods, the optional consumer demand is not stable and is more sensitive to the economic cycle, while the consumer category which is greatly affected by the epidemic and other factors in 2022 is also concentrated in the optional consumption field. Compared with the compulsory consumption, the optional consumption is often the main support direction of the policy side. In the follow-up, with the change of the concept of epidemic prevention, the recovery of the national economy and further support at the policy level, optional consumption is expected to usher in a strong rebound, and the profitability of related companies will also usher in a rapid marginal repair. it is recommended to pay attention to cosmetics, medical beauty, light consumer goods and other growing varieties.

Fourth, high-quality assets.

The consumer sector has never been short of high-quality assets, such as Maotai, Wuliangye and Luzhou laojiao in high-end spirits, Yili shares in dairy products, Gree, Midea and Haier Smart Home in home appliances, tablets in traditional Chinese medicine, Yunnan Baiyao, and so on. Fundamentally speaking, these high-quality assets will have very high investment value for a long time in the future, not to mention that many of them have undergone a great adjustment, and the performance-to-price ratio has been highlighted. In the future, with the continuous relaxation of the control of the epidemic and the repair of public consumer confidence, the valuation of the above-mentioned high-quality assets will still have strong support. Investors are advised to use medium-and long-term thinking to find bargains and hold them patiently. I believe you can get a good return.

Edit / Corrine