Author: Wang Jian

Source: Guoxin Securities

Original title: "[essay] the riddle of low bank valuations: from the bank's own point of view"

The ability of domestic bank management to manage new risks has not been recognized by the market. The risk here does not only refer to a certain business risk, such as non-performing loans, but "new risk". It refers to whether the development of banks can adapt to future environmental changes in the process of the transformation of the overall economic model.

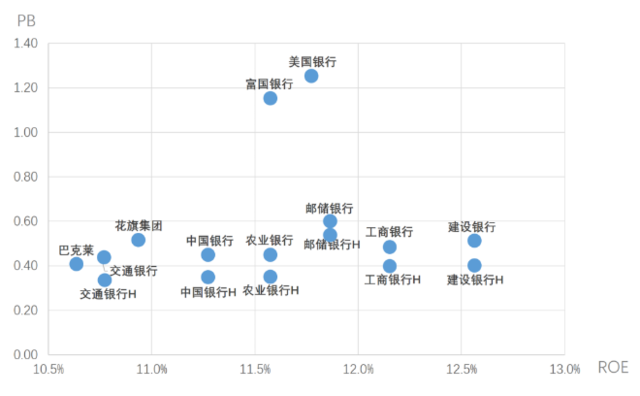

A-share bank shares continue to be undervalued, and what is even more unacceptable is that many high-quality A-share banks are valued at lower valuations than many large overseas banks that are less profitable, which cannot be explained under the PB-ROE framework. To this end, people from all sides of the market give various explanations.

The issue of bank valuation is not a hot academic topic, only a small number of papers are also banking practitioners, there are not many academic achievements.

This paper introduces a paper entitled "Discussion on the importance of Bank Market capitalization and Bank of China Ltd. 's low valuation"(hereinafter referred to as" this article "), the writer is Dr. Huang Zhiling, then chief economist of China Construction Bank Corporation, published in Credit magazine (sponsored by Zhengzhou training Institute of the people's Bank of China) in January 2021.

Based on the fact that the performance of bank stocks in China is acceptable but the valuation is very low, this paper discusses the reasons behind it and some thoughts on the work of bank market capitalization.

This article is divided into three parts (this article is divided into four parts), the logic is concise and clear, showing us an interpretation of the issue of low valuation from the perspective of the bank's internal management.

How to treat the market capitalization of banks

This paper points out that the market value or valuation of a bank represents the market's comprehensive understanding of the development prospect of a bank, and in the long run, it can be used as a good evaluation index, so it should be paid attention to by all parties.

Bank evaluation has always been a difficult problem in the industry. Because the bank's indicators cover all aspects. The essence of the operation of commercial banks is three-sex balance (profitability, liquidity, security), so we can not simply use a dimension of profit, but also take into account risks or other. Usually, when we do bank analysis, asset scale, profitability, risk control, social responsibility and other aspects will be involved, so it is difficult to use one or two indicators to evaluate "who is better than who".

In order to solve this problem, various so-called comprehensive evaluation systems are developed in the industry, and the principle is roughly the same: some representative indicators are selected in all aspects of the bank, and then each index is given a certain weight, and then weighted and summed up. Get a comprehensive score (or rating). Then use this comprehensive score to evaluate "who is better than who". For example, the earliest "CAMEL" rating, the regulatory rating of the Banco Insurance Regulatory Commission, the financial institution rating of the people's Bank of China, and the "top evaluation system" of the Banking Association are generally this routine. Our team has also developed a bank credit evaluation system, that is, to find a bunch of indicators that we think are more important to the bank's credit risk, empower summation and get ratings. See the June 2022 report, Bank Credit risk Analysis: framework and Model.

This set of evaluation system requires a small range of experts to artificially select indicators and set weights, so it is impossible to be completely accurate, and sometimes there will be some results that are not consistent with the intuitive feeling. To this end, we can change the way of thinking: not by a small range of experts to evaluate, but to pull the bank to the market "slip around", let the market to evaluate. Banks themselves disclose all kinds of data and information, and put them in front of the whole market, which will be comprehensively evaluated by Mr. Market. Market capitalization or valuation is a result of Mr. Market's comprehensive evaluation.

Of course, markets can make mistakes and even be manipulated in the short term. But in the long run, it is reliable, at least more reliable than a small range of experts?

Therefore, market capitalization or valuation is also a comprehensive evaluation of banks. Deduced from the point of view of this article, the bank management should not ignore the market value and feel that if they run the bank performance well, they can report to their superiors, but should be deeply aware that if the market value is so low, it must reflect some problems. You can't ignore it. It is gratifying to see that the policy authorities have also made market capitalization one of the assessment contents of state-owned enterprises.

There is no single attribution.

The article goes on to point out that since valuation is also a comprehensive evaluation given by the market, the undervaluation cannot be attributed to one or two factors (that is, one or two indicators of banks cannot be used to explain its low valuation). And this single attribution method happens to be used by our securities analysts in the past.

The background at that time was that the operation of banks in all aspects was OK, and there were not too many particularly negative indicators, but there was only one indicator that was relatively negative, that is, there were more non-performing loans. So if a bank's PB is less than 1 times, say, to 0. 8-0. 9 times, it implies that the market believes that the bank's net worth is inflated and watery. The part of the discount is the hidden non-performing loans. If this part of the "hidden bad" is exposed, then the bad rate of banks could reach 8%.

This method cannot be used when PB falls below 0.7x or even lower. Because according to this method, when the PB level is low, the defect rate is extremely high, and some stocks may even be as high as 20% or more. The failure rate of these mainstream banks listed in China will never reach this level (at least most of them will not). It can be seen that the poor hiding can no longer explain the extremely undervalued value.

So the article needs to answer a central question: so why are bank valuations so low?

The reason for the low valuation

This paper directly gives the point of view: the ability of domestic bank management to control new risks has not been recognized by the market. The risk here does not only refer to a certain business risk (such as non-performing loans), but "new risk", which refers to whether the development of banks can adapt to future environmental changes in the process of changing the overall economic model.

Many of the environmental changes we have learned in school (marketization of interest rates, financial internationalization, financial disintermediation, direct financial development, etc.) are now really happening. To tell you the truth, these things happened later than expected. after all, we were learning these things when we were in college 20 years ago (the United States and other western developed countries had already experienced it at that time). But it is disappointing that we started shouting about these things 20 years ago to let banks practice all kinds of "internal skills". Today, many of our banks are still not fully prepared. This has to be said to be a pity and a very urgent task. Now the country is promoting a higher level of opening up to the outside world, if its wings are not hard, you can't find the north when you fly out.

Of course, this does not obliterate that China's banking industry has made great progress in the past decade. However, the times are also improving, and so are the excellent overseas banks, so we cannot be complacent on our existing transcripts.

In short, our bank, although the current performance is still very good, but the business model, management model (internal skills) is still not advanced enough, and can not fully adapt to the new economic development environment (at least the market can not confirm the capacity of banks). As a senior executive of a large bank, the author regards this as the main reason for explaining the low valuation of the bank from the perspective of the bank itself. This is a great inspiration for us "external eyes".

This article lists some of the capabilities that banks do not yet have but are urgently needed in the new environment, including:

(1) to restrict and encourage effective corporate governance, especially in terms of incentives, we should learn from overseas and change the existing rigid compensation.

(2) the ability to change internal structures, processes and mechanisms to truly be customer-centric.

(3) many banks still lack the ability to deal with globalization, including specific businesses such as RMB derivatives, market services, global financial services, wealth or asset management capacity.

From these angles, we do admit that the capacity of many banks in our country is indeed lacking. Although the performance is OK, if the ability does not keep up, there is no guarantee that the future performance will continue to be good, and sooner or later it will become a "dinosaur" that is about to become extinct in the new economic environment. Compared with overseas, of course, their banks are not all good (and uneven), but some cases make us sigh. For example, some very small banks, and even small banks in the town, although the sparrow is small, with all the internal organs, the business philosophy and business model are very standardized. For example, the Bank of America we tracked last time, a very small bank, the wealth business model is very mature. Please refer to "the way for small and medium-sized banks to create characteristic wealth management".

Therefore, through the "superficial" figures of financial performance, to look at the underlying capabilities of domestic and foreign banks, there is indeed a gap, which may explain our very low valuation. Of course, there is no need to belittle yourself. There are also a number of excellent banks in our country.

Attach importance to the theory and practice of market capitalization management

This paper also puts forward some thoughts on market capitalization management. If a bank has a good market capitalization, it will have many benefits, which in turn will promote its own development. The market capitalization is good, which itself is a reflection of the comprehensive evaluation of the bank. At the same time, it can increase the difficulty of being acquired, reduce the difficulty of other acquisitions, and reduce the cost and difficulty of financing at the same time. Even, there are real cases of high-quality banks in China that have increased their popularity in the business community (investors know it) because of their high market capitalization and large increases.

At the end of the article, several points are mentioned:

(1) Market capitalization is a comprehensive evaluation, not an evaluation of some indicators, and it is of little significance to deliberately optimize some popular indicators (such as increasing the proportion of income and wealth business, etc.), but to improve the overall quality of the bank. the whole bank strives for the overall strength.

(2) improve corporate governance and clarify the division of market capitalization management.

(3) strengthen customs clearance and take the initiative to communicate with investors (some banks have established a regular communication mechanism with investors and analysts, which is worth using for reference)

(4) effective use of market capitalization resources and capital operation

(5) to establish a good image of the capital market.

(6) put an end to pseudo-market capitalization management behaviors such as stock price manipulation.

It is true that more and more banks are beginning to attach importance to these jobs.

Because, in the previous article, the point of view of the paper is that the ability of domestic bank management to control new risks has not been recognized by the market. In other words, our bank does not necessarily lack these capabilities, it may also be: in fact, the ability gradually has, but the market still does not know, can not see …...

Just because these abilities are very inherent abilities (so they are called "internal skills"), it is difficult to simply use one or two indicators to show this ability to the market.

For example: I am often asked which bank has better financial technology.

This kind of question is almost impossible to answer. The ability of financial technology is a typical internal skill, and it is difficult to make a simple comparison.

This is the test of the ability of market capitalization management.

Edit / irisz