The main content of this paper is comprehensive from Guotai Junan Securities Research and CICC finishing Point.

As we all know, since the beginning of this year, under the strong increase in interest rates by the Federal Reserve, the global economy has ushered in a new economic cycle. Among them, Hong Kong stocks gradually fell into the quagmire of low liquidity, the Hang Seng Index repeatedly hit new lows, and the mentality of investors bravely copying the bottom was exhausted again and again.

But since the low of the year at the end of October, the mood has gradually improved, and Hong Kong stocks have rebounded by more than 20% so far.

While rejoicing that Hong Kong stocks are finally expected to get out of the haze, investors are also concerned about whether this wave of "valuable" rally in November can continue into next year. After all, the current multiple indicators of Hong Kong stocks have reached extreme levels. At the current level, it is not difficult to expect a rebound, the key is sustainability? How to grasp the rhythm and direction?

After looking at the institution's outlook for stock market performance in 2023, we found thatMost institutions believe that after two years of decline, the bottom of the probability of Hong Kong stocks has been identified. Recently, the inflationary inflationary point in the United States and the domestic real estate epidemic policy have also undergone marginal changes, and some repair opportunities for Hong Kong stock sentiment and valuation have gradually emerged, which will usher in some room for repair.

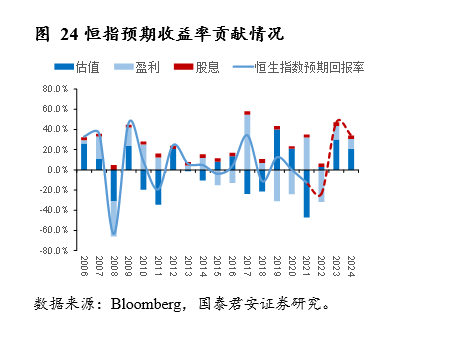

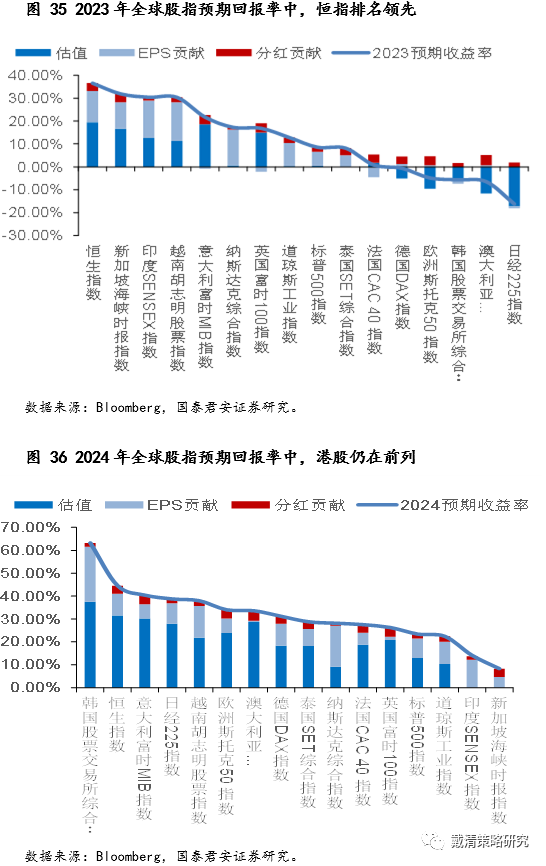

Guotai Junan: Hong Kong stock Hang Seng Index is expected to return 36.6% in 2023, or lead the world.

Guotai Junan's overseas Daiqing team pointed out that since most of the components of the Hang Seng Index are state-owned enterprises and red chips, the economic situation in mainland China will significantly affect the profitable performance of the Hong Kong stock market. Under the combined effect of the overseas interest rate hike and contraction table and the pressure on the Chinese economy, the Hong Kong stock market will face downward pressure of resonance between earnings and valuations in 2022.

However,At present, there are signs that overseas inflation has peaked, and major overseas central banks may stop tightening monetary policy in 2023; at the same time, China's economy stabilizes and most likely rebounds in 2023, and the gap between China's economic growth and other global economic growth is likely to widen. Hong Kong stock market will usher in the profit end and valuation side of the repair rise.

On the basis of the above assumptions, Guotai Junan overseas Daiqing teamThe Hang Seng Index is expected to return 36.6% in 2023.Among themPartial repair of valuationAnd profit growth will be respectivelyPull 19.4%And 13.7% of the Hang Seng Index's expected return, and the remaining 3.5% contribution comes from the Hang Seng Index's expected dividend yield.

The possible shift in the Fed's monetary policy and the possible improvement in the economy after the gradual optimization of China's epidemic prevention policy and other positive risk appetite may prompt the flow of money to Hong Kong stocks and usher in its valuation repair.

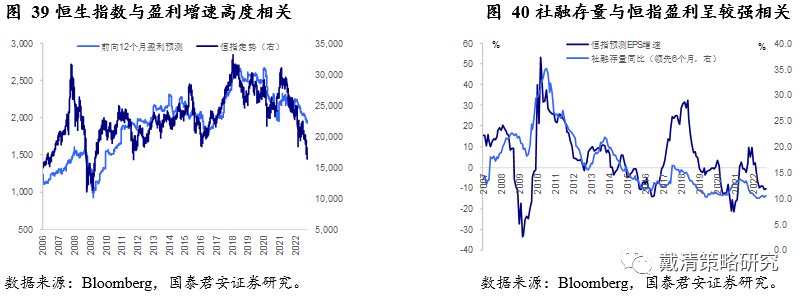

In contrastHistorical trend and profit Forecast of Hong Kong Stock IndexAfter that, Dai Qing's team also found that两The trend of people is highly related.

If domestic policies continue to increase in the future, with social integration gradually bottoming out and picking up, it is expected that the performance of Hong Kong stocks will also bottom out in 2023 and the Hang Seng Index will have a bright performance in 2023.

When earnings expectations are expected to bottom out and pick up, overseas funds will provide more momentum to rise.

Dai Qing's team observedAt present, the option opening of the global bullish on the Chinese market is at an all-time high.The reason is that overseas investors believe that after the optimization of China's epidemic prevention and control policies, profit repair is expected to bring about a recovery deal. Once the epidemic improves and the profit outlook improves, overseas funds will continue to flow into Chinese assets.

CICC: it is estimated that there will be 20% to 25% repair space for Hong Kong stocks in 2023.

The CICC team pointed out that after nearly a year of decline in 2021, Hong Kong stocks fell further in 2022 than most expected. If calculated from the beginning of 2021, this round of decline has been more than 19 months, the longest downward cycle in history, and the decline is second only to the 2008 financial crisis and the Asian financial crisis. From all dimensions, Hong Kong stocks have reached a more extreme level.

On the whole, CICC expects a turnaround in Hong Kong stocks.There may be 20% "25%" room for repair in 2023, based on 6% "10% profit growth and 12%" 18% valuation.

Rhythmically, it still needs time to move. Recent changes in policy expectations at home and abroad have brought some signs of a turnaround. The Fed stopped raising interest rates in the first quarter or brought more downward interest rates and valuation repair opportunities for US debt; after the second quarter, focus on the prospects and sustainability of earnings repair.

Performance expectation and Rhythm judgment of Hong Kong Stock Market in 2023

Source: Bloomberg, China International Capital Corporation Research Department

In terms of capital, despite the downward trend in the Hong Kong stock market this year, southward capital inflows have continued steadily. Since the beginning of the year, southbound capital has flowed into HK $366.8 billion (vs. HK $454.4 billion in 2021 and HK $673.1 billion in 20 years). CICC believes that the reason for the continued inflow of southward funds is thatDomestic monetary policy is loose, exchange rate hedging and high dividend risk aversion.

At present, as the allocation ratio of emerging and global funds to China is significantly on the low side, and the further outflow pressure under the benchmark situation is manageable, but the return of China's fundamentals is the main premise.

At present, the main foreign investment is low for the Chinese market.

Source: EPFR, China International Capital Corporation Research Department

Under the assumption of neutral and optimismIf the Fed's retreat and domestic fundamental repair are achieved, if 30 per cent of investment institutions that track emerging markets adjust their allocation from low to standard, it could generate inflows of $7.2 billion.

CICC believes that Hong Kong stocks are currently under "triple pressure": the geographical situation affects risk appetite (the situation in Russia and Ukraine in March and the turmoil in Chinese stocks), China's growth affects corporate profits (the local epidemic in Shanghai in April-May), and Fed tightening affects financing costs and liquidity (US debt interest rates rose rapidly after August).

The division of the trend of Hong Kong stocks since the beginning of the year and the comparison of multiple influencing factors

Source: Bloomberg,FactSet,Wind, China International Capital Corporation Research Department

At present,Considering that these three pressures have been reflected in the price in turn.Recently, the inflection point of inflation in the United States and the domestic real estate epidemic policy have also undergone marginal changes.Part of the turnaround in Hong Kong stock sentiment and valuations will gradually emerge, but the sustainability of the rebound will require the cashing of molecular-side profits and the subsequent coordination of more policies (in the second half of next year).

In the direction, CICC pointed out that on the basis of high dividends, focus on high-quality growth (low PEG), such as consumption and real estate under policy optimization, high-tech manufacturing, expected reverse repair of the Internet and medicine. Pay long-term attention to the thematic opportunities for Hong Kong's new policies and institutional reforms.

Edit / phoebe