Source: Wall Street

Author: Zhao Ying

Cautiously optimistic but also risky.

As 2022 draws to a close, looking back on the past year, global economic growth has slowed sharply and recession fears have been growing under multiple pressures such as the weakening boost of reopening, the intensification of fiscal and monetary tightening policies, and the impact of the conflict between Russia and Ukraine on the energy landscape.

Looking forward to 2023, "recession" will become one of the unavoidable topics. Which countries will not be spared and which will be avoided?

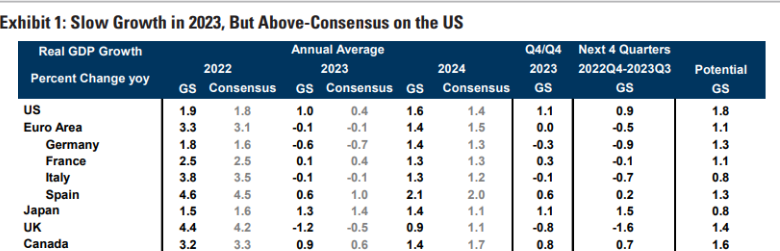

Last week, Goldman Sachs Group released the Global Economic Outlook report 2023.The global economy is expected to grow at 1.8 per cent next year, pointing out that the US economy is resilient and may barely avoid recession; Europe may fall into a mild recession and inflationary pressures persist; and emerging market economies are resilient and will avoid a deep recession.

At the same time, the uncertainty will continue, Goldman Sachs Group pointed out.We need to pay attention to the two major risks of "whether inflation can go down" and "whether interest rate increases will go too far", and political and geopolitical risks can not be ignored.

Us: may avoid recession the Fed remains a hawk for a long time

Goldman Sachs Group economist Jan Hatzius team pointed out in the report that real disposable income growth is expected to remain strong next year, the probability of the US economy falling into recession is only 35%, may be able to avoid recession.

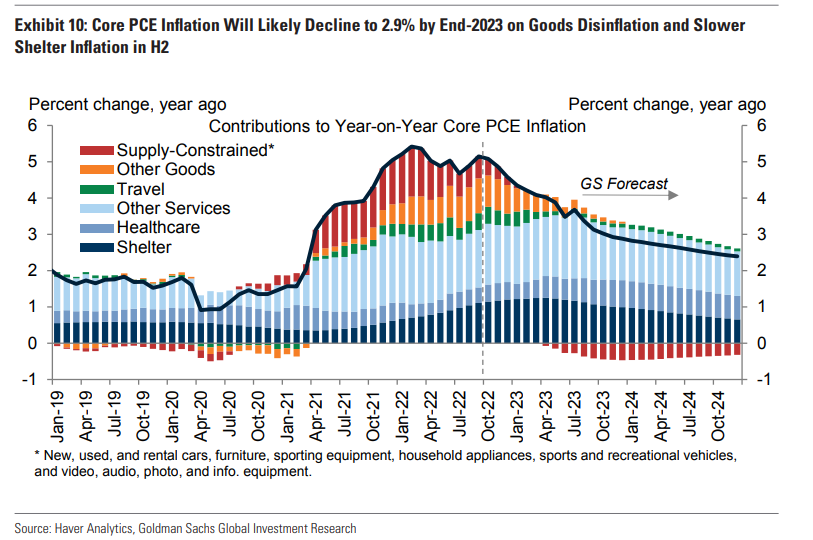

Inflation in the United States will fall sharply next yearCore PCE is expected to slow from 5 per cent now to 3 per cent by the end of 2023, but the unemployment rate is only half a percentage point higher.

However, the Fed will not become a dove, and the situation of "long-term high interest rates" will continue.. Goldman Sachs Group expects the fed to raise interest rates by 125bp to a peak of 5.25 per cent, and will not cut rates in 2023.

1. The US economy may be protected from recession

This year, US economic growth slowed significantly, falling real disposable income (affected by the withdrawal of fiscal stimulus and high inflation) and aggressive monetary tightening, which was 1 per cent below potential growth, as the impetus for reopening weakened.

Goldman Sachs Group predicts that the economic growth rate in 2023 will be roughly the same as this year, and the current forecast for 2023 is much higher than the consensus expected.

In addition, the difference between Goldman Sachs Group and general expectations on the probability of recession is even greater and higher.Sheng expects the US economy to enter a recession of 35 per cent in the next 12 months, far below the media survey's median of 65 per cent, which is almost the lowest probability shown in the survey.

The 35% probability means that Goldman Sachs Group thinks the United States is unlikely to fall into recession, which gives two reasons:

One immediate reason is that economic data show that there is a considerable distance from recession.DistancGDP maintained growth, and real GDP in the United States increased by 2.6% in annualized quarter-on-quarter in the third quarter. Employment remained resilient, and non-farm payrolls in the United States increased by 261000 in October.

More importantly, there are good reasons to expect positive economic growth in the future. It is undeniable that the tightening of the financial environment is putting heavy downward pressure on the economy, accounting for about 0.02% of economic growth.But real disposable income is rebounding from fiscal tightening and soaring inflation in the first half of the year.Inflation core PCE may slow to 3% by the end of next year.

2. This cycle of high inflation is different.

Goldman Sachs Group is optimistic that he expects the Fed to cut core PCE by 2 per cent next year with unemployment rising by just 0.5 per cent.

This seems to run counter to previous cycles of high inflation, especially under Paul Volcker in the 1970s, when unemployment rose sharply.

Goldman Sachs Group's answer is that today is different from the previous cycle of high inflation:

First, the overheated labor market is not reflected in excess.Employees, but in the unprecedented number of job openings.The number of job vacancies surged in 2020-2021 because of employers' concerns about the epidemic and generous unemployment benefits, but now employment as a share of the labour force has only risen to pre-epidemic levels, not beyond. At present, the situation is very different, with a slowdown in demand, a decline in the epidemic, a return to normal unemployment benefits, a decline in excess savings, and a significant decline in the number of job vacancies and the gap between supply and demand of labour.

Second, supply chain recovery and housing market cooling.In terms of commodities, the shift of consumers from goods to services, the recovery of the supply chain and the rise in inventory levels have brought downward pressure on the prices of core commodities. In terms of services, the asking price of the new lease has fallen sharply after the increase in housing demand led to an increase in related rents. The October CPI report suggests that lagged indicators of housing inflation, including new and renewed rents, are likely to peak, and while housing inflation is likely to rise next spring as lending rates rise, it will slow after that.

Third, based on indicators such as household surveys, economic forecast surveys and inflation protected bonds, long-term inflation expectations are still well anchored.Especially compared to the 1970s. Short-term inflation expectations remain relatively high, mainly reflecting the surge in commodity prices. If commodity prices stabilise, inflation should fall. In short-lived and special periods of the epidemic, inflation may just be rising, not deep-rooted.

Taken together, Goldman Sachs Group expects annual core PCE inflation to fall from 5.1% in September to 2.9% by the end of 2023.While durable goods with limited supply and still high profit margins, such as used cars, are expected to slow overall core inflation by nearly half.

The Fed is likely to remain a hawk for a long time

Since inflation will fall rapidly, does that mean the Fed will be relative to doves next year?

On the contrary, Goldman Sachs Group raised the fed peak by 25 basis points to a 5.25 per cent range of 5 per cent. Goldman Sachs Group pointed out:

As real incomes rise, US financial conditions (FCI) need to be tightened to keep economic growth below potential and to continue to balance the labour market.

Even based on our relatively optimistic inflation forecasts, it may be necessary to raise interest rates by at least as much as the market is now pricing to facilitate adjustment in the labour market.

After the FCI moderated over the past monthWe now expect the Fed to raise interest rates by another 125 basis points, including 50 basis points in December and 25 basis points each in February, March and May.

A cut in interest rates next year is also unlikely:

Due to the flexibility of the labour market, inflation is still rising, exceptUnless the economy goes into recession, we won't see any interest rate cuts in 2023.Until the second quarter of 2024, the Fed is likely to cut interest rates by 25 basis points for the first time.

The "long-term high interest rate" once again illustrates the difference in this cycle, and historically, the first rate cut after the Fed's rate-raising cycle was about six months after the last rate hike.

Euro zone & UK: into a mild recession inflationary pressure persists

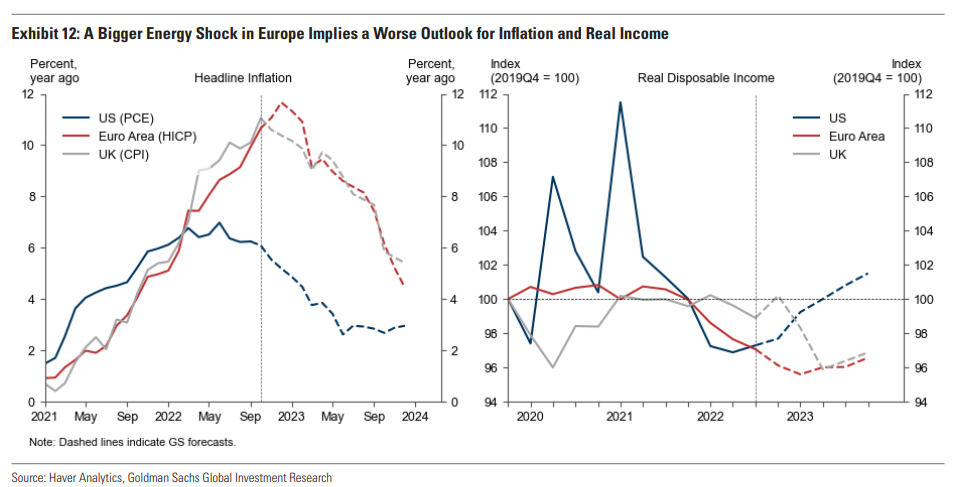

The eurozone and the UK are less fortunate than the US, where thornier energy supply problems could push inflation up to 12 per cent in the eurozone and 11 per cent in the UK.

In turn, high inflation will have a negative impact on real income, consumption and industrial production.Goldman Sachs Group expects real income in the eurozone to fall a further 1.5 per cent in the first quarter of next year and 3 per cent in the UK in the second quarter of next year.

In addition, timely and forward-looking surveys of European countries with gas shortages showProduction in industries such as chemicals and metals has fallen sharply due to rising energy costs.As a result, Goldman Sachs Group expects real GDP to fall 0.7 per cent in the eurozone (2022Q4-2023Q2) and 1.7 per cent in the UK (2022Q3-2023Q2).

1. Natural gas shortage mitigation is expected to avoid a serious recession.

Goldman Sachs Group predicts that there will not be a severe recession in Europe unless it is a cold winter this year and the industrial sector implements stricter energy rationing.

Europe reduced Russia's natural gas imports by 80 per cent and total gas consumption by 20-25 per cent, but did not overwhelm overall activity.So far, most hard economic indicators have remained good, industrial production levels have fallen slightly, real GDP in the eurozone is still rising in the third quarter (slightly lower in the UK) and the labour market remains stable.

The reason for resilience is household energy conservation and other energy alternatives. Along with mild weather, savings have increased natural gas reserves and TTF natural gas prices have fallen by 60 per cent from their peak.

At the same time, Europe continues to benefit from post-epidemic recovery:

First, German chip production and car production have increased, and the bottlenecks caused by the epidemic are easing, roughly offsetting the decline in energy-intensive products.

Second, the household savings rate in Europe has fallen and consumer credit growth has accelerated, supporting consumer spending.

Finally, Europe still benefits from a rebound in services.

While the risk of a recent deep recession has been reduced and the rise in European natural gas prices will be limited next summer, Goldman Sachs Group pointed out that GDP should not be expected to rebound sharply as soon as Europe emerges from a mild recession.Energy prices are likely to remain high until adequate energy supply is ensured or substantial efficiency increases.Goldman Sachs Group raised his growth forecast for the eurozone in 2023 to-0.1 per cent (previously-0.4 per cent).

2. Inflationary pressure may continue or increase interest rate increases.

Core inflationary pressures in the eurozone and the UK have expanded significantly. At present, the UK is facing a perfect storm of "energy crisis" and "overheated labour market". Its core price pressure is the biggest among the G10 countries.

In view of this strong momentum, Goldman Sachs Group expects:

Core inflation in the eurozone will climb further to a peak of 5.3 per cent in December and then gradually fall to just over 3 per cent by the end of 2023; in the UK core inflation is nearing its peak and will fall to 3 per cent by the end of 2023.

Given the reduced risk of a deep recession and persistent inflationary pressures, Goldman Sachs Group expects the eurozone and the UK to raise interest rates more aggressively.

The ECB will raise interest rates by another 150 basis points to a peak deposit rate of 3% (previously expected 2.75%). The Fed will raise interest rates by 50 basis points in December, followed by a second 50 basis point hike in February and a small 25 basis point hike in March and May.

Given the tight labour market and high wage pressures, the Bank of England will raise interest rates by another 150 basis points to a peak of 4.5 per cent.

It is important to note that the ECB's peak interest rate of 3 per cent has two-way risks, with upward risks from persistent core inflation and downside risks from a more severe recession or the outbreak of the Italian sovereign debt crisis.

Central and Eastern Europe & Latin America: economic activity is flexible or avoids deep recession

Since the beginning of this year, some countries in Central and Eastern Europe and Latin America have taken the lead in raising interest rates and began to raise interest rates substantially. The average growth of policy interest rates in nine countries counted by Goldman Sachs Group exceeded 800bp, the GS Financial condition Index (FCI), and the average tightening of 450bp. What is the fate of these economies next year?

Goldman Sachs Group pointed out that the economies of these countries are flexible to a certain extent, and inflation is falling in some areas, especially in Brazil. But central and eastern Europe still faces the risk of rising commodity prices, high inflation and continued monetary tightening.

Although there was no soft landing, the overall economic situation was better than expected. Based on GDP growth, PMI and labour market indicators, most economies are still expanding.

Unemployment is low in almost all economies and the increase in the number of job vacancies reopening and strong private sector balance sheets once again demonstrate the unique characteristics of this cycle.

More encouragingly, core inflation and wage growth in these economies have begun to slow, most notably in Brazil, which is expected to start cutting interest rates in the second quarter of 2023 and return to 2 per cent growth in the second half of the year.

By contrast, Central and Eastern European economies are struggling, still facing the risk of soaring gas prices in Europe, as well as high and widespread inflation, which is still rising in Hungary and Poland. The Czech and Polish central banks are expected to resume raising interest rates soon.

Overall, Goldman Sachs Group pointed out that so farThe resilience of economic activity in Central and Eastern Europe and Latin America means there is unlikely to be a deep recession next year.

Uncertainty remains: can inflation go down? Will the increase in interest rates go too far?

Although Goldman Sachs Group maintains a positive and optimistic attitude, there is still uncertainty as to whether inflation can go down and whether interest rate increases will go too far.

Goldman Sachs Group cautiously mentioned two major risks:

One risk is that inflationary pressures remain so widespread that central banks have no choice but to continue to tighten monetary policy. In this way, a recession is inevitable, including the United States.In an environment of exchange rate depreciation and rising inflation expectations, the ECB and central banks of other emerging economies may be forced to tighten monetary policy further.

Another risk is that underlying inflation does fall, but central banks may be slow to recognise this because they focus too much on lagging inflation indicators such as CPI.Such a risk is unlikely to occur in the US. Fed officials have made it clear that they are focused on more leading indicators, such as newly signed lease rents. In addition, many central banks have either slowed the pace of interest rate increases or hinted that they will do so soon, reducing the risk of excessive tightening.

In addition to core inflation, there are political and geopolitical shocks that could create greater uncertainty and disrupt the global economy by tightening the financial environment or the negative impact of commodity supply.

Goldman Sachs Group believes that there are still many risks for us to return to the turbulent environment of the first half of 2022. So far, the conflict between Russia and Ukraine has persisted, the impact of the Rosneft price ceiling on oil supply is unknown, and political instability in the Middle East may also deal another blow to the energy market, which has a precarious balance of supply and demand.

In short, Goldman Sachs Group's cautiously optimistic global macroeconomic picture remains risky.

Edit / somer