Source: Wall Street

CICC and Shen Wan successively issued articles to discuss the "valuation system with Chinese characteristics", and Citic said bluntly: configure SASAC central enterprises and seize new opportunities.

Overnight, the "valuation system with Chinese characteristics" and central enterprises have become a hot topic. Citic, CICC and Shenwan have issued intensive articles for discussion.

Listed central enterprises with high quality fundamentals but limited investment value will have a good opportunity.

CITIC pointed out that the central enterprises of SASAC play an important role in China's economy, mainly in key industries related to the national economy and the people's livelihood. They are not only the key objects of the current market-oriented reform, but also the vanguard of a series of reforms in our country in the future.Historically, SASAC listed enterprises are more resilient in the bear market, but the valuation flexibility is weak in the bull market.The performance is stable and growing, but the market is reluctant to give a high valuation. To sum up, the fundamentals are good, but the investment value seems to be relatively limited, but we believe that under the background of the current weak market environment and the continuous progress of the reform of state-owned enterprises, listed central enterprises will usher in the allocation opportunity:

The central enterprises of SASAC play an important role in China's economy, which is not only the main object of marketization, but also the vanguard of a series of reforms.

SASAC central enterprises are mainly involved in petroleum and petrochemical, electric power, transportation, iron and steel, coal, communications, military industry, real estate industry chain and other major strategic status entity industries related to international people's livelihood. Since the reform and opening up, the market-oriented reform of central enterprises has been a top priority. In 2020, the state issued a "three-year action plan for the reform of state-owned enterprises", which will continue to guide and help the market-oriented reform of central enterprises. In addition, central enterprises also need to give full play to their social responsibility, assume the function of stabilizing growth in aggregate policy, and be in the vanguard of structural reform, which will benefit in the long run.

Historically, the fundamentals of traditional central enterprises are high quality, but the investment value seems to be relatively limited:

Judging from the market trend, the central enterprises are more resilient in the bear market in history, while the valuation flexibility is weak in the bull market.According to the Guoxin Central Enterprise Composite Index, the rising market of central enterprises in 2020 after the COVID-19 epidemic is limited, but it shows resilience in this year's market. Although the industry distribution of the dismantling index may be the reason for the differentiation of the performance of the central enterprises, even if we examine the sectors, we can find that the leaders of the central enterprises are more resilient in the bear market and the valuation flexibility is weak in the bull market.

From the perspective of driving factors, the performance of central enterprises is stable and growing, but the market is reluctant to give high valuations.The average growth of the overall performance of listed central enterprises in the past 3-5 years is much higher than that of listed companies, while the performance growth of the central enterprises 100 index has outperformed the CSI 300 index in the past year. Although the qualifications and performance of the central enterprises are very high, the market valuation of the central enterprises has always been on the low side.

The future development of SASAC central enterprises will embrace the two main lines of double carbon and innovation.

Carefully screening the high-growth investment main lines within the central enterprises, we think that mainly in the central enterprises under the SASAC which focuses on the real economy, one main line is carbon neutrality, the other is scientific and technological innovation. The dual-carbon transformation will bring business transformation and asset injection, and the valuation of SASAC central enterprises is expected to be reshaped. Under the national system, the state-owned enterprises are expected to focus on scientific and technological innovation, and the high valuation industry is expected to give birth to the leaders of central enterprises.

Looking to the future, the market environment is superimposed with continuous reform, and the central enterprises may meet the continuous market opportunities:

Market environment: central enterprises have good performance and high dividends, and good certainty under uncertainty shows value.Looking at the market so far this year from the perspective of the broad base index, the dividend index has greatly outperformed other indexes since the beginning of the year, and the stocks with high dividends in the bear market have been significantly favored by investors. The dividend yield of central enterprises is high and the valuation is at the lowest level in history, so it has long-term allocation value at present. The good certainty of central companies' performance under downward pressure on economic growth is expected to help them gain a premium.

Continuous reform: the main business reform of state-owned enterprises to improve efficiency, extension investment to expand new areas.In history, it is difficult for central enterprises to get a reasonable valuation. we think the main reasons are that there is still a distance between the marketization of central enterprises and private enterprises, the lack of communication between central enterprises and the capital market, and the industry factors of central enterprises themselves. However, we believe that the above three points are gradually improving. First of all, at the meeting of the political Bureau in July, it was decided that the reform of state-owned enterprises is a long-term reform, in which capital operation is the key. Secondly, driven by double carbon, more than 60% of the listed companies of central enterprises have disclosed ESG special reports. In the future, under the guidance of the three-year action plan for the reform of state-owned enterprises, central enterprises are expected to pay more attention to strengthening communication with investors. Finally, after the transformation of central enterprises from "management" to "management of capital", it is expected that there will be more epitaxial investment to bring about valuation reshaping.

It is an important and realistic problem in China's capital market to explore the establishment of a valuation system with Chinese characteristics and promote the function of market resource allocation to be brought into better play.On the issue of the structure and valuation of listed companies, the speech mentioned the characteristics of the listed company structure of China's capital market with the coexistence of various forms of ownership, covering all industries and the common development of large, small and medium-sized enterprises. it is also pointed out that we should "have a deep understanding of the distinct Chinese elements and development stage characteristics embodied in our market system mechanism, industry industrial structure and main body's sustainable development ability." Deeply study the applicable scenarios of mature market valuation theory, and grasp the valuation logic of different types of listed companies. We believe that from the perspective of the valuation system of the overall market, especially the A-share market, although the degree of internationalization of A-shares has increased in recent years, domestic funds still dominate market pricing, and the valuation of A-shares is more determined by internal fundamental expectations, liquidity and risk premium.

Valuations of state-owned listed enterprises are long-term and generally low.

China International Capital Corporation believes that from a structural point of view, the valuation of A shares is not balanced, especiallyThe valuations of some banks and state-owned listed enterprises are generally on the low side for a long time. The valuation trend of banks and state-owned listed companies has declined in the past decade, and is now at a low level in the historical range.

There is room for improvement in the valuation structure, especially for some banks and state-owned listed enterprises.

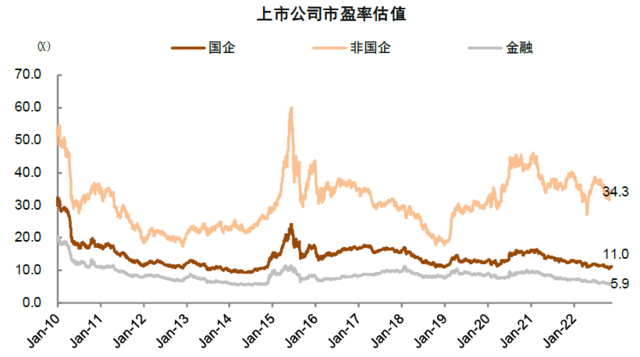

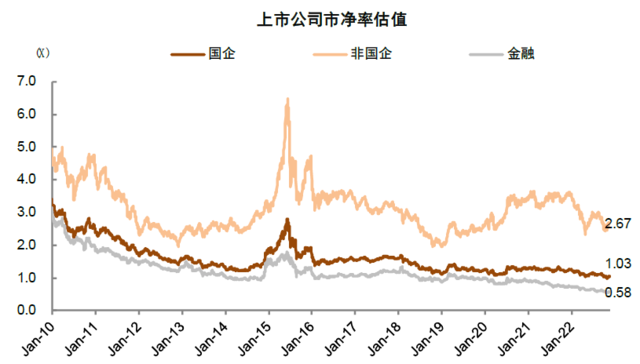

Structurally, the valuation of A-shares is not balanced. The valuation trend of banks and state-owned listed companies has declined in the past decade, and is now at a low level in the historical range, which contrasts with the relatively resilient fundamentals of China's banking industry and state-owned enterprises in recent years. As of November 21, 2022, the TTM valuation of listed state-owned enterprises and non-state-owned enterprises is 11.0 times and 34.3times respectively; among them, the valuation of the financial sector is even lower, with the current price-to-earnings ratio and price-to-book ratio of 5.9 times and 0.58 times respectively, the valuation of price-to-book ratio is already at an all-time low.

The price-to-earnings ratio and price-to-book ratio of listed banks are 4.3 and 0.51 times, and the dividend yield is as high as 6.1%. Compared horizontally with global companies, the valuations of Chinese banks and state-owned listed companies are generally lower than those of overseas comparable companies. The reasons for the low valuations of banks and state-owned listed companies may be various:

1) the marketization of interest rate and other factors affect the market expectation of bank performance, and the performance of banks as a cyclical industry is greatly affected by macroeconomic fluctuations.

2) in the process of the transformation of China's new and old economy, the basic understanding of banking belongs to the traditional field, and the proportion of traditional and old economic industries in listed state-owned enterprises is also high. under this background, the overall performance of new economy of listed companies is better than that of traditional economy in the past ten years. And there are also some differences among investors on the book value of banks and state-owned listed companies.

3) there are some phenomena in the banking industry, such as homogenization, low degree of marketization in operation and management, etc., which are also the main reasons for investors' low pricing on banks at present. In fact, from the operational level, the profit growth and profitability of state-owned listed companies have improved significantly compared with non-state-owned enterprises since 2016, and the debt pressure has been basically resolved after many years of state-owned enterprise reform. The profit growth of listed banks is relatively steady and their ROE is higher than that of non-financial enterprises as a whole. In the future, in the process of active construction of "modern capital market with Chinese characteristics". Investors are expected to gradually improve their understanding of the value of listed state-owned enterprises and the financial sector. On the whole, we think that there is room for improvement in the valuation center of banks and state-owned listed enterprises.

Chart: valuation trend of price-to-earnings ratio of A-share finance and state-owned listed enterprises

Source: Wind, China International Capital Corporation Research Department; Note: data as of November 2022

Chart: since 2016, the profit growth rate of state-owned enterprises has improved and is greater than that of non-state-owned enterprises, and the growth rate of bank performance is relatively stable.

Source: Wind, China International Capital Corporation Research Department

Chart: the profitability of state-owned enterprises has improved since 2016, ROE has gradually exceeded that of non-state-owned enterprises, and the ROE of listed banks has been higher than that of A-shares as a whole for a long time.

Source: Wind, quarterly reports of listed companies, Shanghai Stock Exchange, Fund Association, Insurance Regulatory Commission, Social Security Fund Council, Securities Industry Association, Ministry of Human and Social Affairs, people's Bank of China, Securities Regulatory Commission, China International Capital Corporation Research Department

Chart: compared with the capital markets of overseas major economies, the transaction proportion of individual A-share investors is relatively high.

Source: Wind, Chaoyang Yongshu, China International Capital Corporation Research Department

Shenwan Securities also pointed out in the research report that the value of central enterprises needs to be revalued.

First, promote the reform of state-owned enterprises and accelerate the operation of capital. In history, due to the assessment of asset securitization rate, many state-owned enterprises take listing as the ultimate goal, rather than listing as a smooth financing channel to further expand and become stronger. This makes some state-owned enterprises "lie flat" after listing, lack their awareness as public companies, and fail to communicate with the market, which leads to low valuations or even net valuations, which greatly hinders their ability to further develop through fixed growth, mergers and acquisitions, restructuring and other ways.

Second, make preparations for optimizing the layout of state-owned capital. In different stages of the development of the times, state-owned capital has different missions. Through the increase and reduction of capital market holdings, we can dynamically optimize the layout of state-owned capital in the national economy and play its greatest role. However, the current low valuation limits the potential reduction of state assets in the future. Taking Singapore's Temasek as an example, it was initially positioned as a shareholding platform to promote the reform of state-owned enterprises and enhance their competitiveness. With the vitality of state-owned enterprises and rising share prices, Temasek began to withdraw its capital gradually in 1985. And put state-owned capital into areas and regions with more growth potential. Focus on the central enterprises! For a period in the future, with the maintenance of national security as the main line, scientific and technological innovation is the top priority, the central enterprise group is the best grasp, and the listed central enterprise is the core platform.

Compared with other market players, the advantages of central enterprises are:

(1) personnel shall be appointed by the central government, and operational decisions shall be in line with the will of the state, as referred to by the arm.

(2) it has a market-oriented organization and is the best executor of "catch-up innovation" in the era of great power competition. In the "work Plan for improving the quality of listed companies controlled by Central Enterprises", it is pointed out that listed central enterprises should "be a good national team of scientific and technological innovation" and "focus on obtaining key technologies, core resources and well-known brands, and carry out mergers and restructuring in an orderly manner in accordance with the law." Considering that the non-state-owned science and technology listed companies are bound to enjoy the valuation premium in accordance with the laws of the global capital market in the early growth and technology introduction stage, we believe that the valuation of central enterprises in the current A-share market is very low, with both safety margin and upward flexibility.

The three principles of stock selection of central enterprises: (1) undervaluation and high dividend; (2) active communication with the market and high transparency in enterprise behavior; and (3) in the direction of industry, pay attention to two main lines: large energy category (petroleum, coal, electric power, chemical industry, transportation), large science and technology category (military industry, telecommunications) and so on.

Edit / roy