This week, the United States ushered in the traditional holiday of Thanksgiving, and the Christmas shopping season will begin.

Turkey is on the Thanksgiving table, but Americans may have the most expensive Thanksgiving dinner in history, hit by soaring prices and bird flu.

According to the Bureau of Labor Statistics, the food index increased by 10.9% over last year. According to CPI dataPoultry prices are the highest in the meat category, with Thanksgiving turkey rising 75% to 112%.The price of eggs also soared to $4.18 per dozen, the third highest in history, with eggs at many retailers 200 per cent higher than the normal $1.45 per dozen. Among them, the outbreak of bird flu and supply chain problems are the main factors for the rise in costs.

According to the 37th annual survey of the American Farm Bureau Federation, the average cost of a meal for 10 people this Thanksgiving has risen to $64.05 from an average of $53.31 last year.The increase was about 20%, the highest average cost of a survey in 37 years.

In the context of high inflation, the essential consumer goods industry is favored by the market because it can pass on costs to consumers relatively smoothly and is often defensive in a bear market.

Here are three essential consumer goods stocks that are expected to benefit from rising food prices:

1 、 Performance Food

$Performance Food (PFGC.US)$Is the third largest food service distributor in the United States, with a 9% market share, second only to$Sysco Corp (SYY.US)$ 和$US Foods Holding (USFD.US)$ 。

The company is divided into three divisions: Performance Foodservice, Vistar and PFG Customized, providing (1) all kinds of frozen food, canned and dried food, dairy products, etc.; (2) all kinds of non-food items, such as pizza boxes, disposable napkins, paper products for plates and cups, and all kinds of tableware and kitchen equipment, cleaning supplies, etc. (III) value-added services related to food service distribution, including electronic orders, payment, food safety training, various reports and other data, etc.

PFGC focuses on national chain and independent restaurants (38 per cent of pizzeria), with more than 142distribution centres, more than 200000 products and 125000 customers, enabling it to achieve ideal growth while continuing to trade at discounted prices.

In the post-epidemic era and the current uncertain environment, many competitors are stumbling, while PFGC has a steady income because of its high focus on pizzeria, and a variety of products and services enable it to grow and improve profit margins. Its own-brand products, such as grass-fed beef Braveheart and top seafood Bay Winds, have competitive advantages and differentiation. During the earnings call for the first quarter of 2023, CEO George Holm said:

"We are expected to exceed our initial outlook for fiscal year 2023 and meet the three-year outlook we provided on June Investor Day. Our three-year goal is to achieve revenue of $62 million to $64 billion and adjusted EBITDA of $1.5 billion to $1.7 billion by fiscal year 2025. Our business background is still positive. The slight slowdown in restaurant traffic was offset by the growth of our market share, the continued recovery of the Vistar channel and steady growth in the convenience sector. We pay close attention to the macroeconomic situation and the prospects for 2023. As we emphasize, we feel very good about our position in the market, which is reflected in our revenue and profit performance. "

To achieve growth, PFGC actively made strategic acquisitions, buying Core-Mark, a top wholesale distributor, for $2.5 billion last year, which boosted revenue by 67 per cent to $50.89 billion in fiscal 2022.

Overall, PFGC has a strong financial position and development momentum, the ability to pass on rising food costs to consumers, is a defensive company, its performance may outperform the market.

2. American Food Holdings

$US Foods Holding (USFD.US)$It is the second largest food distributor in the US after Cisco Systems, with a 10 per cent market share in the highly fragmented food service distribution industry.

The company works with approximately 300000 restaurant and food service operators in more than 70 regions and its mission is to provide excellent food solutions and business tools to its partners. In the high inflation, the company relies on the cost advantage to achieve organic growth in market share, and shows a stable return and a huge momentum of growth.

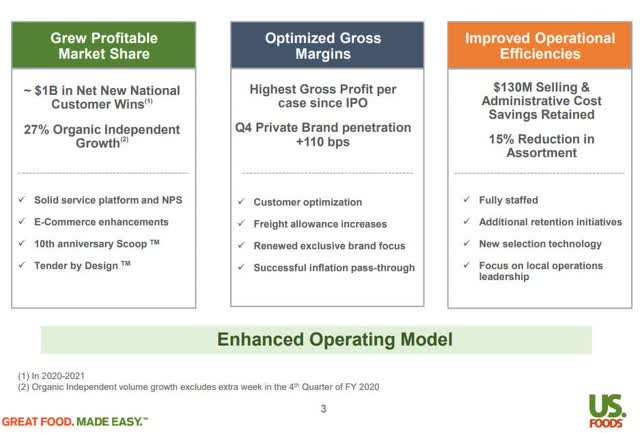

Since the release of results for the fourth quarter of fiscal 2021, management has focused on long-term planning, including:

Restaurant sales are growing 1.5 times faster than the market.

Optimize gross profit margin through pricing adjustment and more private brands

Improve operational efficiency through cost savings

So far, US Food Holdings has been cutting costs and investing in growth, cutting fixed costs by more than $100m and raising $1 billion for new business opportunities. From the perspective of revenue growth and profitability, the company's commitment and focus to serve customers has been translated into continued better-than-expected performance.

Like PFGC, US Food Holdings has a diversified product portfolio and stands out by providing independent restaurant consulting services to improve operations and profitability. In addition, it has its own-brand product line, which improves profit margins and gives it a competitive advantage, which accounts for more than 34% of its sales in 2021.

Revenue in the third quarter of this year was $8.917 billion, up more than 13% from a year earlier. After adjustment, EBITDA increased by nearly 21%. In order to enter the online market and promote market share growth, the company launched its next generation e-commerce digital tool, MOX customers. In view of this year's strong results and cash flow, the company announced a new $500 million share buyback program.

3. United original ecological food

$United Natural Foods (UNFI.US)$Is an organic food distributor providing groceries and general food service products in the United States and Canada. The company is divided into wholesale and retail divisions, as well as a manufacturing department and a brand product line department. The company achieved tremendous growth during and after the outbreak.

Its biggest customer is Amazon.Com Inc's whole Foods supermarket (Whole Foods Market).For more than 20 years, the company has been the main distributor of whole Foods, which was bought by Amazon.Com Inc for $13.7 billion in 2017. Under the revised distribution agreement, the company will continue to act as the principal distributor of whole Foods in all regions of the United States, valid until September 27, 2027. Whole Foods supermarket is also the only customer whose income accounts for more than 10% of the original food revenue.

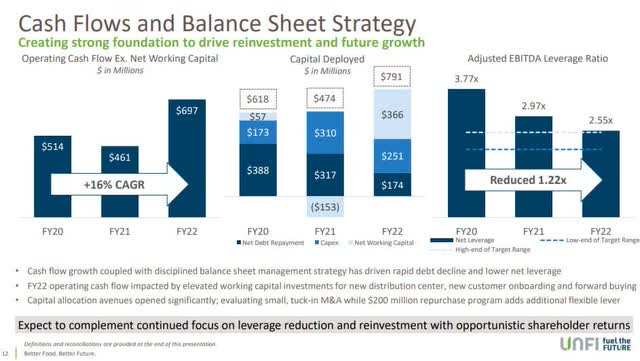

The company has benefited from strong grocery demand and reinvestment for future growth, while focusing on deleveraging and reinvesting for shareholder returns.

All three stocks have outperformed the s & p 500 so far this year, with Performance Food up nearly 27%, u.s. food holdings down about 2.5%, United original food down 4.6%, and the s & p 500 down more than 16%.

Edit / lydia