一周前,全球首家激光雷达上市公司Velodyne宣布与另一激光雷达初创Ouster合并,行业为之震撼。

一周前,全球首家激光雷达上市公司Velodyne宣布与另一激光雷达初创Ouster合并,行业为之震撼。Source: Yuanchuan Automobile Review

Author: Xiong Yuxiang

The cold wind of autopilot blew from Robotaxi to lidar.

A week ago, the industry was shocked when Velodyne, the world's first listed lidar company, announced a merger with another lidar startup, Ouster.

A week ago, the industry was shocked when Velodyne, the world's first listed lidar company, announced a merger with another lidar startup, Ouster.

Ouster, founded by Quanergy, another well-known lidar company, is a start-up trying to subvert the industry with "solid-state" lidar. And Velodyne was once a well-deserved overlord of the industry, and its production of "large flowerpots" (mechanical lidar) is almost a totem of the industry.

But in the cold winter, the landlord's family had no surplus grain. Investors' enthusiasm for autopilot is waning and must work together to reduce costs and increase efficiency, according to the two companies. After the merger, the two companies will have $355 million in cash and a market capitalization of about $400m, after the shares of the two companies have fallen more than 80 per cent. It is said that the actual situation of the merger is that Ouster acquired Velodyne at a low price.

In contrast, although domestic laser companies are still in the stage of losing money, they are living a good life because of financing. Enterprises represented by Suiteng, Wesai and Tudatong have been bound to big customers such as XPeng Inc., ideal, and NIO Inc., and all kinds of technical routes are blooming, and it is not yet known who will win.

So, how did Velodyne, which used to dominate the industry, be reduced to be acquired? Can other companies successfully get to the top by bypassing Velodyne? What is the biggest hidden worry in the lidar industry?

01 the overlord fell

Velodyne is a legend in the lidar industry.

In 2005, David Hall, the American audio tycoon and founder of Velodyne, learned about the self-driving challenge launched by the US Department of Defense, and decided to bow in and develop new sensors for self-driving cars. As soon as he launched, he developed 64-line mechanical lidar HDL-64, which was far better than the widely used single-line lidar with immediate results.

Just two years later, in the new unmanned car challenge, a total of six cars finished the race, five of which were equipped with Velodyne's HDL-64, including the team that won the championship and Asia.[1]。

Velodyne 64-line lidar HDL-64

This race became the beginning of the industrialization of self-driving in the United States and even around the world, and the contestants later became the backbone of the autopilot programs of Alphabet Inc-CL C, Uber, Ford and other companies. Velodyne also came close to the stage and began its 10-year rule over in-car lidar.

Li Yimin, CTO of Tudatong, once said that if it were not for Hall, the development of the global self-driving industry would have been delayed by 10-25 years.

Before 2017, Velodyne basically monopolized the high-performance vehicle lidar. Even though its HDL-64 was quoted at US $80, 000, mainly because the whole mechanical parts needed to be manually adjusted and time-consuming, even so, there was still a price but no market, and the price on the black market once reached about 2 million yuan. In 2016, Baidu, Inc. invested 75 million US dollars in Velodyne just to get the priority to pick up the goods.

During that period, how many new test cars autopilot added each year depended on how many radars Velodyne produced.

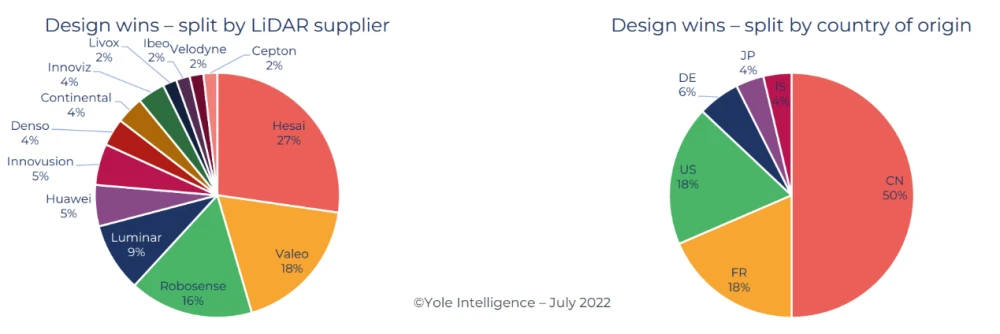

But in the self-driving startup boom that began in 2016, the world was aware of the prospect of lidar, and dozens of startups poured in within a few years. Under the saturated competition, the dynasty of Velodyne declined rapidly. In the competition, the biggest headaches for Velodyne are two Chinese companies: Wesai and Suteng Juchuang.

In 2017, Wesai Technology launched a 40-line lidar, and in the same year, Suiteng created a 16-line lidar for mass production. The two companies competed with Velodyne at the middle and high end and the middle and low end respectively, competing for customers with the cost-effective ratio that Chinese companies are good at.

The following year, the price of Velodyne's 16-line product was cut by 50%. But Wesai and Suiteng continue to expand their share. In 2019, Velodyne launched a patent lawsuit, but Wesai and Suiteng continued to advance by leaps and bounds after paying high patent fees.

In 2020, when Velodyne reluctantly listed SPAC as the first lidar stock in the United States, the best-selling lidar in the world was actually Wesai.

Many customers such as Baidu, Inc. and Wenyuan know that they defected from Velodyne, not only because of the price, but also because of faster product updates and after-sales service.

Compared with Wesai, Velodyne has only a sales department in China, and its service and support capacity is weak. Wen Yuan Zhixing COO tension once complained.Velodyne's lidar repair will be sent overseas, and the whole process will take 1-2 months.[2]Domestic companies can provide 7x24-like babysitting service, or even 7-day refund and exchange[6]。

The change of technology has made Velodyne's situation even worse.

After 2020, the accelerated popularity of intelligent driving in passenger cars has given rise to the demand for specification-level lidar, a much larger blue ocean market. However, there are hundreds of internal parts of the traditional mechanical lidar, and there are a large number of moving parts, so the reliability can not meet the vehicle regulations, and the solid-state / semi-solid lidar can reduce the moving parts.

In fact, Velodyne has long seen the trend, releasing a solid-state lidar prototype in 2017 and a "mass production version" in 2020. However, Velodyne has no solid-state lidar manufacturing experience, the company's management infighting after the listing, founder Hall was also exposed for neglect of management[3]To this day, Velodyne's solid-state lidar has not boarded the production car.

Velodyne accounts for only 2% of the fixed-point orders for solid-state lidar.

Velodyne's failure to convert to solid-state lidar led directly to Hall's ouster from the board of directors last year and a change of management. At the same time, Velodyne's few customers in the automotive industry are still "Buddhist", and their lidar boarding schedules are mostly in 2023 or later, which is not as radical as domestic car companies.

After going public, Velodyne fell into persistent losses. Under the multiple negative conditions, Velodyne has no choice but to stay warm with each passing day.

What happened to Velodyne is really just a microcosm. The share price of the US-listed lidar company has fallen by more than 80 per cent since last year. Not only was Velodyne forced to merge with Ouster, but another Quanergy plunged 99 per cent and was expelled from Nasdaq.

While the performance of the east coast of the Pacific has plummeted, mass production on the west coast of the Pacific has steadily improved.

Fortunately, the seed customers of Chinese lidar manufacturers are the new car-building forces of natural rolls.

Under Wei Xiaoli's fanatical intelligent driving competition, since 2021, solid-state / semi-solid lidar of Suiteng, Tudatong and Wesai have successively boarded the mass-produced models of XPeng Inc., ideal and NIO Inc.. In these three pairs of cooperation, the new forces are deeply involved in the product definition of lidar. Among them, NIO Inc. personally designed the circuit board of the Tudatong Falcon.

Velodyne actually lost to a community with a shared future full of crisis and combat effectiveness on the other side of the ocean.

But the industry is far from winning or losing. If the commercialization of in-car lidar is a 100-kilometer weight-bearing off-road marathon, those who run first have just passed the first checkpoint.

02 no one on the throne

What happened to Velodyne is a cruel fact: although it entered the industry nearly a decade before many companies, there was no moat.

The reasons are regulatory, commercial and even political, of course, but it boils down to technology: in the past few years, the main market for in-vehicle lidars has moved from Robotaxi to passenger cars, moving from mechanical rotation to solid / semi-solid. Velodyne, which started with mechanical lidar, failed to complete this difficult technology and product reconstruction successfully.

But the challengers who ousted Velodyne from his throne are also treading on thin ice. Because the technical routes of the whole industry are diverse, and the rapid development and switching, the technological gamble of trying to build barriers is likely to become a Soha that loses all its underwear.

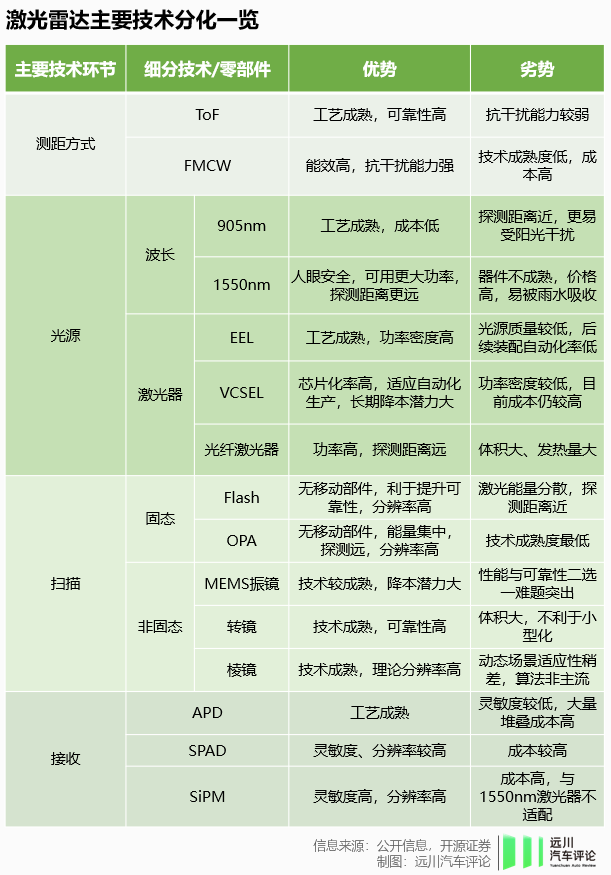

This uncertainty is embodied in that almost every one of the key technologies of lidar, from ranging mode to laser transmitting, scanning and receiving module, does not converge to an optimal solution, but has its own advantages and disadvantages for du (bo).

As a result, there is a scene of letting a hundred flowers blossom in the industry: there are dozens of companies in the industry, and almost every company comes up with a different solution through the arrangement and combination of technology.

A typical example is the lidar "three domestic heroes" Wesai, Suiteng, Tudatong's first passenger car, lidar AT128, M1, Falcon, although the front and rear feet get on the car.But the technical repetition rate is very low.

Among them, Suiteng M1 tends to use more mature parts, which has been iterated many times to improve the integration of components, and has low theoretical cost, so it is suitable to play the role of price butcher.

Hesai AT128 has enabled the new VCSEL array on the light source to pursue the semiconducting of parts and minimize the number of moving parts, which is conducive to product reliability.

The Tudatong Falcon focuses on miracles, with larger size, power (and more expensive parts) in exchange for higher performance, farther vision and higher resolution.

Until dozens or even millions of lidars are delivered for verification, no one knows which solution will win, or that the three will be divided into three levels of the market. or other companies sweep them into the old paper with breakthrough technology-the hot lidar recruits a large number of talents from optics, optical communications and semiconductors, which is not an industry that lacks new technologies.

For lidar enterprises, a more accurate answer is to land more intelligent electric vehicles at a low enough cost as soon as possible, and to ensure the reliability of this precision optical equipment in a complex vehicle environment. Make your plan a de facto industry standard as much as possible.

Therefore, the lidar enterprises in the forefront focus on two key words: engineering and manufacturing.

Li Yifan, CEO of Hesai Technology, said in an interview with Nine chapters Zhijia that CTO, who is in charge of engineering, is in charge of thousands of people to Shaoqing, while he and the chief scientist are in charge of more than 100 people each. Last May, Hosai Investment began to build its own "Maxwell" lidar super factory.

Similarly, Suiteng Juchuang last week formed a joint venture with Lixun Precision Manufacturing company Liteng Innovation, which is trying to take the lead in bringing the endless technology competition back to the mass production competition of precision manufacturing.

Even so, lidar is still a costly business in the short term. The Wesai Maxwell super factory has an investment of 200 million US dollars and plans to produce one million units a year. On September 29 this year, Wo Sai announced that the monthly delivery of the car's lidar had just exceeded 10,000-the fastest head player.

Two days later, Tesla, Inc. 's annual AI Day was held, and Musk passed the cold to every lidar company.

03 the greatest enemy is not a colleague

It is easy to overlook the fact that the biggest enemy of lidar companies is not competitors in the same industry, but cameras, or, more accurately, those that develop pure visual autopilot. Tesla, Inc. is the person in charge of this camp.

In the past few years, Musk has repeatedly regarded the Diss lidar as an autopilot "crutch" and anyone who relies on lidar will fail.But for a long time, most practitioners' attitude towards lidar is "you spray yours, I use mine".This is because pure visual autopilot without lidar is highly dependent on deep learning and once had major deficiencies in environmental perception:

On the one hand, the camera itself is not an all-weather sensor, and it is difficult to work properly on rainy and snowy days and at night; on the other hand, in the previous vision algorithm framework, objects captured by the camera must be recognized before they can be considered by the system to exist. This leads to the extremely unstable performance of pure visual autopilot in dealing with untrained obstacles and stationary objects, and often fails to detect and misdetect.

The lidar can detect obstacles through accurate ranging without training, which provides a guarantee for autopilot.

Therefore, the mainstream view of the intelligent driving industry was that a multi-sensor fusion sensing system should be built to make the camera and lidar complement each other. However, the hardware advantage of lidar is gradually flattened by Tesla, Inc. 's advantage through software algorithm.

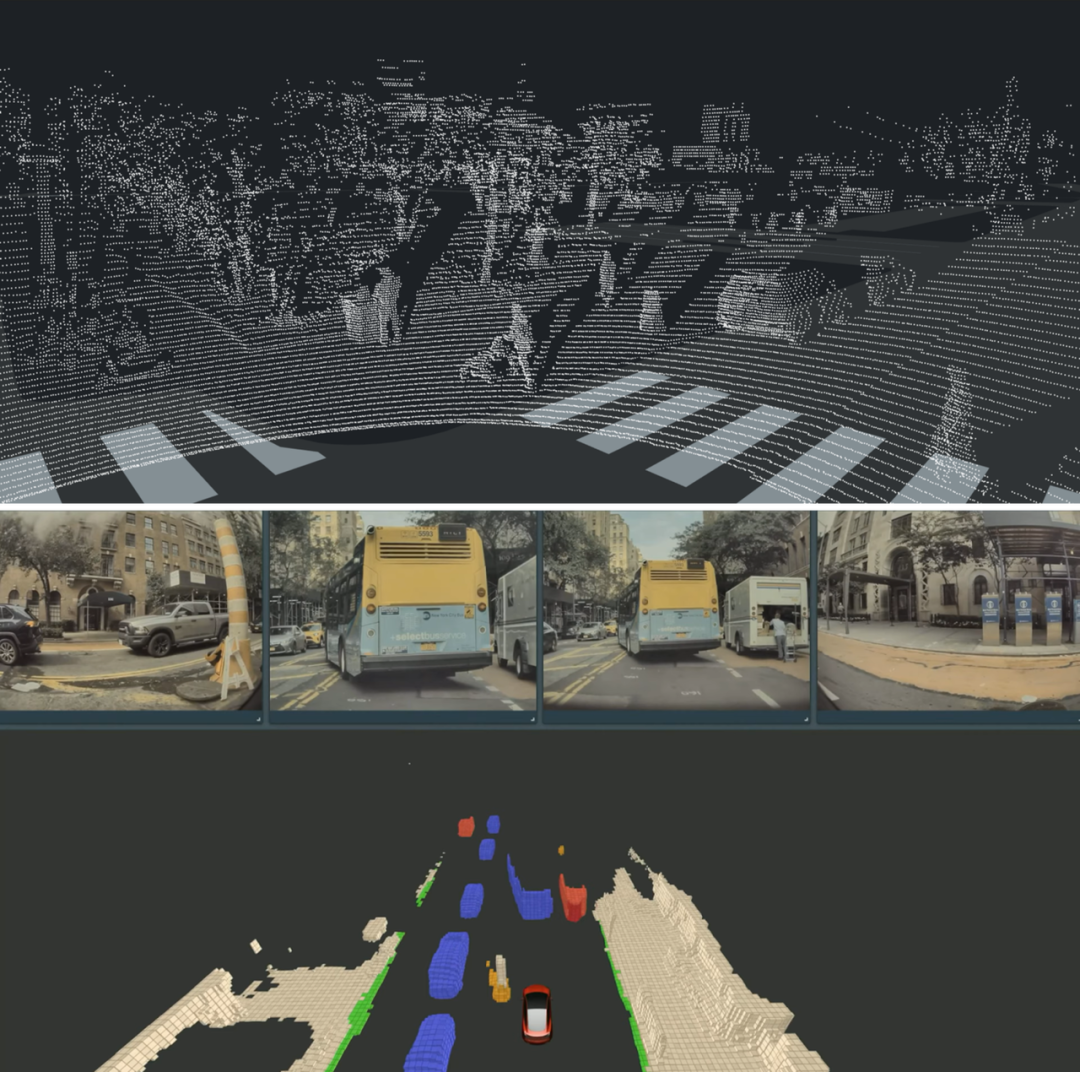

On this year's AI Day, Tesla, Inc. introduced occupation Network (Occuppancy Network) in detail. This algorithm can restore the three-dimensional world with high precision and high real-time based on two-dimensional images. It can not only sense the volume of objects, but also distinguish their dynamic and static states. This is essentially no different from the ability of lidar.

The above picture shows lidar perception, and the following picture shows the occupation of network perception.

If the camera can become a substitute for lidar, the living space of the latter will be in jeopardy.

Ideally this year, we will vigorously increase the size of intelligent driving based on visual perception. And after occupying the network to open up, the ideal is to take the lead in increasing the ambition of others--CEO Li wants to say on Weibo Corp that the essence of lidar is to occupy the network.It is said that Wu Xinzhou, the person in charge of XPeng Inc. 's intelligent driving, also privately told lidar manufacturers to prepare for the transformation.

However, the industry is not all Tesla, Inc. 's followers. By the middle of this year, Suiteng Juchuang had won more than 40 lidar model locations, and Wesai also claimed that there were millions of pre-installation locations from the mainframe factory. More car companies are waiting to see: whether the lidar is used or not depends on whether it is cheap enough, and the sex can be unstable.

Prior to this, the price of car-grade lidar has been reduced from 10,000 yuan to more than 3000 yuan, but compared with a few hundred yuan a high-definition camera, the price of lidar still puts an embarrassing burden on most models. To reduce the price by another order of magnitude is not only the ardent hope of the lidar, but also a prerequisite for large-scale loading.

A secret battle between cameras and lidar to steal from each other has actually begun.

The strategic goal of lidar is to reduce costs. According to Li Yifan's vision, the final price of lidar will be 2-3 times that of the camera.[4]The strategic goal of the camera is to improve the efficiency, make the visual algorithm more accurate and confident, and approach the lidar as much as possible.

At present, the sound of the coexistence of the two is still the mainstream, but in this race, the lidar, as a new sensor, is facing greater hidden worries.In history, the primary factor that determines the rise and fall of a new technology is often not the advanced nature of its theoretical performance, but the ability to use existing technologies and facilities.

Compared with lidar, the ecology of the camera is perfect and huge.

Image-based computer vision has always been a prominent study of AI, with the largest number of sensors (cameras), the largest amount of data and the most intensive talent. This advantage has been directly inherited in the field of intelligent driving. At present, most intelligent driving functions are accomplished by cameras + visual algorithms, or at least mainly by cameras. This brings a complete closed loop of data, as well as the extremely high speed of evolution of visual algorithms.

In comparison, the ecological construction of lidar is still in its infancy, with fewer data and talents, and more immature algorithms. Even, because people are familiar with images rather than point clouds, lidar data labeling is less efficient and more expensive than images: an image usually takes tens of seconds and costs a few cents, while the typical labeling cost of a lidar point cloud is from a few minutes to ten yuan.[5]。

The roots of these differences may be traced back to the formation of civilizations and even the evolution of eyes by ancient human ancestors.

Andrej, Tesla, Inc. 's former director of AI, recently said in a podcast that the artificial world created by human beings is built from the point of view of being easy for the human eye to perceive, so visual sensors will naturally be at the core.Tesla, Inc., who has figured this out, is breaking through the ceiling of visual smart driving every year. Not long ago, Tesla, Inc. began to push FSD V11 in North America.

This means that lidar will fight an unequal war. In the face of rapidly evolving rivals, lidar needs to run faster, cooperate more closely with the downstream, and break through the impossible triangle of "cost, performance and stability" as soon as possible if it is to win a place in autopilot.

Reference:

[1]It Began With a Race... 16 Years of Velodyne LiDAR,Velodyne

[2]Misjudgment, counterattack, car overturning, lidar ten years on the road, later LatePost

[3]LIDAR maker Velodyne boots its founder after an investigation into 'inappropriate' behavior,The Verge

[4]A Lidar head player's thinking from 1 to 10-- Nine chapters Zhijia Dialogue CEO Li Yifan, Nine chapters Zhizhi

[5]After burning hundreds of billions of dollars in ten years, the unmanned car still has no way to go. I will LatePost later.

[6]Eighteen years of Lidar fighting: the Twilight of the Gods in the West, the New King in the East, HiEV garlic car Research Institute

Edit / Corrine