Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Beken Corporation (SHSE:603068) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Beken

What Is Beken's Net Debt?

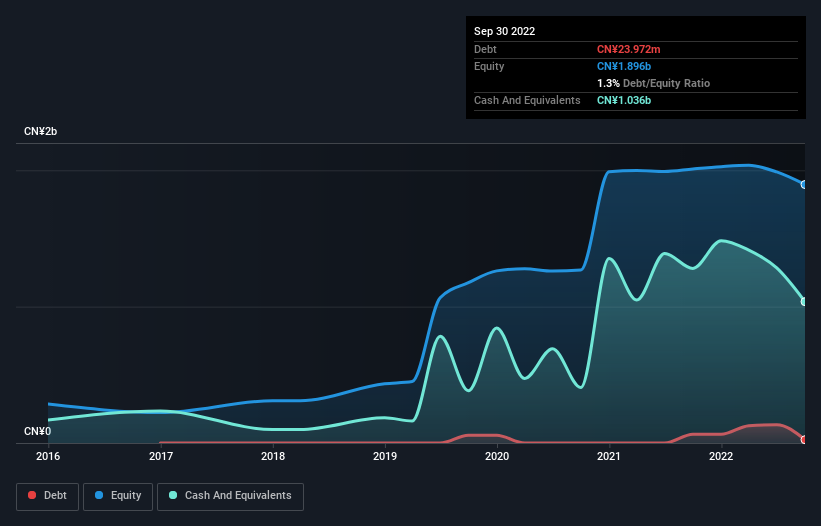

As you can see below, Beken had CN¥24.0m of debt at September 2022, down from CN¥64.9m a year prior. However, it does have CN¥1.04b in cash offsetting this, leading to net cash of CN¥1.01b.

SHSE:603068 Debt to Equity History November 17th 2022

SHSE:603068 Debt to Equity History November 17th 2022A Look At Beken's Liabilities

Zooming in on the latest balance sheet data, we can see that Beken had liabilities of CN¥247.0m due within 12 months and liabilities of CN¥13.5m due beyond that. Offsetting these obligations, it had cash of CN¥1.04b as well as receivables valued at CN¥123.6m due within 12 months. So it can boast CN¥899.6m more liquid assets than total liabilities.

It's good to see that Beken has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Due to its strong net asset position, it is not likely to face issues with its lenders. Succinctly put, Beken boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is Beken's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Beken made a loss at the EBIT level, and saw its revenue drop to CN¥819m, which is a fall of 22%. To be frank that doesn't bode well.

So How Risky Is Beken?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year Beken had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of CN¥264m and booked a CN¥112m accounting loss. With only CN¥1.01b on the balance sheet, it would appear that its going to need to raise capital again soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Beken you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.