In this year's aggressive global "austerity race", Japan can be counted as an "out of place" exception, leading to a series of anomalies, such as the sharp devaluation of the yen, the lack of trading of Japanese bonds for days and the surge in the trade deficit. All kinds of "chaos", especially the distorted relationship between exchange rate intervention and monetary easing, as well as persistent record trade deficits, seem to point to a state that is difficult to stabilize. It is worth thinking about how long this situation can last and whether it will produce a "butterfly effect" and a chain reaction.

First, the "fragile" balance: the devaluation of the yen vs. Monetary easing "fighting between the left and the right"

The depreciation of the yen has led to a substantial increase in the trade deficit, which has not only failed to boost exports in the context of falling overseas demand and high oil prices, but has created some economic pressure. In order to boost the economy, monetary policy is loose, which further increases the downward pressure on the exchange rate. If the economy does not boost for a long time, it may form a negative cycle. Loose currency + foreign exchange intervention is the lesser of the two evils, but it is quite unstable.

Second, the meaning to the world: the possible "ripple" effect under the transmission of funds; pay attention to the changes of foreign exchange operation and monetary policy

For the world, the significance of changes in the yen and Japanese bonds is mainly to bring about a chain reaction through the supply of "cheap money".Exchange rate intervention may cause interest rate volatility by selling Japanese foreign currency holdings, while monetary policy may have a greater impact if there are marginal changes, such as asset volatility caused by a reversal of the carry trade or short-term liquidity shocks caused by the unwinding of short positions in the yen. In the benchmark case, the probability of policy change is small, but we need to pay attention to the end of the president's term and foreign exchange pressure.

Third, historical review: what happened to the sharp devaluation of the yen before?

1997 compared with 2012, the current objective environment of the active devaluation led in 2012 is more similar to the devaluation cycle that began in 1995, but Japanese banks are more cautious in lending than before the Asian financial crisis, and their exposure is not completely similar. Looking back, core indicators such as currency swaps that measure global dollar liquidity and the Bank of Japan's monetary policy are noteworthy.

The yen depreciates sharply, the Bank of Japan is "firmly" loose, and Japan's trade deficit is a record; will Japan become a possible "black swan"?

In this year's global aggressive "austerity race", Japan can be regarded as an "out of place" exception. The Bank of Japan's insistence on easing and 0.25% YCC (yield curve control) has led to a series of seemingly "abnormal" phenomena.:

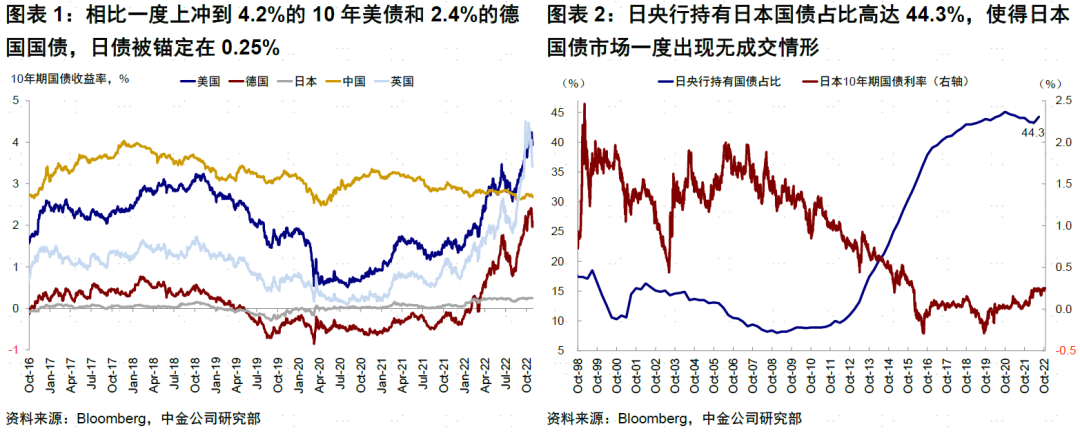

1)Compared with 4.2% of 10-year Treasuries and 2.4% of German bunds, JGBs were anchored at 0.25%, and the Bank of Japan held 44.3% of JGBs, which once led to no turnover in the JGBs market.

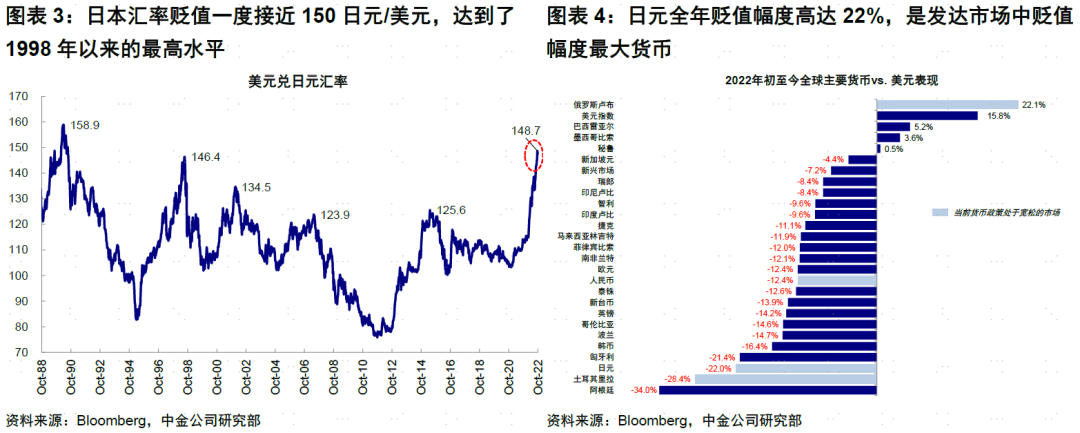

2)At one point, the exchange rate of the yen exceeded 150 yen per dollar, the lowest since 1998, with a depreciation of 22% this year, which not only exceeded the devaluation of sterling, which was the lowest since the 1980s, but even exceeded the exchange rates of most emerging markets. this forced the Ministry of Finance and the Central Bank of Japan to intervene in the exchange rate for the first time since the financial crisis in 1997, albeit with little success.

3)Japan's trade deficit soared, with the monthly trade deficit (goods and services, BOP calibre) hitting a new high of 2.9 trillion yen in August, adding to the depreciation pressure on the yen.

All these "chaos", especially the distorted "left-right" relationship between exchange rate intervention and monetary easing, and the persistent record trade deficit, seem to point to a state that is difficult to stabilize.So how long this situation can last and what kind of "butterfly effect" and knock-on effect some changes will have on global financial markets are worthy of our consideration in the current situation of global market turmoil.

Compared with other emerging markets, Japan's importance to global markets lies in its knock-on effect through liquidity.In the current situation of global radical austerity and the intensification of offshore "dollar shortage" ("grey rhinoceros under the disappearance of" cheap money "," dollar shortage "and global" panic "), Japan, as one of the last positions of global" cheap money ", its possible changes and the breaking of the fragile balance. It is likely to have a big impact (the current global level of negative interest-rate debt has fallen from a high of $18 trillion during the outbreak to $1.8 trillion, all of which are Japanese bonds). Therefore, in this paper, we will analyze the causes of the current situation in Japan and the possible impact on the future.

First, Japan in a "fragile" balance: the devaluation of the yen vs. The "left-right struggle" of monetary easing

The depreciation of the yen has led to a sharp increase in the trade deficit.In the context of the current high oil prices, the sharp depreciation of the yen has not had the effect of boosting Japan's net exports. on the contrary, the deficit continues to widen due to the sharp rise in the import price of the local currency. Japan has been running a trade deficit for 15 consecutive months since June 2021, reaching a record 2.9 trillion yen in August this year. The surging trade deficit has also become a factor exacerbating the downward pressure on the yen. In this context, corporate profits have also been suppressed to a certain extent. EPS growth in the Nikkei 225 index in the first and second quarters was-79.2 per cent and-81.0 per cent respectively; net profit margins fell to 2.7 per cent and 1.3 per cent respectively (an average of 8.8 per cent in 2021); and in 2023 it is unanimously expected that EPS will be adjusted from the first half of this year and the current growth rate has been lowered to 5.7 per cent.

Economic weakness restricts the shift in monetary policy.If the Bank of Japan does not strictly adhere to the control of the 0.25% yield curve against the backdrop of aggressive interest rate increases by the Federal Reserve, it may ease some of the depreciation pressure, but the current overall weak growth situation makes the Bank of Japan firmly maintain its loose posture. (at the interest rate meeting that just ended in October, the Bank of Japan maintained negative interest rate policy and YCC, and maintained dovish guidance.[1]). Although the depreciation of the exchange rate has had a certain boost effect on external demand, the decline in import demand in the US and Europe has also weakened Japan's export outlook. The sub-entry of new export orders in the PMI has been below the 50% rise and fall line for eight consecutive months and is still 47.4% in October. The new orders index has also fallen below 50% in April. At the domestic consumer level, Japan's consumer confidence index fell from around 39 at the end of 2021 to 31 in September, and continued to fluctuate.

It is not difficult to see that the Bank of Japan and the Ministry of Finance choose to stimulate the economy through easing and suspend the momentum of excessive exchange rate depreciation through foreign exchange market intervention, which is the lesser of the two evils in austerity and devaluation.. But this path can be done only if the economy is effectively boosted and inflation remains relatively moderate (the Bank of Japan raised its inflation expectations to 2.9 per cent in fiscal year 2022 from 2.3 per cent.[2])。

Otherwise, the weak economy > policy easing > exchange rate depreciation pressure > > economic downward pressure may gradually evolve into a negative cycle.There is a risk that foreign reserves will be consumed too fast to upset the current balance unless we "passively wait" for the Fed to slow the pace of tightening. Therefore, Japan, which is in a fragile balance, has a relatively large economy and a relatively large capital market, and this instability undoubtedly requires attention.

Second, the meaning to the global market: the possible "ripple" effect under the capital side transmission; pay attention to the change of foreign exchange operation and monetary policy

For the world, the significance of the changes in the yen and Japanese bonds is mainly to bring about a chain reaction through the supply of "cheap money".. Risk aversion or a rapid rise in the financing cost of Japanese bonds could trigger part of the cost based on the depreciation of the yen and the low-interest financing of Japanese bonds investors sell their holdings and return the yen for the purpose of reducing their positions (the so-called carry trade reversal, carry trade), which in turn increases the demand for the yen, resulting in a de facto appreciation of the yen, which is one of the reasons why the yen is often seen as a safe haven exchange rate. If this transaction forms a trend and self-reinforcing realization, even do not rule out a larger market disturbance. The recent continuous intervention of the Japanese Ministry of Finance in the exchange rate of the yen, or obtaining funds by selling US bonds, may also be one of the factors contributing to the recent rise in US bond interest rates.

For Japan's interior,If the persistently low interest rate environment is reversed, whether there will be a chain reaction similar to that of previous British pensions is also the focus of the market ("grey rhinos with the disappearance of" cheap money "). Japan's policy uncertainty index rose again to 140 in September, reaching highs of previous policy fluctuations (such as the COVID-19 epidemic in 2020 and the first implementation of negative interest rates in early 2016). In addition, the policy path of the current central bank governor Kuroda when his term expires in April next year is also uncertain.In the short term, we expect Japan to still respond with a combination of monetary easing and foreign exchange intervention, but we need to pay attention to marginal changes.

►The impact of exchange rate intervention policy is mainly caused by interest rate fluctuations through the selling of foreign exchange.Japan's Ministry of Finance publicly announced in September that it had conducted a foreign exchange intervention and bought 2.8 trillion yen, which was the first large-scale yen-buying intervention since the Asian financial crisis in 1997-1998. The range was also close to the peak of the intervention at that time (2.8 trillion yen was also purchased in April 1998), which partially alleviated the pressure on the depreciation of the yen. Although the foreign exchange intervention quota data for this month have not been disclosed, combined with the judgment of CICC's foreign exchange group ("Japanese foreign exchange intervention # 2:" invisible "foreign exchange intervention"), the high probability of exchange rate changes between the United States and Japan on October 21 also comes from foreign exchange intervention. High-frequency outbound investment data under Japan's BOP caliber show that net sales of medium-and long-term bonds reached 1.4 trillion yen in the week of October 22, possibly due to Japan's realization of foreign currency assets and yen purchases, while as of 2021, 47 per cent of Japanese BOP medium-and long-term bond investments were US bonds. Looking back, if the yen continues to depreciate at a faster rate, the Ministry of Finance may choose to intervene in the exchange rate again. The vast majority of Japan's official foreign exchange reserve assets are securities assets, and Japan is the largest overseas holder of US Treasuries (16.0 per cent of foreign investor holdings and about 5 per cent of the US debt market).

Further foreign exchange intervention may not rule out the possibility that it will put some short-term upward pressure on US bond interest rates.. Moreover, the current seemingly high spreads between the United States and Japan will hit a multi-year low if the higher cost of foreign exchange hedging is deducted, so the momentum for Japanese investors to buy large amounts of US bonds may not be very strong.

If there is a marginal change in monetary policy, the impact may be greater, but the probability may be low in the benchmark case.The current foreign exchange intervention of Japan and the continuous YCC policy of the Bank of Japan restrict and even contradict each other.In theory, if the YCC is adjusted or the Fed slows down the rate of raising interest rates, it is possible to solve the current problem of exchange rate depreciation more effectively.But before the Fed policy can retreat or the Bank of Japan is unwilling to adjust monetary policy, the current foreign exchange intervention is more of a temporary cure than a permanent cure. If it lasts longer, it will make the market worry that foreign reserves will be consumed too quickly.

In addition, under imported inflation, Japan's CPI exceeded 3% year-on-year in August, still as high as 2.9% in September, and exceeded the Bank of Japan's target level of 2% for six consecutive months, and CPI excluding food and energy also reached 1.9% in September. The central bank meeting in October further raised its inflation forecast for fiscal years 2023 and 2024 to 1.6%.[3]. The Bank of Japan expects inflation to fall below 2% in 2023, so it remains loose.But there is also a need to watch the end of the term as central bank governor next year and the risk of a change in foreign exchange pressure, especially when Fed policy is pushed back.The potential impact is mainly reflected in two aspects:

One is the asset volatility caused by the reversal of the carry trade (carry trade).At present, the pricing of Japanese treasury bonds is distorted due to the YCC policy. If the YCC is adjusted upward, it cannot be ruled out that due to the shaking of confidence in the long-term loose policy, the interest rate of treasury bonds will rise sharply in the short term (or even exceed the level controlled by YCC), thus exerting certain pressure on the carry trade position. We approximately equate the size of foreign bank lending in Japan to the size of the carry trade, with the current position of 11 trillion yen, which is significantly smaller than before the financial crisis (more than 20 trillion yen in 2007), but also higher than the previous cycle of yen depreciation. If this position is forced to close, the ability to export low-interest liquidity from Japan to overseas will be curbed.

Second, the current high-scale yen short positions forced to close may trigger short-term shocks.The current CFTC yen speculative net short position is about 100000, the 92.8 per cent quantile since 2000. If the Bank of Japan monetary policy changes, the yen is at risk of appreciation, while higher short positions will amplify fluctuations and, in extreme cases, may trigger short-term liquidity shocks.

Third, historical review: what happened to the sharp devaluation of the yen before? 1997 and 2012

The depreciation of the yen so far this year can only be compared with the Asian financial crisis (45 per cent from April 1995 to August 1998) and Abenomics (38 per cent from 2012 to 2015). So, we briefly review what happened and the impact of the previous two rounds of devaluation are as follows:

1995-1998: monetary policy differentiation between the United States and Japan and the Asian financial crisis.The devaluation of the Japanese yen for three years from 1995 to 1998 can be divided into two stages.The devaluation of the Japanese yen in the first stage is mainly affected by the reverse monetary policy of the United States and Japan.The Fed began its rate-raising cycle in February 1994, raising interest rates by 300bp (the federal funds rate ranges from 3 to 6 per cent) within one year. Although it briefly cut interest rates three times in 1995, it raised interest rates again to 5.5 per cent in 1997 to prevent subsequent inflationary pressures caused by economic overheating. By contrast, the Bank of Japan has been in a cycle of interest rate cuts during the same period, with the yen depreciating from a high of 81 in 1995 to 127 in April 1997, by 36%.The devaluation of the Japanese yen in the second stage was mainly affected by the Asian financial crisis.The Asian financial crisis that broke out in 1997 made the Japanese economy even worse, and the Japanese government also tried to stimulate its economy with the help of the depreciation of the yen. However, the fiscal tightening implemented at the beginning of the year and the impact of exchange rate depreciation in some Southeast Asian countries on Japan's financial system and exports in 1998 all increased the downward pressure on the economy. as a result, the dollar against the yen fell from 113 in June 1997 to a low of 146 in August 1998, a depreciation of 23%.

The sharp depreciation of the yen has further increased the pressure on capital outflows from some Asian markets.Since the Bank of Japan holds about 1/3 of the debt of Asian markets affected by the financial crisis, most of it is denominated in dollars.The sharp depreciation of the yen is equivalent to a disguised increase in debt exposure in yen terms.Since Japan continued to suffer from internal bad debt problems from 1997 to 1998, it triggered the pressure of withdrawing loans from Southeast Asian countries, which in turn aggravated the capital outflows of these countries and worsened the Asian financial crisis.[4]. Although the Japanese government took a large-scale intervention of 2.8 trillion yen in April 1998, it did not immediately stop the decline of the yen until the default of Russian government bonds and the outbreak of the LTCM incident forced risk aversion to rise in August of the same year, and the yen bottomed out.

2012-2015: three arrows of "Abenomics" lead the yen to depreciate sharply. After taking office at the end of 2012, former Japanese Prime Minister Shinzo Abe launched a series of policies, namely Abenomics, mainly including active financial policy (large-scale quantitative easing), flexible fiscal policy (expanding government fiscal expenditure), and the "three arrows" (three arrows) of building a reformed economic policy (promoting and developing private investment), in an attempt to improve the international competitiveness of Japanese goods through the depreciation of the yen. The yen fell 38% against the dollar from 78 in September 2016 to 125 in June 2015. Although the Fed began its interest rate hike cycle again in December 2015, financial market turmoil triggered by Brexit and risk aversion helped the yen to appreciate in 2016.

On the whole, the current devaluation is not the same as that in 2012, and the objective environment is similar to that in 1995, but Japanese banks are more cautious in lending than during the Asian financial crisis. therefore, it is not entirely similar to the Asian financial crisis in terms of risk exposure. Looking back, Japan's potential policy changes are noteworthy, with core observation indicators such as global dollar liquidity currency swaps and the Bank of Japan's monetary policy.

Market dynamics: doves are expected to push interest rates down and US stocks rebound; the ECB raises interest rates as scheduled, while the Bank of Japan keeps YCC; interest rates lower, US stocks rebound, and growth leads

Asset performance: stocks > debt > bulk; interest rates fall, US stocks rebound, growth lags behind

After the RBA rate increase slowed to 25bp on Oct. 4, Canada's rate rise unexpectedly slowed to 50bp this week, lower than expected 75bp, and the market is associated with whether the Fed is also slowing down. However, PCE data released near the weekend show that core inflation is still accelerating, supporting the Fed's current path of raising interest rates, with a high probability of raising interest rates by 75bp in November, while the extent of the rate increase in December may depend more on subsequent inflation and non-farm conditions. In terms of asset performance, doves expect to push US debt interest rates down, and 3m10s spreads were once upside down in intraday trading; although overall US stocks rebounded, the growth style represented by FAAMNG fell significantly, with lower-than-expected performance as the main reason: Meta earnings were lower than expected across the board, income accelerated year-on-year decline, and net profit fell sharply; Microsoft Corp's net profit fell by 13%, the biggest drop in two years. Alphabet Inc-CL C due to a sharp drop in advertising revenue growth, revenue and profits are lower than expected.

In Europe, the new British Prime Minister Sunak takes office.[5]Interest rates on gilts fell back to levels before the tax cuts were announced. As for other major central banks, the ECB announced this week that it would raise interest rates by 75bp, while saying that QT's decision would be announced again at its December meeting.[6]The Bank of Japan keeps its YCC policy unchanged.

Liquidity: further tightening of onshore dollar liquidity

►Liquidity: further tightening of onshore dollar liquidity

Over the past week, FRA-OIS spreads continued to widen to 45.6bp, while credit spreads on investment grade and high-yield bonds narrowed slightly. 90-day spreads in the financial sector narrowed, while non-financial spreads widened; the three-month cross-swap between the pound and the dollar widened, and the cross-swap between the yen, euro and the dollar narrowed. The amount of reverse repos used by major US financial institutions on the Fed's books has fallen, but it is still more than $2 trillion per day.

► Emotional position: Xinxing is approaching oversold, euro bulls rise sharply, silver turns short

The bearish / bullish ratio of US stocks (10-day average) has risen over the past week, and emerging stocks are close to overselling. In terms of positions, speculative net short positions in US stocks decreased, while emerging net short positions increased; euro speculative net long positions increased significantly; gold speculative net long positions continued to decrease and silver turned to net short positions.

► capital flows: emerging markets, bond funds turn into inflows

Over the past week, bond funds have turned to inflows, while inflows into money market funds and equity funds have accelerated. From a sub-market point of view, developed Europe continued to outflow, the inflow of the United States and Japan accelerated, and emerging markets turned into inflows; among emerging markets, China, Brazil and South Korea recorded inflows, while China inflows were obvious.

Fundamentals and policies: the GDP of the United States improved in the third quarter compared with the previous quarter, the core resilience remained, and the PMI of the service industry and manufacturing industry in Europe and the United States declined.United States:

Markit manufacturing PMI fell to contraction range, service industry continued to decline. The US Markit manufacturing PMI fell to 49.9 in October, below expectations of 51 and a previous value of 52, falling into a contraction range for the first time since June 2020. Itemized, new orders returned to the contraction range, falling to 46.7 from 51.1 in September, indicating that current demand is weakening; purchase and factory prices have fallen, but they are still high and price pressure remains; supply delivery continues to repair, and the employment segment has fallen. PMI in the service sector continued to decline to 46.6, below the rise and fall line for four consecutive months. Itemized, price pressure in the service sector rose slightly, new orders reflecting demand declined, and employment fell to a contraction range.

GDP improved month-on-month in the third quarter and exceeded expectations. In the United States, the annualized rate of GDP in the third quarter was 2.6%, indicating that it was too early to worry about a technical recession caused by negative growth data in the first and second quarters. Itemized, commodity consumption continued to decline (- 0.28%), real estate investment declined (- 1.37%), destocking continued (- 0.7%), and imports weakened (1.14%). On the contrary, service consumption is still resilient (1.24%), indicating that growth may not enter a recession so quickly, but the weakening direction is still obvious. We expect an eventual recession is also a high probability, possibly in the first half of next year, but the benchmark situation may not be very deep.

PCE growth slows compared with the same period last year, but core PCE toughness remains. The US PCE price index rose 6.2 per cent in September from a year earlier (expected 6.3%vs. The previous value was 6.2%), which slowed for the third month in a row, with a month-on-month increase of 0.3%, unchanged at the expected and previous value. Core PCE growth rose to 5.1 per cent year-on-year (expected 5.2%vs. The previous value was 4.9%), an increase of 0.5% over the previous month. In the breakdown data, the gasoline fuel segment fell significantly from the previous month, but the rate of decline slowed compared with August; transport services, including motor vehicle services and public transport, increased significantly (2.1%).

PCE growth slows compared with the same period last year, but core PCE toughness remains. The US PCE price index rose 6.2 per cent in September from a year earlier (expected 6.3%vs. The previous value was 6.2%), which slowed for the third month in a row, with a month-on-month increase of 0.3%, unchanged at the expected and previous value. Core PCE growth rose to 5.1 per cent year-on-year (expected 5.2%vs. The previous value was 4.9%), an increase of 0.5% over the previous month. In the breakdown data, the gasoline fuel segment fell significantly from the previous month, but the rate of decline slowed compared with August; transport services, including motor vehicle services and public transport, increased significantly (2.1%).

Europe: manufacturing and services PMI continued to decline.Euro zone Markit manufacturing PMI fell to 46.6 in October, below the previous figure of 48.4 and expectations of 47.9, the lowest since May 2020. New orders and output reflecting demand have fallen significantly, price pressures have fallen, but remain high, and employment and supply delivery have improved. Services PMI fell to 48.2, flat but lower than the previous value of 48.8, the lowest since November 2020, while the segment of new orders is still below the rise and fall line, indicating that demand is still weak.

Market valuation: still above reasonable levels of growth and liquidity

Market valuation: still above reasonable levels of growth and liquidity

The current S & P 500's 16.8-fold dynamic PPease E is higher than the reasonable level (~ 13.6 times) that can be supported by real interest rates and high-yield spreads.

Edit / ruby