结构性心脏病介入新技术沸腾了国内的心脏介入产业,多家企业布局了相关赛道。在国内众多企业中,乐普医疗子公司心泰医疗是中国结构性心脏病介入医疗器械行业的先行者及先天性心脏病封堵器械国内领先的供应商,20余年来,始终专注于结构性心脏病介入医疗器械的研发和生产。

结构性心脏病介入新技术沸腾了国内的心脏介入产业,多家企业布局了相关赛道。在国内众多企业中,乐普医疗子公司心泰医疗是中国结构性心脏病介入医疗器械行业的先行者及先天性心脏病封堵器械国内领先的供应商,20余年来,始终专注于结构性心脏病介入医疗器械的研发和生产。In 2018, Academician GE Junbo, an interventional expert in heart disease, pointed out during China structure week that the new technology of structural heart disease opened and represented the fourth cardiac revolution of interventional cardiology.

The speeches of the bosses are often profoundly predictable, and structural heart disease has become the main theme of the innovation and upgrading of domestic cardiology medical devices after 2018. The domestic market for structural heart disease is also experiencing rapid growth.

After 2020, new instruments and technologies for structural heart disease continue to emerge in China, and the cumulative number of surgeries has increased significantly. The number of TAVR cases in China is growing at an annual rate of nearly 50%, surpassing the development speed of all previous interventional techniques; at the same time, patent foramen ovale occlusion (PFO) and left atrial appendage closure (LAAC) are also showing a rapid development trend. According to Frost Sullivan, the domestic market for structural heart disease has also grown from 400 million yuan in 2017 to 2 billion yuan in 2021.

The new technology of structural heart disease intervention has boiled the domestic heart intervention industry, and a number of enterprises have laid out related tracks. Among many domestic enterprises, Xintai Medical, a subsidiary of Lepu Medical, is a forerunner in China's structural heart disease intervention medical device industry and a leading domestic supplier of congenital heart disease blocking devices for more than 20 years. Always focus on the R & D and production of structural heart disease intervention medical devices.

The new technology of structural heart disease intervention has boiled the domestic heart intervention industry, and a number of enterprises have laid out related tracks. Among many domestic enterprises, Xintai Medical, a subsidiary of Lepu Medical, is a forerunner in China's structural heart disease intervention medical device industry and a leading domestic supplier of congenital heart disease blocking devices for more than 20 years. Always focus on the R & D and production of structural heart disease intervention medical devices.

At present, Xintai Medical is applying for listing on the main board of the Hong Kong Stock Exchange. as a new wave of cardiology interventional therapy, what are the follow-up growth points in the structural heart disease market? As the leader of the first three revolutions of cardiology interventional therapy, how will the subsidiary of Lepu spin-off settle in the field of structural heart disease? The arterial network was combed.

Structural heart disease is booming

The core of the three major markets

From 2009 to 2019, US stocks created 14 tenfold pharmaceutical stocks with a market capitalization of more than $10 billion, of which five were innovative medical device stocks, namely, Intuitive Surgical in surgical robots, Acci in oral invisibility correction, Dexcom in continuous blood glucose monitoring, and Edward Life Sciences and Abiomed in structural heart disease.

Among them, only two companies have been born in the field of interventional treatment of structural heart disease in a decade, and the global market for structural heart disease has reached US $9.3 billion in 2021. Why interventional treatment of structural heart disease can lead to two myths of creating wealth.

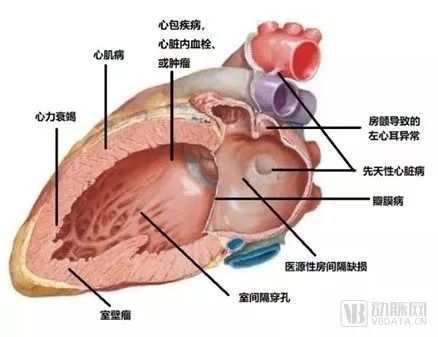

Because if a person lives to be 80, his heart needs to beat more than 2.5 billion times, in such a heavy work, every part of the heart may have problems. Heart problems can be divided into three categories, including coronary heart disease, arrhythmia and structural heart disease, while structural heart disease mainly includes congenital heart disease, valvular disease, cardiomyopathy and complications caused by other conditions (such as atrial fibrillation). Increases the risk of cardiogenic stroke and myocardial infarction.

Types of structural heart disease

In the 1950s, invasive cardiac catheterization already allowed doctors to detect congenital heart disease and valvular disease, but at that time the treatment required thoracotomy. With the application of new technology of minimally invasive interventional therapy in the field of structural heart disease, the global market for the treatment of structural heart disease has ushered in rapid growth.

In China, the maturity of several subdivisions of interventional therapy for structural heart disease is different. Interventional therapy of congenital heart disease is the most mature; interventional therapy of valve is in rapid development; prevention of atrial fibrillation is in the early stage of development; adjuvant therapy of heart failure is in the early stage of exploration.

First of all, let's take a look at the relatively mature interventional occluder market, which includes precordial occluder and left atrial appendage occluder.

The first heart occluder is used to treat congenital heart disease. About half of the CHD of congenital heart disease is ventricular septal defect (VSD) and atrial septal defect (ASD). The global market scale of congenital heart disease occluders includes only three congenital heart disease occluders (atrial septal defect occluder, ventricular septal defect occluder and patent ductus arteriosus occluder).

The technology of congenital occluder has been developed for more than 30 years, and the method of operation is more mature. The total amount of interventional treatment of congenital heart disease in China has ranked first in the world, with about 75000 cases of congenital heart intervention in 2021.

In addition to cardiac interventional occluder, the occluder also includes cardiogenic stroke occluder, which mainly includes patent foramen ovale and left atrial appendage occluder products. Cardiogenic stroke can be prevented by implanting cardiogenic occluder, which is currently the most fatal disease in China. More than 3 million stroke patients were admitted in China in 2021. The development of cardiogenic occluder in China is still in the emerging market.

What can not be ignored in the structural heart disease market is the rapid rise of valve intervention in the past decade.

In 2002, Professor Alain Cribier, a French interventional cardiologist, completed the first TAVR (transcatheter aortic valve replacement) operation in the world, and minimally invasive intervention was used to treat aortic disease. in the past, valve surgery can only be performed by thoracotomy, but thoracotomy is taboo for more elderly and high-risk surgical patients.

The new TAVR technology marks the prelude to a golden two decades of valvular interventional therapy, with global sales of valvular interventional devices reaching $7.1 billion in 2021, according to Frost Sullivan.

The valve market in China is in the early stage of rapid development, and the number of TAVR surgeries is increasing rapidly at a rate of 50%. However, from the perspective of permeability, the permeability of valvular interventional instruments is seriously low. Due to a shortage of qualified hospitals with experienced doctors, only 0.8% of eligible patients received transcatheter aortic valve replacement in 2021, compared with 4.3% worldwide. China's market for transcatheter aortic valve replacement is significantly inadequate.

Generally speaking, in the context of aging, aortic stenosis, aortic regurgitation and mitral / tricuspid regurgitation have become the mainstream types of structural heart disease that seriously threaten the health of residents. The number of these patients has increased significantly, giving rise to a huge demand for clinical diagnosis and treatment. The domestic market for structural heart disease is experiencing rapid growth in the context of new technological changes and the growing demand for clinical diagnosis and treatment.

A burst of vitality in the field of structural heart disease

Four new trends are emerging.

The new technology of interventional valves in the field of structural heart disease has created a global market of nearly 10 billion yuan from scratch. What else are the highlights of the structural heart disease market in the future? Four trends have attracted global attention.

For congenital heart occluder, biodegradable occluder is the direction of research and development. At present, the occluders on the market for interventional treatment of congenital heart disease are basically made of non-degradable nickel-titanium alloy, which will remain in the human body permanently, which is not ideal for children. The development of biodegradable occluder has become the trend of the next generation of congenital heart disease occluder, but it is faced with the challenge of material technology.

In the field of LAA occluder, new LAA occluder devices are developed and applied clinically, which makes LAA occlusion more safe, effective and convenient, and minimalist LAA occlusion surgery is widely carried out.

For interventional valves, the improvement of anti-calcification and durability of TAVR products makes the promotion of TAVR to young patients is a major direction, for doctors, precision release to improve the success rate of implantation is another major direction.

In addition to aortic valves, innovations in mitral and tricuspid valves are also to be expected. In clinic, the patient base of mitral valve and tricuspid valve is more than that of aortic valve, but the development of interventional therapy of mitral valve and tricuspid valve lags behind. Mitral and tricuspid valves are also considered to be the main components of the future market for structural heart disease.

In addition to the intervention of occluders and valves in the race track, the attention in the field of heart failure has also begun to increase, and the field of structural heart disease is in the stage of innovation.

Structural heart disease, a track with great momentum for change, has been favored by many giants, and whoever controls the track will dominate the heart disease market in the next decade.

At present, which companies dominate the structural heart disease track?

In the occluder market, according to the data reported by Frost Sullivan, the scale of the domestic occluder market reached 426 million yuan. The domestic market has basically been localized, and the share of domestic products has exceeded 91.5%. Among domestic companies, Xintai Medical has the highest market share, reaching 38%. In 2018, Xintai Medical completed the world's first fully degradable VSD interventional therapy, bringing a new breakthrough in the global biodegradable occluder field.

In the market of cardiogenic stroke occluder, the occluder therapy of patent foramen ovale is still in the emerging stage, with the participation of four domestic companies, the alloy-based occluders of AGA Medical and Beijing Huayi Shengjie have been approved to market, Xintai Medical's biodegradable foramen ovale occluder is in the registration preparation stage, and the biodegradable foramen oval occluder of Shanghai Jinkui Medical is in the clinical trial stage.

The global LAA occluder market reached US $900 million in 2021, and the domestic LAA occluder permeability is still very low. According to Frost Sullivan, the permeability is only 5.9%, compared with 44.9% and 14.6% in the United States and Europe. Therefore, at the present stage, the domestic market scale of left atrial appendage occluder is also relatively small, with a market scale of 500 million yuan in 2021. A number of companies have launched left atrial appendage occluder products, including Xintai Medical, Boston Science, Abbott Laboratories, Xianjian Technology. Boston Science is the market leader of left atrial appendage occluder, and its left atrial appendage occluder product achieved sales revenue of about $830 million, or about 5.5 billion yuan, in fiscal year 2021. The domestic market has not been fully developed. At present, Xintai Medical's biodegradable left atrial appendage occluder has completed type testing and animal experiments, and is about to enter the clinical stage. With the help of domestic substitution and technological innovation, Xintai Medical is expected to overtake in the curve with the help of degradable left atrial appendage occluder.

In the interventional valve market, according to Frost Sullivan's data, the market size of interventional devices for valvular disease in China has reached 1 billion yuan in 2021 and is expected to increase to 7.9 billion yuan in 2025, with an annual compound growth rate of 69.8%. At present, nine TAVR products have been commercialized in the domestic market. In 2021, there are more than 6500 TAVR operations in China (including meridian and apical operations, excluding clinical studies), but in 2020, the number of TAVR operations in China is only 3500.

In the mitral valve market, only Abbott Laboratories's mitral edge repair product MitraClip has been approved and listed in China, and MitraClip has also been certified by FDA and CE. In the Chinese market, there are more than 14 enterprises in the mitral valve market. In 2021, there were about 350 cases of transcatheter mitral marginal repair (TEER) in China.

Structural heart disease market is complex and diverse, in the first heart intervention market gave birth to the domestic invisible champion Xintai Medical, while the whole valve market is still in the warring States period. The cardiogenic stroke market is in the early stage of development, and the domestic substitution trend is obvious.

The domestic market for structural heart disease has complex characteristics and a large patient base, but due to the relatively higher learning difficulty and longer learning curve of interventional therapy for structural heart disease, lack of market education and experienced practitioners, and many enterprises in product research and development, but the homogenization is serious.

To break through the structural heart disease market, there are high requirements for the long-term clinical needs understanding ability, commercialization ability and market education ability of enterprises.

Deep ploughing the market of structural heart disease

Local leader sprint IPO

In the emerging structural heart disease intervention R & D enterprises in China, Xintai Medical has been involved in structural heart disease for more than 20 years.

Xintai Medical is the invisible champion in the field of cardiac intervention. Xintai Medical developed the first VSD occluder made in China, won the second prize of national scientific and technological progress, and ranked first in the market share in the field of cardiac intervention for many years in a row.

Xintai Medical is not only pioneering in the field of cardiac intervention, but also making continuous iterative innovation. Backed by parent company Lepu Medical's leading biodegradable technology, Xintai Medical has applied biodegradable technology to the field of structural heart disease, launched the world's first commercial fully degradable occluder MemoSorb ®, and has laid out five original biodegradable products.

Compared with the traditional metal occluder, the biodegradable occluder is designed to be gradually degraded into carbon dioxide and water. Since the biodegradable occluder will not remain permanently in the human body, it provides patients with other future treatment options.

Biodegradable technology will lead to market expansion in the field of plugging. Xuanxin occluder products have entered the industrial harvest stage, and the market capacity has expanded from about 1.5 billion yuan in the past to nearly 5 billion yuan. Due to the upgrading of Xintai Medical products, MemoSorb ®fully degradable occluder will monopolize the market opportunity in a certain period of time.

In the valve field, Xintai Medical is not the first company to enter the market. How can Xintai establish its competitive advantage in this highly competitive market?

Xintai Medical's strategy is to establish an advantage through innovative products in the field of valvular disease and achieve curve overtaking in the valvular field.

In terms of pipeline layout, Xintai Medical has laid out four major valve races: aortic valve, mitral valve, tricuspid valve and pulmonary valve, in which TAVR and mitral chordae tendineae repair and valve clip repair have entered the clinical trial stage.

In the product route, Xintai Medical has chosen a differentiated design path. The original design of Xintai Medical ScienCrown TAVR conforms to the trend of younger patients on the patient side; on the doctor side, the "short valve + complete recovery system" can effectively reduce the operational risk of doctors.

In addition to innovation, Xintai Medical's advantages in the valve field also include the patience to cultivate the market.

In recent years, domestic medical devices often show a trend, before the outbreak of demand, participants flock to the supply first. However, the demand of the medical industry needs to be cultivated for a certain period of time, and the demand for the operator in the valve intervention industry, which is difficult to operate, is higher, the cultivation of the market needs capital and time, and the market needs to reach a certain market scale in order to develop automatically. The domestic valve intervention industry is expected to break out in 2024 and 2025. Xintai Medical has a rich pipeline layout in the field of valvular intervention, and strategically hopes to meet the outbreak of the market with innovative products.

In the design of interventional mitral valve system, the interventional mitral valve system is divided into two routes: repair and replacement, and the repair products have many surgical routes, such as marginal mitral valve repair, annuloplasty, chordae tendineae repair, annular reconstruction and so on. Xintai Medical's mitral valve products have two major routes of repair and replacement at the same time, covering a variety of product routes, such as edge-to-edge repair, chordae tendineae repair, annulus repair, annulus reconstruction and so on. It can provide solutions for different mitral valve patients.

In terms of market education ability, Xintai Medical has ploughed structural heart disease for 20 years and has accumulated rich and professional commercial experience and resources. At the same time, Xintai relies on Lepu Medical, which has more than 20 years of practical experience in the cardiovascular field, and has successfully counterattacked and seized the market segment many times.

In terms of commercialization, Xintai Medical has also shown strong profitability, and it is a rare profitable and fast-growing enterprise in the heart section of Hong Kong's capital market structure. In the first half of 2022, the revenue of Xintai Medical was 125 million yuan, compared with 110 million yuan in the same period last year, and the operating profit was 34 million yuan, compared with 46 million yuan in the same period last year. The gross profit margin of the company from 2018 to 2020 is 87.9%, 88.3% and 89.8% respectively; the profit is 38.61 million yuan, 51.91 million yuan and 68.77 million yuan respectively, and the net profit rate is 39.0%, 44.6% and 46.4% respectively.

From the perspective of long-term development, Xintai Medical uses the degradable technology platform to consolidate its advantages in the field of interventional occluders, and actively participates in the construction of domestic interventional valve market with the help of Xintai Medical's specialized market education and training experience in the structural heart disease market. Look forward to Xintai Medical to make more contributions to the domestic structural heart disease market in the future.

In the past decade, the wave of change in the field of structural heart disease has been blowing continuously in China's clinic. under the warm wind, it has changed the domestic industrial ecology, and the seeds of innovation have also fallen. The gap between China's structural heart disease innovation medical equipment and the world has gradually narrowed. Enterprises such as Xintai Medical have led global innovation for many times. In the land of structural heart disease, which has not been fully reclaimed, can it grow into a towering tree? Let's wait and see.

* reference articles

Xintai Medical prospectus

With the accelerated rise of domestic innovative equipment of left atrial appendage occluder, can we overtake in these 10 billion track bends? China Medical Science and Technology Network

Structure 2021 report hit-structural heart disease intervention is booming, and there is still a lot of room for improvement in a number of technologies-"outpatient clinic"

Academician GE Junbo: the definition, category, present and future of structural heart disease