Source: Yuanchuan Investment Review

Author: Huang Xiaofeng

Of the four funds currently managed by Zhang Kun, 2 start with 'quality' and 3 end with 'selected'. In September last year, Zhang Kun's famous masterpiece "Yi Fangda small and medium-sized disk" was directly renamed "Yi Fangda quality selection", and the Buff was covered with two layers.

It seems that starting from the name of the fund, Zhang Kun is trying to express Zhang Kun's value investment concept of "going down together with good business model and competitive enterprises for a long time". But the different product designs and investment ranges of the four funds show that this is not an easy task.

To put it simply, the investment scope of "Yifangda Blue Chip Select" is similar to that of "Yifangda high-quality enterprises held for three years". They can both invest in A-shares and Hong Kong Stock Exchange companies, the main difference is that the latter has a three-year closed holding period. As a QDII fund, Yi Fang Da Asia Select can not only buy companies within the scope of Hong Kong Stock Connect, but also choose all companies listed on the Hong Kong Stock Exchange and Asian companies listed on other exchanges, so its main positions are concentrated in Hong Kong stocks and Chinese-listed stocks. Yi Fang quality Select originally could only invest in the A-share market, but after changing to a QDII fund, the scope of investment became A-shares and all companies listed on the Hong Kong Stock Exchange.

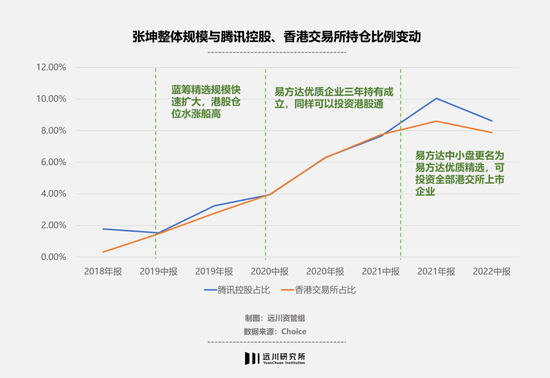

In the past few years, Zhang Kun has been in the three major markets of A shares, Hong Kong stocks and US stocks.Really do not fear market fluctuations, long-term maintenance of high positions in the 'quality selection' stocks are 5-Guizhou Moutai, Wuliangye, Luzhou laojiao, Tencent and Hong Kong Exchanges and Clearing.

Although the bottom stocks iterative, frequent ups and downs, but Guizhou Moutai, Wuliangye, Luzhou laojiao three liquor stocks have always been maintained in the top range of high positions. Although Tencent and Hong Kong Exchanges and Clearing did not account for a high proportion in the overall management scale of Zhang Kun at the beginning, they have been expanding together according to the expansion of Zhang Kun's position in Hong Kong stocks.

Since the end of 2017, Yi Fangda Asia Select has been holding large positions in Tencent and HKEx. Blue-chip selection was established in 2018, and the two stocks in its Hong Kong stock position have also been heavily allocated for a long time. However, because the two funds were not as large as Yi Fangda's small and medium-sized companies at that time, they accounted for a relatively low proportion of Zhang Kun's overall size.

But since then, no matter whether Yi Fangda's high-quality enterprises have been held and established for three years, or after small and medium-sized companies have changed their names to high-quality selections, they can see that Tencent and the HKEx firmly occupy the ranks of key stocks in their Hong Kong stock positions from the beginning to the end. finally reached the level of position on a par with the 'Mao Wu'.

Maotai, Wuliangye, Luzhou laojiao, Tencent and HKEx are basically the "bottom positions of faith" held by Zhang Kun, which is a concrete manifestation of Zhang Kun's company with a good business model, strong competitiveness and can accompany growth for a long time. The rotation of the remaining 6 to 20 stocks can better reflect Zhang Kun's judgment of the market and his choice under unexpected circumstances.

Among them are traditional core asset leaders China Merchants Bank, Yili shares, and Shanghai Airport, as well as the legions of 'beggars' BABA, JD.com, Meituan, and Kuaishou Technology, who continue to make bottoms. The more controversial new consumer leader Pop Mart International and the new Jinshun cycle hot CNOOC.

The constant belief position is the cornerstone of Zhang Kun's investment concept, and the position changing in different market environment is also the key to understand the whole investment context of Zhang Kun.

01 '7ft' railing

Before 2020, liquor and medicine have been Zhang Kun's one or two major industries for a long time. But in Zhang Kun's eyes, the pharmaceutical industry is more like Buffett's "7-foot" railing-it is more difficult to invest.

In consumer goods, pharmaceuticals and technology, the three areas in the world that are most likely to produce large companies, the pharmaceutical industry is more likely to make small companies grow than the other two, that is, industries with less stability and lower brand moats. Because this is a product-driven industry, as long as effective drugs can be made, the restrictions on brands and channels are not as strong as in the field of consumption and technology.

Therefore, Zhang Kun's investment in the pharmaceutical industry is not as concentrated as spirits. There are blood products companies such as Hualan Biology and Tiantan Biology, which also have great advantages on the supply side, Ayre Ophthalmology with scale and brand effect, tablets with stronger consumer attributes, General Healthcare that walks out of the alternative mode of oral cavity, and Wuxi Biologics, the leader in the global CDMO industry.

Among them, Hualan Biology is relatively more in line with Zhang Kun's scarcity aesthetics on the supply side, because there are no new blood products enterprises since 2001, with certain license barriers. Although Hualan Biological reported lower-than-expected results in 2017, falling by more than 20% in nine days, Zhang Kun chose to keep making bottoms and finally reaped the market that Hualan Biological had more than tripled in the next three years.

However, after mid-2020, affected by the collection policy, the pharmaceutical industry has undergone great changes on the supply side. Zhang Kun also began to reduce the allocation proportion of the pharmaceutical industry, and almost cleared pharmaceutical stocks at the end of 2021.However, in the middle of this year's reporting season, when the pharmaceutical industry broke the record of public offering fund positions since 2018, Zhang Kun's four funds chose to increase their positions in Wuxi Biologics, copying the bottom of medicine with a small proportion of positions.

However, the pharmaceutical industry is not the only industry that Zhang Kun finds it difficult to invest, but still insists on research and investment. Another industry that Zhang Kun is passionate about also makes him feel that it is difficult to invest, that is, the Internet industry.

Similar to the pharmaceutical industry, Zhang Kun's investment in the Internet industry is also relatively scattered, and because Internet companies are distributed in the Hong Kong stock market and the US stock market, they are limited by the scope of investment. in addition to the "belief warehouse" Tencent, it is difficult to see Zhang Kun's preference for other Internet companies in his position.

For example, although Meituan is the second largest Internet company besides Tencent in Zhang Kun's overall size, among the two QDII funds selected in Asia and high-quality selection, BABA and JD.com accounted for a higher proportion of positions than Meituan in the second quarter of this year. In addition, both non-QDII funds hold Kuaishou Technology, but the positions of the two QDII funds are not in the list.

But in any case, the Internet industry has become another embodiment of Zhang Kun's' confrontation with the market'in the past few years.In the miserable years of Chinese stocks, Zhang Kun left a lot of positions for his favorite Internet companies, whether when Yi Fangda's high-quality enterprises were held and established for three years, or when small and medium-sized stocks were changed to QDII.

As for the view of the Internet industry, Zhang Kun said in an interview: "the Internet industry has a charm, it can turn high returns into reinvestment in a short period of time, and then high returns, repeated cycles, and finally let enterprises grow up rapidly." "

This industry that quickly turns established advantages into dominance is also favored by Zhang Kun, who is keen to find a stable moat. It's just that this way can not only make them grow rapidly, but also they may encounter "good fortune, where misfortune lies".

Can 02 Alpha withstand the impact of Beta

In his new fund roadshow in 2020, Zhang Kun quoted Buffett as saying:My three best investment ideas may be similar to most investors, but my three worst ideas are much better than most investors.To prove this, Zhang Kun came up with the profit-to-loss ratio of Yi Fangda's small and medium-sized shares to 9:1 after the final sale of shares at that time.

In fact, in an interview with Zhang Kun, he also said that although he will have industry preferences and pay attention to balance and dispersion to a certain extent, most of the behavior that can really allow him to control the pullback comes from choosing some better companies. can also have enough fundamentals to support when falling.

This will not be a problem until 2020, because even the Shanghai airport, which was changed by the black swan at that time, should be profitable when clearing positions because of Zhang Kun's long holding period. But after 2020, a lot of things have changed, and Black Swan has shown its power.

Typical representative is Yi Fangda Asia Select once heavy position in the education and training industry. In the first quarter of 2021, Asia Select chose to buy more and more in the education industry, increasing the position of many general education stocks, of which TAL Education Group and New Oriental Education & Technology Group have become the top ten heavy stocks. However, with the tightening of policy in the second quarter, the share prices of a number of educational institutions fell to rock bottom, and Zhang Kun also chose to clear his position and leave the market.

In the second quarterly report of 2021 selected by Yi Fangda Asia, Zhang Kun wrote: "in the second quarter, the share prices of education and training enterprises fell greatly under the influence of policy expectations, which had a negative impact on the net worth of the fund, and made me reflect on some assumptions in the long-term investment framework. I hope to further improve it. "

In the fourth quarter of 2020, Haikang Weiwei, which Zhang Kun chose to buy, was also one of the victims of Black Swan.

In 2021, the United States banned Haikang from using US communications networks; in 2022, sanctions continued to increase, and Haikang could be included in the SDN. Under repeated sanctions, Haikangwei's share price fell by more than 50% from last year's high, and by the second quarter of this year, none of Zhang Kun's four funds had been listed as Haekangwei.

03 ending

The unity of knowledge and practice in investment is not only reflected by long-term holding, but also needs to be interpreted by action in every trade-off.

Looking back, Zhang Kun's investment thinking has always been relatively clear and firm: looking at the problem from a supply-side perspective, looking for companies with high barriers, stronger competitive advantage, and long-term excellent data such as ROE and ROIC. In the choice of industry, it is also based on several industries within its own ability circle, and it does not choose to invest in the 'new half army' industry because of prosperity.

There are not many enterprises that can meet Zhang Kun's investment criteria in the A-share market, so as the scale expands day by day, he also chooses to increase the proportion of positions in the Hong Kong stock market and invest in Internet companies that are optimistic against the market.

However, we should also note that Zhang Kun's previous failed investments were to a large extent not due to the problems of the enterprise itself.It is the macro environment and the black swan that have greatly changed the long-term assumptions and industrial choices of these enterprises.This is also an unavoidable risk in long-term investment.

In any stock market, companies that can really stand the test of time are extremely scarce, just as Zhang Kun's real 'belief warehouse' is also very limited.

However, as a public fund manager, under various risk control restrictions, how to evolve the portfolio management at the helm of nearly hundreds of billions of dollars from the critical aesthetic of stock selection, and break through the boundary of winning rate in the treacherous market environment? There are so many questions that you have to find the answer on your own in the end.

Edit / Corrine