Source: Wall Street

The much weaker-than-expected US ISM manufacturing index in September, weakness in credit markets and the Credit Suisse crisis have all increased the likelihood that the Fed will be forced to adjust its policy. Traders are now downgrading expectations for the Fed to tighten money and are again betting that the Fed will cut interest rates as soon as May.

On Monday, Oct. 3, eastern time, u.s. stocks opened higher, with all three major indexes rising more than 2% by midday, while bond prices rebounded and yields plunged.

The yield on the benchmark 10-year Treasury note fell below 3.57% in early trading on Monday, down 26 basis points from its intraday high above 3.80% in early trading in Asia, the first intraday drop of 26 basis points this year and the second such sharp decline in the past decade.

The media believe that the rebound in US stocks and US debt prices is partly due to the unexpected weakness of the leading indicators of US manufacturing released on Monday. In September, the US ISM manufacturing index was much lower than expected, falling to 50.9, close to 50% of the dividing line between stagnant manufacturing activity and a new low in more than two years. In addition, the credit market is weak and weak, andCredit Suisse which is betted by speculators on a Lehman-style crisisBoth increase the likelihood that the Fed will eventually have to adjust its policy in the midst of turmoil.

Wall Street noticed that it was only after US stocks released ISM data in early trading that the yield on 10-year Treasuries fell to its lowest level since September 22, giving up all the gains since the Fed raised interest rates aggressively for the third time last month by 75 basis points.

Traders have cut expectations of Fed tightening and are again betting that the Fed will cut interest rates as soon as May next year.

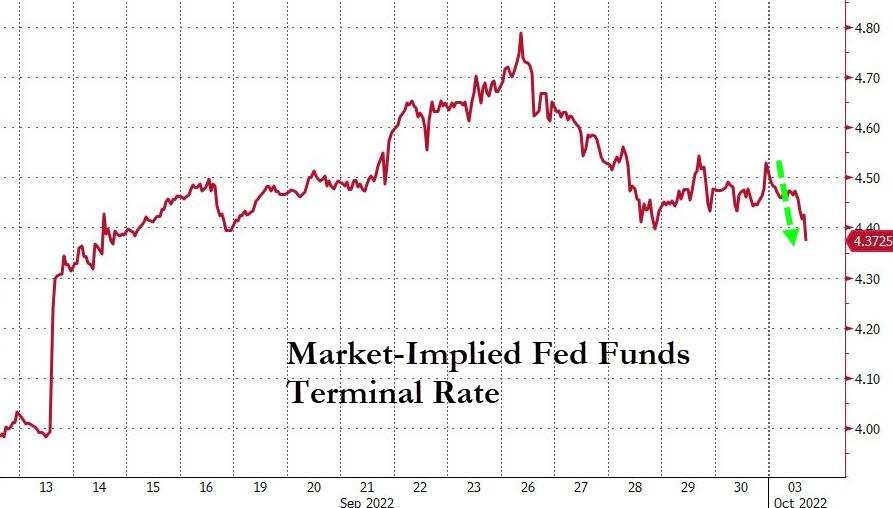

According to Bloomberg's global interest rate implied probability (WIRP), the market expected the Fed's terminal interest rate to be 4.38 per cent on Monday, down 14 basis points from the 4.52 per cent expected on Friday. Shortly after the Fed announced a 75 basis point hike at its meeting last Wednesday, the market expected interest rate reached a high of 4.7 per cent, equivalent to a 32 basis point drop from its high more than a week ago.

The market expects the Fed terminal interest rate to fall further.

The implied interest rates have been on a downward trend since May, suggesting that investors expect the economic slowdown to prompt a change in Fed policy.

However, the media believe that these investors betting that the Fed will cut interest rates next year may be disappointed. After the S & P 500's worst September in two decades, US stocks are set for a belated rebound and are likely to continue to rebound, but the market's strategy against the Fed has not really worked this year.

Investors are likely to take clues from Fed officials' comments last week, which are slightly different from the hawkish consensus expectations so far. While comments by Fed officials this week may add caution, it should be hard to see a departure from the Fed's consensus on resolute efforts to curb inflation, especially when the Fed's preferred measure of inflation is still at its highest level in nearly four years.

The core PCE price index, the Fed's preferred indicator of inflation, rose 4.9 per cent in August from a year earlier, faster than the 4.7 per cent expected in July and market expectations, but there were calls from market participants to start buying US stocks after the data were released.

Jim Paulsen, chief investment strategist at Leuthold Group, said in an interview on Friday that the Fed's monetary tightening may be coming to an end because inflation has peaked, which has been a good time to buy stocks.

Palusen points to a number of factors that have had the effect of monetary contraction, including slower monetary and fiscal growth, a stronger dollar and higher bond yields, which he expects to slow next year.

While Fed officials claim to be committed to the target of reducing inflation to 2 per cent, the Palusen believes they are close to meeting it.

"I don't know if the Fed has to do anything more. I think [they] may have won the war on inflation, but we just don't know yet. Historically, peak inflation has been a good time to buy stocks. "

Palusen pointed out that the current valuation of the S & P 500 is relatively low and investor sentiment is very pessimistic, which is generally seen by contrarian investors as good for the stock market.

He points to rising bond yields, falling commodity prices and increasingly unaffordable mortgage rates, citing flickering pessimistic signals across the economy as a sign of excessive Fed tightening.

Edit / roy