Source: Wall Street

The first domino collapsed.

Recently, the pension on which Britons depend for survival is on the verge of collapse, triggering a huge market shock and attracting the widespread attention of investors.

UK pension funds face massive margin calls because of the collapse in the price of gilts used for collateral, while the sale of margin positions could trigger a further collapse in the UK bond market, which is caught in a "death spiral". The Bank of England then rushed to buy long-term government bonds to save the bond market from fire and water.

Because UK pensions use interest rate swaps to hedge the risk of interest rate volatility, when gilt yields unexpectedly rise sharply, the floating yield they have to pay makes the strategy suffer a lot of losses.

The yield on 10-year UK government bonds has soared to 4 per cent so far this year, making it the biggest tipping point for the unexpected "black swan incident" and the crisis.

Although the Bank of England has stepped in, as long as gilt yields continue to rise in the future, the pension liquidity crisis is a time bomb that could detonate the market at any time.

The Operation Mode of British Pension-- hedging liabilities with LDI

The United KingdomEnterprisesOccupational pension provided to employees(different from the state pension)There are two main forms: defined benefit plan (Defined Benefit Plan,DB) and defined contribution plan (Defined Contribution Plan,DC).

In the history of pension development, because the DB plan can provide definite retirement benefits and resist longevity risks, providing employees with life-long old-age security has become a strategy and industry consensus for enterprises to attract employees.

The DB plan is also known as the final salary Pension Plan (Final Salary Schemes). Pension managers promise to pay a fixed amount of money when employees retire, so how much a client can get after retirement depends on how much the client is paying now, and has nothing to do with the manager's investment performance.

For the pension itself, the DB plan means that the amount of money it needs to pay customers in the future is fixed.If the pension needs to pay the client a pension of £1 million in 30 years' time, the pension can now buy gilts maturing that year. If you buy high-quality corporate bonds with higher yields, they can use extra money to invest in stocks, real estate or other growth assets in addition to buying bonds. Pensions themselves need to constantly adjust their investment plans to meet this goal.

There is a concept of Duration in the bond market, which refers to the average maturity time of bonds, that is, the average time for bondholders to recover all their principal and interest, which is mainly used to measure the sensitivity of bond price changes to interest rate changes.

Other things being equal, the longer the duration, the more sensitive the bond price to changes in interest rates. The 30-year duration means that the present value of the future cash flow of pensions (that is, the net present value of liabilities) is very sensitive to interest rates.

In addition, since most British pensions are linked to inflation, changes in inflation will also make the present value of pensions fluctuate. The higher the inflation, the more the pension will have to spend in the future, and the higher the net present value of the debt with the same interest rate.

For a long time, most British pensions have adopted a debt-driven investment strategy (LDI) to hedge their liabilities. When the discounted present value of the asset side and the liability side of the pension do not match, it is necessary to set the sensitivity of the asset side to nominal interest rate and inflation according to the sensitivity of the liability side to nominal interest rate and inflation.

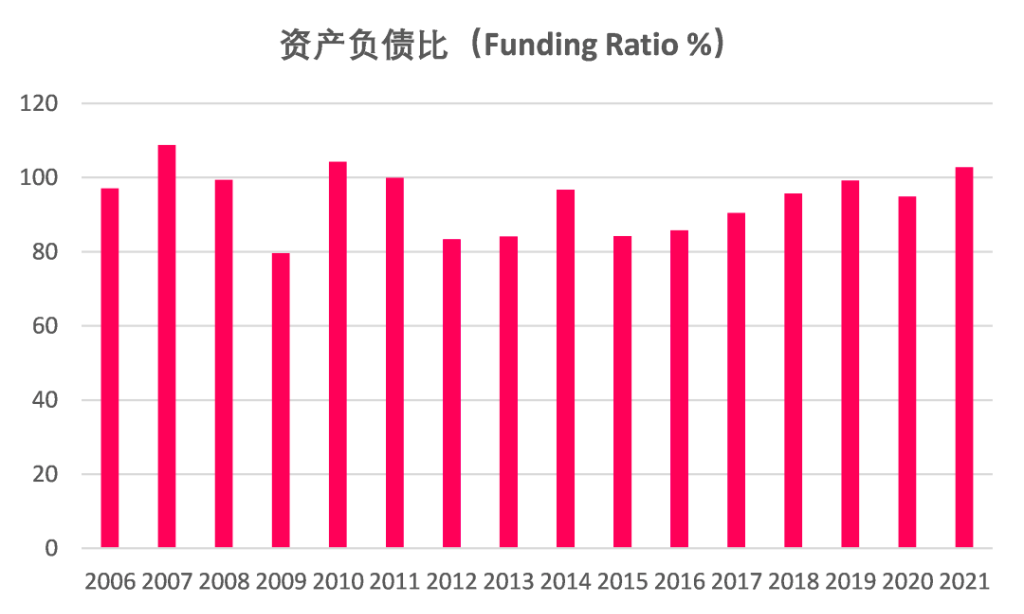

Millman, the consultancy, estimates that as of August 31 last year, total assets in UK pensions were equivalent to 106 per cent of liabilities.

The use of derivatives is more vulnerable to interest rate fluctuations.

As of March last year, the total assets of the UK's DB programme were about 1.7 trillion pounds, while those of the DC programme were 11.35 million pounds. DB plans to dominate the UK financial marketIt is one of the sources of systemic risk in the UK financial market.

Because of the large volume of the DB plan, it is necessary to breed its safeguard mechanism to hedge against the risk of large fluctuations. Pensions can use derivatives-interest rate swaps (Interest Rate Swap, IRS) to match interest rate risks, or inflation swaps (Inflation Swap) to match inflation risks.

Interest rate swap is the exchange of interest rate payments with different nature between the two sides of the transaction on the basis of the same nominal principal amount, in order to reduce financing costs. For example, one party can get a preferential fixed interest rate loan, but wants to raise funds at a floating rate, while the other party can get a floating rate loan, but hopes to raise funds at a fixed rate. Through the transaction, both parties can get the desired form of financing.

In recent years, British pensions often use the "pay floating rate and get a fixed interest rate" in interest rate swaps.The long-term treasury bonds bought by the pension are fixed interest income, which pays floating interest by signing an agreement with the counterparty, the investment bank.

Interest rate swaps only need to pay a small amount of collateral to investment banks to obtain long-term capital matching contracts. With preferential financing costs, pensions can buy higher-yielding stocks or corporate credit bonds. This can not only meet the regulatory requirements, but also achieve the time matching between the asset side and the liability side, but also obtain the income of the asset side.

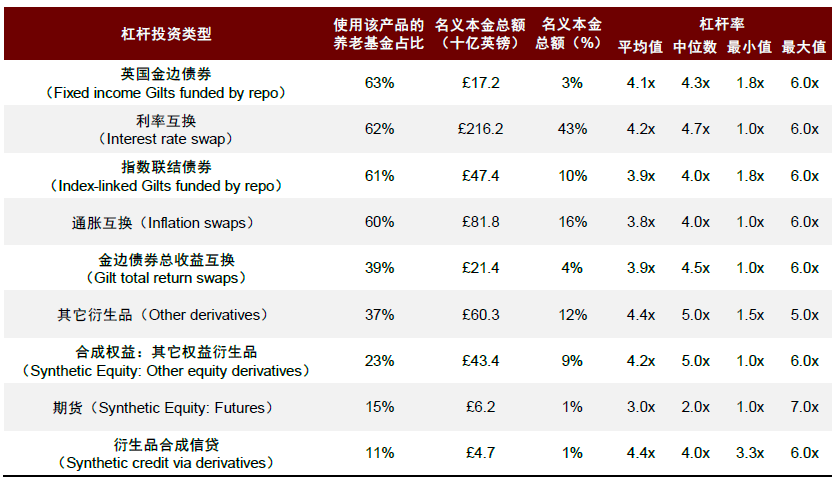

The UK Pensions Authority said in 2019 that 62 per cent of Britain's large pensions had at least some exposure to interest rate swaps.

(source: OMB Research, China International Capital Corporation Research Department * data as of the end of 2019)

In fact, leverage in pensions is a common industry phenomenon, and as long as it works well, UK regulators allow or even encourage this strategy to help funds manage interest rate risk. A guide from the UK Pensions Authority said the strategy usually "improves the balance between investment risks and returns, but it does introduce additional risks."

According to a 2019 survey of 137 large British pensions by the British Pensions Authority45% (nearly half) of pensions have increased the use of leverage in the past five years, with a maximum leverage ratio of up to seven times.

Us corporate pensions also increased the use of derivatives after the federal government required interest rates on long-term corporate bonds to measure corporate debt in 2006.

What happened in 2022?

As a floating rate payer, pension is very sensitive to long-term floating rate liabilities.

It is true that British interest rates have been falling all the way over the past two decades, and inflation has always been extremely low. In this case, the pension can be said to make a lot of money by paying floating interest rates and charging fixed interest income.

Since 2022, UK interest rates have gradually risen under the influence of a wave of interest rate increases by global central banks, and domestic inflation has soared to a 40-year high.

Especially after the British government announced the most aggressive tax cuts in half a century, the UK bond market set off a bloodbath: the yield on 30-year gilts soared by 120 basis points in just a few days, while the yield on 10-year gilts soared by more than 300 basis points in a year, becoming a "black swan event" that surprised the market.

According to media reports, Calum Mackenzie, an investment partner at pension fund consultancy Aon PLC, said that these pension strategies were basically implemented after the global financial crisis in 2008, so these positions have never been tested at a time when interest rates are rising rapidly.

When interest rates rise rapidly, floating interest payments far exceed the fixed income of long-term treasury bonds purchased by pensions, meaning that interest rate swaps are at a loss. The tricky thing, however, is that the government bond collateral provided by pensions to investment banks has plummeted because of soaring bond yields.

In this case, the deposit and collateral are quickly exhausted and the pension needs to be repaid.

Typically, pensions can "keep up" with the requirements of investment banks by investing in new high-yield bonds. However, the price of gilts has plummeted so fast that pensions do not have such time buffers and opportunities.The internal liquidity of the pension has been impacted and is facing great pressure of default.

To make matters worse, the continued sell-off of gilts has led to rising yields, which will lead to higher interest rates for pensions in interest rate swaps. Fund managers will have to sell more gilts (the most liquid) to make up the margin. Plunge it into a "death spiral".

For example, in a pension of $1 billion, an one-basis-point change in interest rates in the interest rate swap strategy generates a gain or loss of about 2 million. Over the past two months, the yield on 30-year gilts has risen by 230bp, and the loss from interest rate swaps is 460 million, nearly half of total pension assets.

UK pension assets totaled about £1.5 trillion at the end of August, up from £400 billion in 2011, according to the UK Pension Protection Fund (PPF). The loss of the entire pension over the past two months has resulted in about 690 billion of the margin to be paid.

The pension market in the UK is also huge: excluding government bonds held by the Bank of England, pension funds account for 40 per cent of the UK institutional asset management market and 2/3 of GDP.

If pensions need to sell assets to cover margin positions, the prices of all asset classes, including stocks and bonds, will tumble at the same time, causing a shock in financial markets. And that's exactly what British regulators don't want.

The impact on the market may be greater than the collapse of Lehman Brothers in 2008.

In the week from September 20th to September 27th, the price of 10-year gilts fell from 105.4 to 91.4. This is equivalent to a decline in the value of pension assets by 13.3 per cent (about £140 billion).

Fortunately, the Bank of England finally stepped in decisively to save the market, pulling the pension back from the brink.The Bank of England can ease the pressure on collateral by buying long-term government bonds to drive down yields, push up prices and reduce pension losses.

The Bank of England said in a statement last week that it would temporarily buy long-term gilts "on any necessary scale" to restore order in the UK bond market. The price of gilts soared across the board after the announcement, with 30-year yields tumbling by 100 basis points and the 10-and 30-year yield curves upside down for the first time since 2008.

If the Bank of England does not act in time, UK long-term government bond yields are likely to rise all the way to 6% or even 7%, pensions may face massive explosion and bankruptcy, and the pensions on which millions of Britons depend for survival will evaporate overnight. the entire British financial system will be thrown into chaos.

Some people in the market thinkBecause of the pensions of countless Britons, the crisis is likely to have a greater impact on the market than the collapse of Lehman Brothers in 2008.If the UK Pensions Authority fails to coordinate the issue of margin in interest rate swaps between pensions and investment banks in the short term, the asset-end value of pensions will depreciate sharply once long-term government bond yields soar again. Liquidity crisis could break out again at any time.

CICC said that in the short term, the Bank of England's "temporary QE" can repair bond market liquidity, stabilize asset prices and prevent the bond market liquidity crisis from turning into a debt crisis or even a full-scale financial crisis; but in the medium to long term, the Bank of England's temporary QE contradicts interest rate increases, and public expectations about the central bank's policy bias are more confused. The UK market turmoil and liquidity depletion are the result of disorderly fiscal stimulus, and then the Bank of England conducts a "temporary QE" to maintain market liquidity, which is equivalent to the central bank "covering the bottom" for the negative impact of fiscal expansion, and the risk of a decline in the credibility of the central bank and runaway inflation may further rise.

In addition,Whether UK long-term government bond yields will soar again is closely linked to the Fed's rate hike.If the Fed continues to signal hawkish interest rate increases at the next FOMC meeting, gilt yields are likely to follow this trend and the pension liquidity crisis will become a "time bomb".

Edit / roy