Source: Caihua Society

Author: Mao Ting

Since the second half of this year, the pace of tightening monetary policy by western central banks has been accelerating, with the Federal Reserve, the European Central Bank, the Bank of England and other "hawks" exasperating to curb domestic inflation.

Money begins to flee risky assets and park in safer havens, such as better-yielding dollars, waiting for winter to come.

How are global stock markets performing?

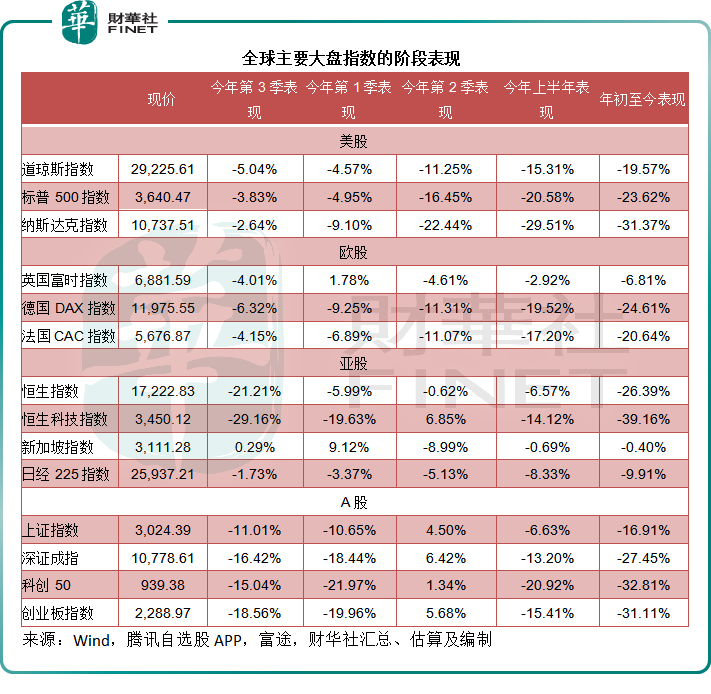

After the Fed raised interest rates by 75 basis points for the third time, the three major indexes of US stocks fell for several days in a row, accumulating some losses. At the close of trading on September 29, 2022, the Dow, the S & P 500 and the NASDAQ fell 5.04%, 3.83% and 2.64%, respectively.

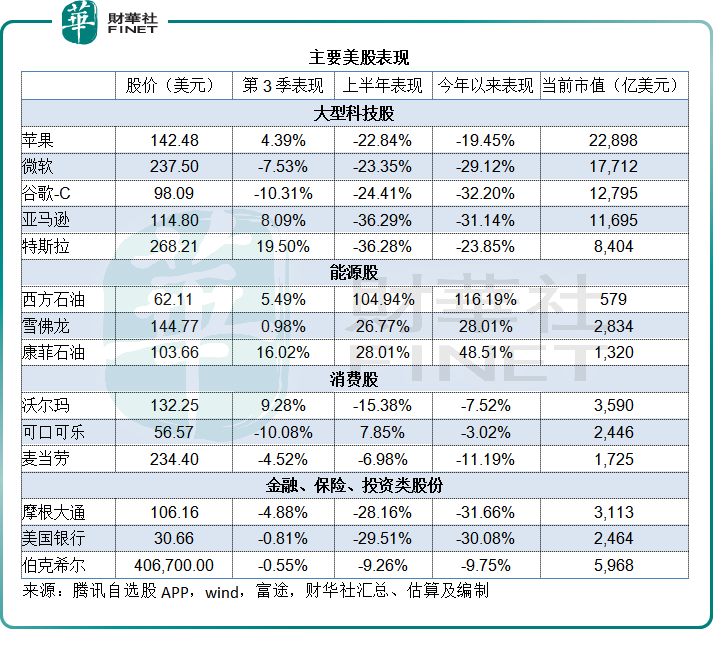

Among them, the weak performance of the large technology stocks with the highest market capitalization is an important reason for the decline of the major indexes, which has been weak in recent days.$Apple (AAPL.US)$It rose slightly by 4.39% in the third quarter, but it was not enough to offset the decline of Microsoft Corp, Alphabet Inc-CL C, Amazon.Com Inc and NVIDIA Corp.

On the other hand, after falling 36.28% in the first half of the year, electric car manufacturers$Tesla (TSLA.US)$It regained its rally in the third quarter, up 19.50%, bringing its market capitalization back to $800 billion.

Continue to be increased by Buffett.$Occidental Petroleum (OXY.US)$Maintained an upward trend in the third quarter, while$Chevron (CVX.US)$It seems to be lack of stamina.

Consumer stocks$Walmart (WMT.US)$After changing the declining trend in the first half of the year, it rebounded in the third quarter and outperformed.$Coca-Cola (KO.US)$和$McDonald's (MCD.US)$。

European stocks, which are also starting to "eagle", have also been affected by higher interest rates, with the UK's FTSE, Germany's DAX and France's CAC down 4.01 per cent, 6.32 per cent and 4.15 per cent respectively in the third quarter (which closed on September 29th, 2022).

From the perspective of time, both US and European stocks experienced sharp declines in the first half of this year. On the basis of this weakness, the decline in the third quarter was relatively moderate. However, Hong Kong stocks performed slightly better than European and US stocks in the first half of the year, and when the "water intake" accelerated in the third quarter, they were relatively more hit by selling, as shown in the table below.

Global IPOSerious shrinkage

When US stocks peaked last year, a large number of SPAC (special purpose buyout companies) emerged, making US stocks the world's largest IPO financing market last year. But IPO activity in U. S. stocks has shrunk sharply this year as the secondary market cools.

In the third quarter of 2022, there were 69 IPO cases in the US stock market, raising perhaps $2.994 billion, compared with 139cases of IPO and $55.028 billion of IPO in the third quarter of last year, according to Wind. In the first three quarters of this year, the number of IPO in the US stock market was 394, down from 1324 in the same period last year, and the amount of financing was $19.866 billion, down from $248.516 billion in the same period last year.

The five largest initial public offerings of US stocks this year, including two SPAC, two asset management companies and a medical equipment company, raised the largest or $168 million for asset manager Corebridge Financial (CRBG.US), far less than the tens of billions of dollars that US stocks peaked last year.

In terms of Hong Kong stocks, IPO activity in the Hong Kong stock market showed signs of picking up in the third quarter. According to Wind, 29 companies listed in the third quarter, raising HK $53.424 billion, accounting for more than half of the HK $73.153 billion in the first three quarters, surpassing US stocks.

The Hong Kong stock market welcomed the listing of a number of giants in the third quarter, including$CTG DUTY-FREE (01880.HK)$、$TIANQI LITHIUM (09696.HK)$、$LEAPMOTOR (09863.HK)$、$ONEWO (02602.HK)$And so on, the scale of financing and market capitalization can be called the largest of this year's IPO.

It is worth noting that since the beginning of this year, a number of Chinese-listed Chinese stocks have returned to the Hong Kong stock market, including$ZHIHU-W (02390.HK)$、$TUYA-W (02391.HK)$、$NOAH HOLDINGS-S (06686.HK)$和$MNSO (09896.HK)$Some of them are in the form of introduction to listing and non-financing, including$NIO-SW (09866.HK)$、$BEKE-W (02423.HK)$、$OCFT (06638.HK)$And the most recent$TME-SW (01698.HK)$。

In addition, four SPAC companies were listed on the Hong Kong stock market in the first three quarters of this year.

After the third quarter, a number of expected new economy and biotechnology companies will be listed on the main board of the Hong Kong Stock Exchange in early October, including Feitian Cloud Motion and the first share of power batteries.$CALB (03931.HK)$、$BETTERS MED (06678.HK)$The financing function of the Hong Kong stock market is still efficient.

The A-share market continues to be the most active listing place in the world. According to Wind, A-share financing in the third quarter of this year may reach 174.4 billion yuan, an increase of 8.26 per cent over the same period last year, while initial public financing in the first three quarters may be 486.3 billion yuan, up 29.65 per cent from a year earlier.

The largest A-share IPOs so far this year include China Mobile Limited, CNOOC, Lianying Medical, Haiguang Information and JinkoSolar Holding Co Ltd. See the table below, the share prices of these large companies have performed well after listing, with JinkoSolar Holding Co Ltd rising 233.40%.

Even so, breaking has become the norm in the IPO market all over the world, and A shares are no exception. Of the 304 A-share IPOs so far this year, 73 have broken on the first day of listing (calculated at the closing price on the first day of listing), accounting for 24%, and 140 have broken after listing (at the closing price on September 29), accounting for 46%.

The same is true of US stocks, which have fallen below the offering price of newly listed companies so far this year, according to Wind.

These data may mean that the performance of global stock markets continues to be under pressure against the backdrop of "water collection", so where is all the money?

Where does the money go?

As interest rates rise in the dollar and expectations of rising yields continue, money is flowing to assets with better earnings prospects, including the dollar and commodities, such as petrochemical energy, which is in short supply.

Since the beginning of this year, the cumulative price increase of crude oil has reached double digits, the increase of refined oil has been even greater, and the price of fuel oil has risen 41.01%. However, the price of gold, which usually acts as a Poseidon needle in inflation, has fallen, down 8.40 per cent so far this year.

As can be seen from the table below, both gold and energy prices fell sharply in the third quarter, and petrochemical energy prices fell even more than the stock market fell over the same period, mainly due to the poor global economic outlook. demand for these products may not be as good as expected, cooling the high prices of these commodities.

A more important reason is that these commodities are priced in dollars, and the Fed's interest rate hikes have led to a strengthening of the dollar and the fundamentals of commodities remain unchanged, so their dollar prices have been lowered accordingly.

So in the final analysis, the Fed's raising interest rates and shrinking its balance sheet led to a short-term flow of money to the dollar with higher potential yields, and led to a wave of money in global stock markets in the third quarter.

However, this situation should not last long. The Fed has raised interest rates by 3 percentage points this year and is expected to raise interest rates by 2023, with target rates as high as 4.6 per cent, meaning there is still room to raise interest rates by 1.35 percentage points. See chart below, the dollar index is up 17.26% so far this year.

The Fed cannot raise interest rates indefinitely because the hawk will completely deplete economic vitality, companies are reluctant to invest, consumers are reluctant to spend, and high interest rates will lead to economic contraction, which the central bank does not like to see.

At the end of the interest rate hike cycle, funds will be deployed again to look for assets with low risk and high returns. When the stock market falls to a level that squeezes out both risk and overvaluation, it naturally attracts money in pursuit of profits.

In the short term, the Fed's interest rate hike cycle may be in the middle, and the ECB is likely to expand the pace of interest rate hikes in the short term, so the hawk is still pressing in the fourth quarter of this year and the first half of next year, and the turnaround may occur at the end of the interest rate hike cycle, when inflation weakens and economic activity in the West slows.

A return to normal at home will bring a bigger catalyst to accelerate the recovery of the global economy.

So short-term capital markets are still likely to continue to fall, but the lower they go, the greater the potential for a rebound. The long-term recovery prospects of the global economy have not changed, and patient funds will be able to take advantage of low absorption opportunities to realize the return of "patience".

Edit / Corrine