Source: ZX Energy and carbon Neutralization Research, Wall Street

Authors: he Jianyun, Zhu Ziyue

Events: on the evening of September 27th, Beijing time, explosions occurred in the Beixi No. 1 and No. 2 pipelines, resulting in natural gas leaks at some sites. Gazprom announced that it was considering sanctions against Ukraine's state oil and gas company Naftogaz, and TTF gas prices rebounded to more than 200 euros / megawatt hours.

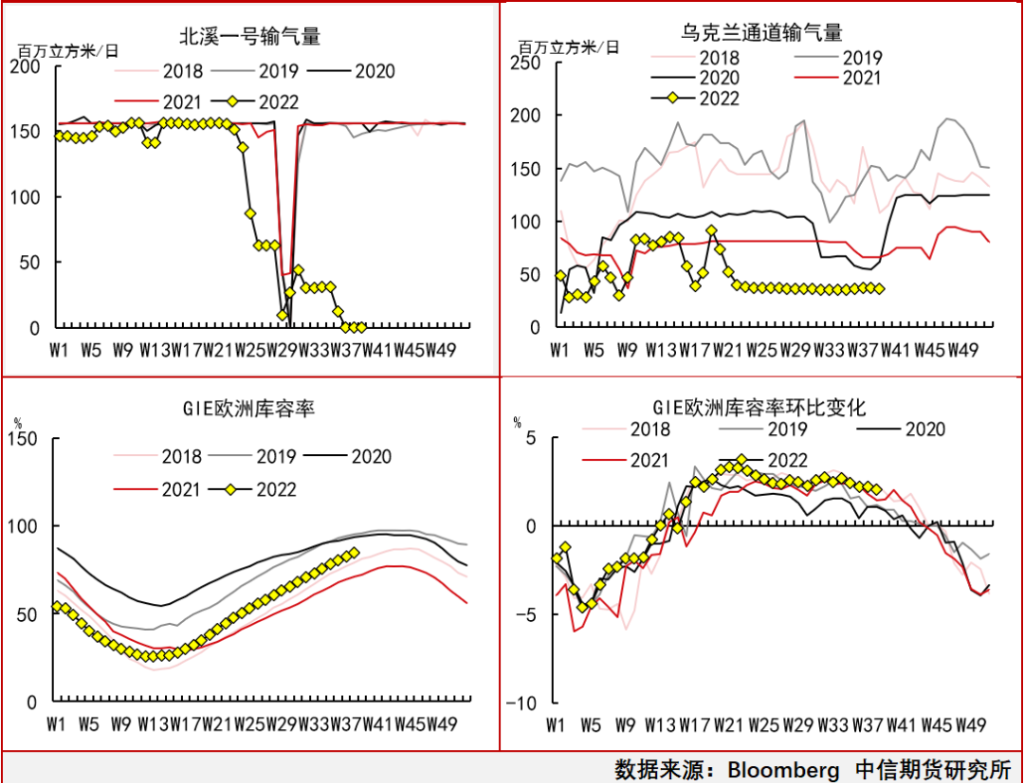

The explosion of Beixi pipeline has little impact. After the completion of Beixi 2, it was not actually put into operation, and Beixi 1 also began to stop supply indefinitely from August 30. Under the background of geographical conflict, the possibility of resuming operation of Beixi pipeline is extremely low.Even if the Beixi pipeline is completely scrapped, it will have little impact on the supply and demand of natural gas in Europe.

The explosion of Beixi pipeline has little impact. After the completion of Beixi 2, it was not actually put into operation, and Beixi 1 also began to stop supply indefinitely from August 30. Under the background of geographical conflict, the possibility of resuming operation of Beixi pipeline is extremely low.Even if the Beixi pipeline is completely scrapped, it will have little impact on the supply and demand of natural gas in Europe.

The dispute between Gazprom and Naftogaz was the main driver of last night's rise in gas prices. At present, Russia's pipeline gas export to northwest Europe is only about 37 million cubic meters / day of the Ukrainian channel. Gazprom said it would prevent Ukraine's oil and gas company from charging transit fees, which could lead to the risk of a cut in the supply of the only direct pipeline from Russia to Europe, prompting a rebound in TTF prices last night.But even in the case of a supply outage in Ukraine, we believe that the risk is relatively manageable, with gas prices or short-term spikes, but the impact on supply and demand in the heating season is limited.

Russia's influence weakens marginally, and the focus on the supply side is on LNG imports. From the perspective of supply risk, the current Russian gas volume is already on the low side. The amount of Russian natural gas imported into Northwest Europe is less than 100 million cubic meters per day, of which 37 million cubic meters per day comes from the Ukrainian channel, 0.5 to 60 million cubic meters per day comes from Russian LNG, and the rest comes from pipelines through Turkey. Russia's supply accounts for less than 10% of Europe's total imports, and the impact on the market has been marginal.The focus on the follow-up supply side is whether European LNG imports can remain strong.

Europe's LNG imports have been maintained at about 350 million cubic meters per day in the last four months, up more than 100% from the same period last year. If European LNG imports decline significantly in the fourth quarter, prices may rise again.

Pay attention to the later weather conditions and the speed of going to the library. At present, Europe has replenished its inventory to 87%, which is at a historically high inventory level, which has provided a certain margin of safety for the winter. If the EU can firmly implement the 15% consumption reduction target, the EU has sufficient natural gas stocks to make it through this year's heating season.

In terms of demand risk, Europe has begun to cool down, and prices could rise sharply again if this year's heating season is unusually cold and demand is much higher than expected, causing inventories to evaporate too quickly.

Edit / ping