Source: Wall Street

Author: Yin Hongchang

British natural gas futures rose more than 33% on Tuesday, while continental gas benchmark futures rose more than 21%, according to the World wide Web.

Can Europe survive this winter?

Data show that since the conflict between Russia and Ukraine, Europe has continued to replenish natural gas sources through multiple channels and directions, and specific measures include signing contracts and cooperation agreements with many countries to obtain natural gas supply, building LNG receiving stations to obtain larger receiving capacity, and building natural gas pipelines to increase gas sources.

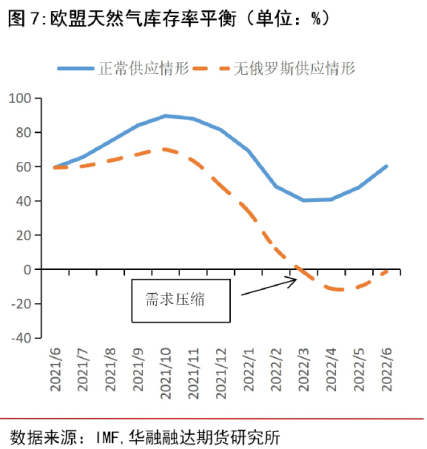

According to the Huarong Futures Research report, due to active purchases, the EU's natural gas reserves reached 85.58% as of September 17, which is catching up with the historical average and achieving the EU's target of 80% storage rate by November 1. Previously, the European Union passed legislation requiring the capacity of the EU's underground gas storage to reach 80% by November 1, 2022.

What does the target of 80% capacity ratio mean? How long will it last?

According to the Huarong Futures Research report, taking the current storage level as the starting point, and assuming that Russia has cut off the natural gas supply to Europe for a long time, IMF has made a brief calculation of the monthly natural gas storage, and the conclusions are as follows:

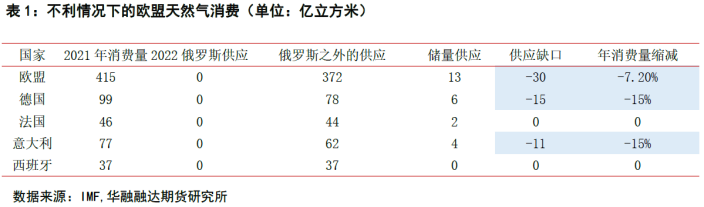

1) in the case of a total closure, there will be a serious shortage of natural gas in many parts of Europe and consumption will need to be adjusted, and EU winter consumption (from the beginning of November to the end of March) will need to be reduced by about 12% (7% per year, 3 billion cubic meters).

2) in the case of complete closure, the impact on the natural gas market may vary from region to region.

Britain, Ireland, Spain, Portugal, Sweden and Denmark can adapt to such supply disruptions because they are less dependent on Russian gas.

France, the Netherlands and Belgium are somewhat dependent on Russian natural gas, but they also have direct access to LNG import capacity and alternative pipeline supply routes, or they can be adjusted.

Germany and Italy, both highly dependent on Russian natural gas, will have a consumption gap of about 15 per cent (a total of 2.6 billion cubic metres).

Generally speaking, Huarong Futures believes thatIf the EU can reach an agreement to cut gas demand by 15% this winter, it seems to be able to make it through the winter.

EU manufacturing industry may be hit hard

But at the same time, Huarong Futures pointed out that in order to ensure household electricity consumption, this 15% of the demand is reduced, a large proportion of which may come from industrial electricity and gas consumption, which will have a great impact on the EU's manufacturing sector, especially Germany and Italy.

The data show that the ways of direct industrial consumption of natural gas generally include: 1) heating (such as blast furnace), 2) chemical manufacturing, and 3) indirect use of electricity generated by natural gas plants. In terms of natural gas consumption in each industrial sector after value added adjustment, non-metallic minerals (including manufacturing such as glass, ceramics and concrete) are at the top of the chart.

Huarong Futures also specifically talked about the impact on the non-ferrous metals industry, pointing out that rising power costs are affecting the supply of copper, aluminum and zinc in the non-ferrous metals industry.

The non-ferrous metals industry is characterized by very high electrical intensity, which is as high as 40% of the production cost under normal electricity prices. according to Wood Mackenzie data, it takes about 15 megawatts of electricity to produce a ton of electrolytic aluminum, which is nearly 40 times that of copper.

Electrolytic aluminumSince October 2021, the European Union has lost nearly half of its electrolytic aluminum production capacity (about 1 million tons). From October 2021 to the end of August this year, the production reduction caused by the energy crisis in Europe and America has reached 1.48 million tons per year, of which 1.18 million tons per year in Europe and 304000 tons per year in the United States.

ZincWith the rise of electricity prices in Europe, electricity accounts for more than 60% of the cost of zinc smelting in Europe. At present, all nine electrolytic zinc smelters in the European Union have been seriously affected by the power crisis, and many smelters have reduced production or completely stopped production. According to public statistics, 760000 tons of production capacity has been suspended, equivalent to 45 per cent of total EU production.

For copper, so far, copper producers have been less affected by the crisis than zinc and aluminium smelters. Overall, the impact of the European energy crisis on copper is relatively small, coupled with the scarcity of copper resources, so its supply bottleneck is often reflected in the upstream mining link.

What other varieties may be affected?

In addition to the above mentionedNatural gas itself, non-ferrous metals (aluminum, zinc and copper)In addition, by combing a number of brokerage research reports, the following varieties may also be affected.

1. Coal-alternative demand or boost coal prices

Open source securities point out that alternative demand will provide upward momentum in coal prices.

According to its estimates, the average EU natural gas consumption from 2017 to 2021 is 16.9 EJ, and the reduced natural gas consumption is expected to be replaced by coal. It is expected that Europe will reduce natural gas demand by about 22.017 million tons from September to December in 2022, and will increase coal demand by 66 million tons in 2023.

2. Chemical products-production capacity + cost advantage.

Electricity prices in Europe soar, production costs of some chemicals soar, production capacity is limited, and domestic chemical companies ownCapacity + cost advantage.

According to the statistics of Huafu Securities, the cost advantages of nitrogen fertilizer, phosphate fertilizer, potash fertilizer, titanium dioxide, inorganic salt, soda ash, chlor-alkali, tires, spandex and carbon fiber of chemical fiber are the most obvious.

Guojin Securities said that we can focus on the varieties with relatively high production capacity in Europe. Europe accounts for 50 per cent, 43 per cent, 36 per cent, 34 per cent, 28 per cent, 27 per cent, 27 per cent and 26 per cent of global production of chemicals such as vitamin A, potassium chloride, vitamin E, formic acid, MDI, TDI, methionine and propylene oxide.

3 、 LNG

Huatai pointed out that if Beixi completely stops its gas supply, Europe is expected to use seaborne LNG carriers to seek alternative countries to purchase natural gas (such as the United States, Algeria, Qatar, etc.), which will be good for LNG transport market demand and push up LNG rates.

Zhongtai Securities pointed out that the European energy crisis, guard against stagflation demand shrinking and European manufacturing energy / raw material costs rising, delivery capacity decline, tap China's high-end equipment import replacement opportunities. Can pay attention to: 1) Natural gas equipment: LNG receiving station / gasification plant equipment (discharge arm, compressor, storage tank and LNG tank truck), LNG ship, LNG tank.

2) the European manufacturing industry may accelerate the search for capacity transfer solutions, and China is expected to undertake a larger part of the industrial chain transfer by virtue of its cost and supply chain advantages. SKF, Danobart, Volkswagen, BASF and other manufacturing enterprises have expanded production in China, and equipment manufacturing technology in related fields is expected to improve.

Edit / somer