Frasers Property Limited (SGX:TQ5), is not the largest company out there, but it had a relatively subdued couple of weeks in terms of changes in share price, which continued to float around the range of S$1.00 to S$1.09. However, is this the true valuation level of the mid-cap? Or is it currently undervalued, providing us with the opportunity to buy? Let's take a look at Frasers Property's outlook and value based on the most recent financial data to see if there are any catalysts for a price change.

Check out our latest analysis for Frasers Property

What's The Opportunity In Frasers Property?

According to my price multiple model, which makes a comparison between the company's price-to-earnings ratio and the industry average, the stock price seems to be justfied. I've used the price-to-earnings ratio in this instance because there's not enough visibility to forecast its cash flows. The stock's ratio of 5.97x is currently trading slightly below its industry peers' ratio of 9.43x, which means if you buy Frasers Property today, you'd be paying a decent price for it. And if you believe Frasers Property should be trading in this range, then there isn't much room for the share price to grow beyond the levels of other industry peers over the long-term. Furthermore, Frasers Property's share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. This may mean it is less likely for the stock to fall lower from natural market volatility, which suggests less opportunities to buy moving forward.

What does the future of Frasers Property look like?

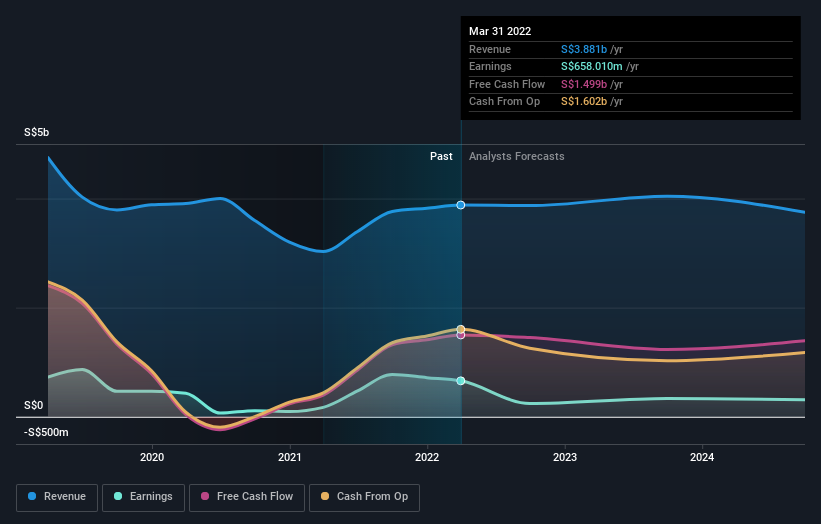

SGX:TQ5 Earnings and Revenue Growth September 27th 2022

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it's the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Though in the case of Frasers Property, it is expected to deliver a highly negative earnings growth in the next few years, which doesn't help build up its investment thesis. It appears that risk of future uncertainty is high, at least in the near term.

What This Means For You

Are you a shareholder? TQ5 seems priced close to industry peers right now, but given the uncertainty from negative returns in the future, this could be the right time to reduce the risk in your portfolio. Is your current exposure to the stock beneficial for your total portfolio? And is the opportunity cost of holding a negative-outlook stock too high? Before you make a decision on TQ5, take a look at whether its fundamentals have changed.

Are you a potential investor? If you've been keeping an eye on TQ5 for a while, now may not be the most optimal time to buy, given it is trading around industry price multiples. This means there's less benefit from mispricing. Furthermore, the negative growth outlook increases the risk of holding the stock. However, there are also other important factors we haven't considered today, which can help crystallize your views on TQ5 should the price fluctuate below the industry PE ratio.

So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. Our analysis shows 3 warning signs for Frasers Property (2 are concerning!) and we strongly recommend you look at these before investing.

If you are no longer interested in Frasers Property, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Frasers Property Limited(SGX: TQ5)並不是目前最大的公司,但就股價變化而言,其幾周表現相對疲軟,股價繼續在1.00新元至1.09新元的區間內浮動。但是,這是中盤股的真正估值水平嗎?還是它目前被低估了,爲我們提供了買入的機會?讓我們根據最新的財務數據來看看Frasers Property的前景和價值,看看價格變動是否有任何催化劑。

查看我們對弗雷澤地產的最新分析

弗雷澤物業的機會是甚麼?

根據我的價格倍數模型,該模型將公司的市盈率與行業平均水平進行了比較,股價似乎是合理的。在這種情況下,我之所以使用市盈率,是因爲可見性不足以預測其現金流。該股5.97倍的比率目前略低於其同業同行9.43倍的比率,這意味着如果你今天購買Frasers Property,你將爲此付出不錯的代價。而且,如果你認爲Frasers Property的交易價格應該在這個區間內,那麼從長遠來看,股價沒有超過其他行業同行水平的空間。此外,與其他市場相比,Frasers Property的股價似乎也相對穩定,其低貝塔值就表明了這一點。這可能意味着該股不太可能因市場的自然波動而下跌,這表明未來的買入機會減少了。

Frasers Property的未來是甚麼樣子?

新加坡交易所:TQ5 收益和收入增長 2022 年 9 月 27 日

尋求投資組合增長的投資者可能需要在購買公司股票之前考慮公司的前景。儘管價值投資者會爭辯說最重要的是相對於價格的內在價值,但更有說服力的投資論點是以低廉的價格獲得高增長潛力。儘管就Frasers Property而言,預計它將在未來幾年內實現高度負的收益增長,這無助於建立其投資論點。看來未來不確定性的風險很高,至少在短期內是如此。

這對你意味着甚麼

你是股東嗎? 目前,TQ5的價格似乎接近行業同行,但考慮到未來負回報帶來的不確定性,現在可能是降低投資組合風險的合適時機。您當前的股票敞口對您的總體投資組合有益嗎?持有前景不佳的股票的機會成本是否過高?在你對 TQ5 做出決定之前,先看看它的基本面是否發生了變化。

你是潛在的投資者嗎? 如果你關注TQ5已有一段時間了,那麼現在可能不是最佳的買入時機,因爲它的交易價格是行業價格倍數。這意味着錯誤定價帶來的好處較小。此外,負增長前景增加了持有該股的風險。但是,還有其他重要因素我們今天沒有考慮,如果價格波動低於行業市盈率,這些因素可以幫助你具體化對TQ5的看法。

因此,如果你想更深入地研究這隻股票,考慮它面臨的任何風險至關重要。我們的分析顯示 Frasers Property 的 3 個警告標誌 (2 個令人擔憂!)我們強烈建議您在投資之前先看看這些。

如果您對Frasers Property不再感興趣,可以使用我們的免費平臺查看我們其他50多隻具有高增長潛力的股票清單。

對這篇文章有反饋嗎?擔心內容嗎? 取得聯繫 直接和我們在一起。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St 的這篇文章本質上是籠統的。 我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。 它不構成買入或賣出任何股票的建議,也沒有考慮您的目標或財務狀況。我們的目標是爲您提供由基本面數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。簡而言之,華爾街在上述任何股票中都沒有頭寸。