Source: Zhitong Finance and Economics

Author: Liang Zhongrong

On September 22, a day destined to go down in the annals of Hong Kong stocks, the Hang Seng Index fell directly back to 2011, with 11 years of upward efforts to return directly to zero.

Comparing today's index into the historical dimension, the Hang Seng Index fell to a new low of 17965 points, while the Hang Seng Index hit a high of 31183 in February 2021, a cumulative decline of 42 per cent in a year and a half.

42% is considered an 8-magnitude earthquake, and its performance is the worst when compared to the world's major capital markets.

Source: Societe Generale Securities

Therefore, when the Hang Seng Index fell to an 11-year low, the market was cloudy, pessimism pervaded the Internet, the continued negative impact of the Fed's interest rate hikes in the future on the future, the economic trend of China and the United States on the stock market, and the factors of the emotional cycle are far from reaching the freezing point. these endless views seem to prove that Hong Kong stocks can continue to decline in the future.

However, these possibilities are not compared in the context of the five historical stock market crashes in Hong Kong stocks, nor do they see the dawn of bridging the gap in Sino-US relations, let alone follow the tide of economic, technological and social transformation in the world and China. Do not stand on the Lion Rock, do not stand on the top of the Great Wall, overlooking to September 21 may be the historical demarcation point between the history and the future of investing in Hong Kong stocks.

On September 19 alone, there were three things worth paying attention to: the staff of the US PCAOB began to examine the audit draft of US-listed Chinese stocks; in New York, State Councilor and Foreign Minister Wang Yi held discussions and exchanges with representatives of the National Committee on US-China Relations, the National Committee on US-China Trade, and the American Chamber of Commerce; and Wang Yi met in New York with former US Secretary of State Henry Kissinger, who bears witness to the revival of Sino-US relations.

History is constructed by countless fascinating small details, they witness the rise and fall of history, the rise and fall of the times, from the above many small details, we may peep into the corner of the grand narrative of the future.

In the world, high global inflation in 2022 and the risk of accelerated liquidity contraction may be vigilant. Us stocks and A stocks will be the main battlefields of global capital accumulation, and Hong Kong stocks with reasonable valuations may also hit bottom and usher in opportunities for recovery. The 98-year-old Munger began to copy the bottom of Chinese stocks, as evidenced by the fact that Goldman Sachs Group and Qiaoshui Fund opened a chariot to increase their holdings of Chinese stocks.

Former British Prime Minister Winston Churchill said: never waste a crisis!When Hong Kong stocks experience a fall from an all-time high of 33484 in 2018, many wealth has vanished and countless legendary funds have disappeared in the market, and standing on this is the starting point for more new wealth and legends.

1

Behind the new low of the Hang Seng Index

In history, there have been many stock market crashes in Hong Kong stocks, and the causes of the five stock crashes are very different.

From the macro point of view, it is mainly the increase of interest rates by the Federal Reserve and the weakening of liquidity in Hong Kong stocks.

The Federal Reserve raised interest rates overnight by 75bp, forcing Hong Kong, which implements the linked exchange rate system, to follow suit. The Hong Kong Monetary Authority raised the base rate by 75 basis points to 3.5%, effective immediately.

For the Hong Kong market, its trading capital is mainly foreign capital, the market is obviously affected by the US dollar and Sino-US relations, and the Hong Kong market is greatly affected by US dollar Taper or US dollar interest rate hikes. The Fed's interest rate hike and contraction table, the Fed's interest rate hike and contraction table will lead to a rising debt of overseas funds, and Hong Kong, as the financial center of Asia, will face a lot of hot money withdrawal.

On the domestic side, the domestic economic recovery in August is relatively optimistic, and the year-on-year growth rates of social retail and industrial value added are relatively excellent. At the same time, the continuation of MLF reduction means that the monetary policy of the people's Bank of China may tilt to the sound end, and the liquidity of Hong Kong stocks may improve or slow down.

The liquidity tension in the Hong Kong stock market caused the Hang Seng Index to fall 2.6 per cent to 17965.33 and hit a 10-year low. At one point, the Hang Seng Technology Index fell 3.5 per cent to 3606.66.

In terms of valuation system, the composition system of Hang Seng Index is dominated by domestic capital, but the pricing power of the market is in the hands of foreign investors, which makes it more vulnerable to the joint influence of A shares and US stocks than other markets.

It should be pointed out that the Hang Seng Index has a relatively high weight in finance, real estate and the Internet. Among them, finance and real estate were their big year in 2016 and 2017, when many sellers continued to describe the arrival of a new macro upward cycle. Therefore, at that stage, the performance of the Hang Seng Index is better than that of the CSI 300.

From 2018 to 2019, a large number of domestic Internet companies and 18A enterprises went to Hong Kong to list, which brought a round of Hong Kong stocks to play a new trend, and rebounded quickly after the fall of the index, and became an important component of the Hang Seng Index with the rise of weight.

But it also leaves a hidden danger.

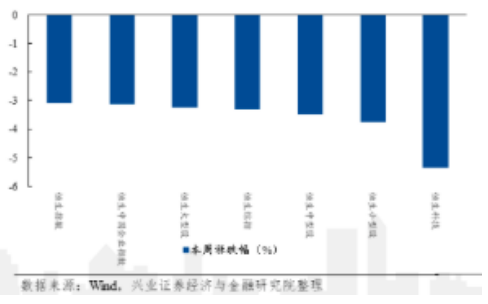

In the past year or so, the fundamentals of domestic consumption, Internet and pharmaceutical industry have been materially impacted one after another since the second half of 2021. With the decline of the real estate industry and the repeated impact of the epidemic on offline physical consumption, the Internet advertising and e-commerce industry has been greatly affected.

At the same time as in China, this round of rapid decline in Hong Kong stocks is mainly driven by track stocks such as real estate, technology, medicine and consumption, either as direct explosions as real estate and education stocks, or the collapse of crowded valuations or valuation bubbles such as technology, consumer and medicine, leading to a direct fall in the index.

At the same time, the widening valuation differences on AH shares prevailed in the market, and more views clearly said that the bottom of Hong Kong stocks had arrived, so a lot of funds repeatedly copied the bottom in the process. In the past six months of continuous bottoming, due to not getting a good profit effect, burst or emotional accumulation, resulting in a capital stampede, resulting in the Hang Seng Index has been slowly falling.

2

Is it a gold pit or a valuation trap?

Supply and demand theory, efficient market hypothesis, Merrill Lynch clock research, industry life cycle, capital asset pricing model, each theory contains a certain logic of the times, with a certain philosophical basis. To sum up, there are only three analysis methods: basic analysis, technical analysis and evolutionary analysis.

Combined with these three kinds of analysis, then, after adjusting for quite a long time, after setting an 11-year low, is the current time of Hong Kong stocks a gold pit or a valuation trap?

Here's our point: be careful, but don't waste this crisis.

We combine several aspects to verify the rationale of this view, which are: emotional cycle, Sino-US relations, corporate performance, buyback motivation.

Emotional cycle is more important than economic cycle, corporate profit cycle, credit cycle and so on. Because the ultimate goal of other cycles is to influence investors' views and emotions, there are peaks and troughs in the stock market.

From the perspective of the emotional cycle, we can see two dimensions: the extent of the decline in Hong Kong stocks and the performance of the financing side of IPO.

Historically, the last stock market crash in Hong Kong was in 2008, when it fell from a high of 26374.09 in May 2008 to 10676.29 at the end of October, halving 70 per cent. At the height of panic in September 2008, the Hang Seng index fell nearly 40 per cent. This time, the Hang Seng Index fell 40% in a year, the biggest drop in the past month was more than 10%, and even more than 20% in February-March, indicating that the mood has been effectively released after two surges in a year, and the decline is close to the historical extreme.

Source: HKEX, WIND

On the financing side, Hong Kong's share of Asian IPO fell to a 20-year low of just 7 per cent in the previous August. For comparison, the average share of Hong Kong in 1995-2021 was 26%.

Excessive trust, excessive infatuation, and excessive skepticism and complete mistrust of the future are two different extremes and undesirable. We must learn to accept and make use of this emotional cycle. The reversal at the bottom lies in the direction of these two extreme crossroads.

As far as Sino-US relations are concerned, in the preface, we have described such subtle changes. At the same time, oil stocks rebounded quickly, just like the rebound of oil stocks this year-even without the conflict between Russia and Ukraine, oil futures were negative in 2020 and superimposed on the reality that new energy could not quickly replace traditional energy. The same is true of analogies to Sino-US relations.

In terms of the fed's rate hike, us 10-year bond rates have risen to 3.69 per cent, the highest since 2011, putting downward pressure on the s & p 500. The risk-free interest rate of more than 3.6% is attractive to pension funds, so we are not worried that long-term bond interest rates will continue to rise disorderly.

In contrast, Hong Kong stocks southward funds, recently showed a relatively resolute bottom position increase situation.It can be found that domestic investors are still sticking to the trading thread of improved fundamentals, while foreign investors are focusing on the interpretation of the liquidity environment. As FOMC interest rates gradually approach 375-400bp, the liquidity deduction focused by foreign investors will gradually fade, while macro and micro fundamental recovery is expected to become the main driver of the more sustainable Hong Kong stock market.

In the long run, the height and sustainability of Hong Kong stock market repair still depends on the inflection point of China's economy and the degree of improvement.

From the perspective of A-shares represented by enterprises, in 2022, China News A-share enterprises showed strong profit resilience, the profit side exceeded market expectations, and the all-A net profit grew by nearly 2% (even excluding the financial industry. The second quarter also achieved a slight decline of 0.1% compared with the same period last year), and the revenue-profit scissors gap is expected to further close in the third and fourth quarters.

In terms of large enterprises, the quarterly income of 2022Q2 and BABA remained stable, with adjusted EBITA down 18% year-on-year, and non-GAAP net profit down 30% year-on-year, higher than market expectations; Tencent non-IFRS adjusted net profit was 28.1 billion yuan, down 17% from the same period last year, but also higher than market expectations, and was praised by the market as the beginning of Tencent's real bottom rebound.

The confidence of enterprises in themselves comes from the strength of repurchase in a depressed market.Tencent, BABA, Meituan and XIAOMI are not inferior in this respect. Take Tencent as an example. Tencent has bought back 17.7 billion Hong Kong dollars so far this year, ranking first among Hong Kong stock buybacks.

3

Conclusion

Judging from the valuation and investment of Hong Kong stocks, the fundamentals of China's economy and the degree of control over the COVID-19 epidemic are the fundamental factors for the stability of the RMB exchange rate and the attractiveness of Chinese assets.

Source: Societe Generale Securities

Zhongtai International pointed out that the current forecast PE of the Hang Seng Index and the MSCI China Index are 7.3 per cent and 36 per cent respectively over the past 15 years, with low valuations but not extreme levels. However, after the Fed raises interest rates, it can eliminate some of the uncertainties or bring a rebound window for Hong Kong stocks.

Everbright Securities believes that there is room for valuation repair in the Hong Kong stock market in the short term, and the long-term trend still depends on fundamentals. Overall, after the introduction of various economic support policies in August, economic fundamentals are expected to continue to recover in the third quarter. On the other hand, excluding the new economy, the PE and PB valuations of Hong Kong stocks are at historical lows since 2002, and the quantiles of valuation are also at low levels in recent years. With the basic landing of various negative factors, Hong Kong stocks have some room for valuation repair in the short term, and the rebound at the end of August is likely to continue.

In fact, from the dimension of time, it is overlooking along the long historical process of industrialization, the superposition of the deepening period of the fourth industrial revolution and the ebb period of the third industrial revolution, which is the background of the new economy. In this sense, the investment philosophy of Hong Kong stock investment, the wave of industrialization, the industrial revolution, or the Kondratiev cycle, should be the first macro factor to consider as an investment.

From 5G to new energy, from artificial intelligence to bioengineering, China's stable social system, perfect industrial chain, unified big market, huge engineering dividend, strong infrastructure construction capacity, millions of scientists and engineers, will establish China's competitiveness in the fourth industrial revolution.

In the past 70 years, the success and leadership of East Asian countries in the world, and the success of China's reform and opening up in the past 40 years, we believe that although there are doubts in the middle, the trend will not change. At present, we are reshaping the underlying logic of the economy. Adhering to reform and opening up is a national policy that will not be changed. The key to future success lies in whether the reform is more thorough and more resolute.

Edit / new