美联储的鹰派信号让本有望反弹的美股挣扎后重回两个多月低谷。

美联储的鹰派信号让本有望反弹的美股挣扎后重回两个多月低谷。The three major US stock indexes fell after the Fed raised interest rates, rose during Powell's press conference and fell again after the meeting, closing at a new low for at least two and a half months. Pan-European stock index ended six consecutive declines to get rid of more than two-month lows, defense stocks Rheinmetall rose more than 9 per cent, Russian stocks hit an one-month low, at one point fell nearly 10 per cent.

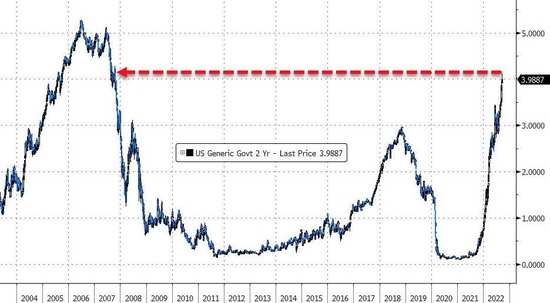

The yield on two-year US bonds rose above 4.0% in intraday trading for the first time since 2007, and the 10-year yield hit an 11-year high before falling.

The dollar index hit a 20-year high after two weeks, the euro hit a 20-year low and the pound hit a new low in 1985. Crude oil rose at least 2% in intraday trading before falling to a two-week low. Gold is out of its two-year trough.

The Fed's hawkish signal sent U. S. stocks back to a more than two-month low after struggling to rebound.

The Fed's hawkish signal sent U. S. stocks back to a more than two-month low after struggling to rebound.

The Fed is widely expected to continue to aggressively raise interest rates by 75 basis points this week, after three major indexes of US stocks rose in intraday trading ahead of the Fed's decision on Wednesday. Short-term US Treasuries, which are more sensitive to the outlook for interest rates, accelerated their decline, with yields continuing to hit record highs. The yield on two-year Treasuries rose above 4 per cent for the first time since 2007, and the dollar index hit its highest level since 2002 two weeks later.

At midday, the Fed announced its third consecutive 75 basis point rate hike as scheduled, and unexpectedly released a stronger hawkish tendency: Fed officials' median interest rate forecast for next year was 4.6%, higher than the previous market peak of 4.5%. Most officials expect to raise interest rates by another 125 basis points by the end of the year, putting the possibility of another 75 basis points in November on the table. After the announcement of the Fed's decision, the three major US stock indexes plunged in intraday trading and fell quickly. Two-year Treasury yields continued to hit 15-year highs, and the dollar index stabilized above 111.00 for the first time since 2002, and then fell back, but retained its intraday rally.

At a press conference after the meeting, Federal Reserve Chairman Powell reiterated that the annual meeting of central banks around the world at the end of last month said that it would be appropriate to hold on to raising interest rates until it was done. It would be appropriate to repeat what was said after the last meeting in July that interest rate increases would be slowed down "at some point in time". During the press conference, U. S. stocks rose, the Nasdaq and S & P refreshed their daily highs, up more than 1% during the day. But after the Powell conference, the US stock index returned to its downtrend and eventually fell to its lowest point since at least early July.

Commentators said that the Fed's bitmap is more hawkish than the market expected. On the one hand, it is possible to continue to raise interest rates aggressively by the end of this year; on the other hand, it is possible that most of the rate hike cycle will end more quickly. The market weighs on both sides, generally speaking, more hawkish signals prevail. The alternation of gains and losses in US stocks highlights investors' unease about the economic outlook and market uncertainty in a highly inflationary environment.

European stocks closed before the Fed's decision and dodged a bullet. After Putin delivered a speech to the nation for his first partial mobilization since World War II, European defense stocks soared, with German-listed Rheinmetall up more than 9%, helping European stocks rebound. The Russian stock index, which once fell more than 10 per cent on Tuesday due to signs of escalating conflict between Russia and Ukraine, continued to refresh its low for more than a month, falling nearly 10 per cent at the start of the day and erasing most of its losses by the close.

Among commodities, international crude oil, which fell on Tuesday, rebounded in intraday trading. Russia's intention to strengthen its military deployment made the geopolitical situation even more tense. Crude oil rose at least 2% in intraday trading. The U.S. Department of Energy announced that last week, crude oil stocks rose for three weeks in a row and the four-week average for gasoline demand hit a new low since 1997. Crude oil fell at least 1% on the day, and finally continued to refresh its two-week low. Gold, which has been falling for several days, has come out of its trough for more than two years, and the rise has expanded after the Federal Reserve raised interest rates.

After the Federal Reserve raised interest rates, the three major US stock indexes turned lower during the Powell press conference, and then fell to a new low in at least two and a half months.

The three major US stock indexes collectively opened high. when the morning session was high, the Dow Jones Industrial average was up more than 310 points, or just over 1%. The S & P 500 was up more than 0.8% in early trading, and the NASDAQ composite index was up more than 0.8% at midday. After the Fed's decision was announced, the three major stock indexes all turned down. at one point, the Dow fell more than 260 points, and the S & P fell more than 0.8%, and the Nasdaq fell 0.9%. It rose after the Powell press conference. During the press conference, the Dow approached intraday highs. When the S & P and Nasdaq refreshed their daily highs, they rose more than 1.3% and nearly 1.7% respectively. After the Powell press conference, they fell again and later refreshed their daily lows. The Dow fell more than 500 points, and the intraday declines of the S & P and Nasdaq both widened to more than 1%.

In the endThe three major indexes, which ended two consecutive days of losses on Monday, closed down for the second day in a row, hitting at least two-and-a-half-month closing lows and the fourth day of the last five trading days. The Nasdaq closed down 1.79% at 11220.19 points, the lowest since July 1.S & p closed down 1.71% at 3789.93, its lowest close since June 30th. The Dow closed down 522. 45 points, or 1.7%, to 30183.78, the lowest since June 17.

Russell 2000, a small-cap stock index dominated by value stocks, closed down 1.42%, hitting its lowest level since July 18 for two days in a row. The tech-heavy Nasdaq 100 index closed down 1.8 per cent to its lowest level since July 1, while Russell 2000 turned lower after the Fed's decision and Powell's press conference.

Trend of major US stock indexes from Tuesday to Wednesday

The S & P 500 sectors collectively closed down for two days in a row, with the exception of essential consumer goods which fell more than 0.3 per cent, all sectors fell at least more than 1 per cent, while Tesla, Inc. and Amazon.Com Inc's consumer discretionary goods, Meta's communications services, materials and finance all fell more than 2 per cent.

Most leading technology stocks have fallen for two days in a row.Tesla, Inc. closed down 2.6% and continued to fall off Monday's highest close since Aug. 15. Among the six major technology stocks in FAANMG, Amazon.Com Inc closed down 3% to its lowest level since July 26. Facebook Inc's parent company Meta closed down 2.7%, the lowest since January 7, 2019. Nai fell nearly 2.5% and continued to fall from Monday's high since August 18. Apple Inc, which has risen for two consecutive days, closed down 2%, Alphabet Inc-CL C's parent company Alphabet fell 1.8%, and Microsoft Corp fell more than 1.4%. It fell for six consecutive days to its lowest level since March 31 last year.

Most of the hot Chinese stocks continue to fall.ETF KWEB and CQQQ closed down nearly 4.8 per cent and 3.6 per cent, respectively. The Nasdaq Golden Dragon China Index closed down 5.9%. The four components of the Nasdaq 100th index, including Duoduo, JD.com, Baidu, Inc. and NetEase, Inc, all fell more than 5 per cent, leading the decline, second only to Marriott International, which closed down more than 5.6 per cent. Among the other stocks, XPeng fell by more than 11%, NIO Inc. Motor by 10%, Yatsen by more than 9%, Dada Nexus Limited by about 9%, Li Auto Inc. by nearly 9%, Trip.com by more than 8%, New Oriental Education & Technology by more than 5%, Alibaba by nearly 5%, Tencent Powder by more than 3%, Zhangmen Education by more than 50%, Kaixin Auto by 20%, JinkoSolar by more than 2%, and Canadian Solar by about 0.8%.

For European stocks, the pan-European stock index, which has been down for six days in a row, rebounded. The European Stoxx 600 index has shrugged off its closing low since July 5, set on Tuesday. Among the sectors, only tourism, which fell 1.9%, and banks, which fell 0.4%, closed lower on Wednesday. The decline in bank stocks sent the Spanish stock index down alone among European countries, led by the utility sector, which rose more than 1.8%. The industrial sector and oil and gas, which benefited from the intraday rebound in crude oil, rose nearly 1.6%. Defence stocks generally soared, with Frankfurt-listed Rheinmetall up 9.3 per cent, Milan-listed Leonardo 5.5 per cent, London-listed BAE Systems 4.3 per cent and Paris-listed Thales nearly 4 per cent.

Russia's benchmark stock index, the MOEX index, fell nearly 10 per cent early Wednesday, approaching its biggest drop since the conflict between Russia and Ukraine in February, when it fell nearly 11 per cent on Tuesday, before closing down 3.83 per cent, the lowest since early August.

The yield on 2-year US Treasuries rose above 4.0% in intraday trading for the first time since 2007. The 10-year yield hit an 11-year high and then fell.

European government bond prices did not continue to fall collectively, some rebounded in intraday trading and yields fell, but short-term bond yields all kept rising and continued to hit record highs. The yield on UK 10-year benchmark government bonds closed at 3.31%, up 2 basis points on the day, setting a new intraday high in 2011 for two consecutive days. The yield on 2-year gilts closed at 3.34% and rose 7 basis points on the day, setting an intraday high of 2008 for two consecutive days. The yield on 10-year German bunds closed at 1.89%, down 3 basis points on the day, away from Tuesday's high since December 2013. The yield on the two-year German bond closed at 1.73%, up 4 basis points in the day, while U. S. stocks rose above 1.76% in early trading, hitting a 2011 high for five consecutive days.

The yield on the benchmark US 10-year Treasury note was measured at 3.52% in early trading in Europe, down about 4 basis points in the day, and US stocks erased all their declines in early trading. After the announcement of the Fed's decision at midday, US stocks rose above 3.6% in the short term and once tested 3.64%. After breaking 3.6% in midday on Tuesday, it reached its highest level since April 2011 for the fourth day in a row, and then quickly fell below 3.60% and continued to decline. At one point in late trading, US stocks approached 3.50% to refresh their daily lows, closing at 3.53%, down 3 basis points on the day.

Before the Fed announced the decision, the yield on two-year Treasuries, which is more sensitive to the outlook for interest rates, rose above 4.0% in early trading, breaking through this mark for the first time since October 2007. After the announcement of the Fed resolution, it broke above 4.10%. It hit a new high since October 2007 for three consecutive days and hit a nearly 15-year high for nine consecutive days, rising nearly 13 basis points in the day, and then fell back. U. S. stocks closed at 4.05%. It rose by about 8 basis points in a day.

The trend of 2-year Treasury yield since 2004

Widening spread between 2-year and 10-year US Treasury yields, an important early warning indicator of recessionIt reached-52 basis points in intraday trading, and the level of yield upside down was close to the highest level since Volcker became the Fed in 1982.

Edit / ruby