Source: Securities firm Chinese author: Chengzhen

Editor's note:There are many differences between mature markets and local emerging markets, including: (1) there are strong class actions in markets such as the United States, which are highly responsible for issuers and intermediaries; (2) the structure of investors in markets such as the United States is different. Institutional investors account for more than 60% of the market capitalization for a long time. 3. The professional ability and reputation restraint mechanism of investment banks are very strong, and the interests are highly bound to customers. 4. The professional standard of intermediary institutions such as accountants and lawyers is relatively high.

The word delisting, for the A-share market, is like a "familiar stranger", although familiar but not common.

Let's take a look at a set of data:

According to WFE data, the cumulative value of delisting of listed companies worldwide reached 21280 from 2007 to October 2018, with a cumulative value of 16299 exceeding IPO.

Let's take a look at the US stock market, the largest stock market in the world:

According to WRDS data, between 1980 and 2017, the total number of companies still listed and delisted in the US stock market reached 26505. Excluding 6898 companies with unknown survival status, 5424 companies are still listed, accounting for 28 per cent, and 14183 companies have been delisted, accounting for 72 per cent.

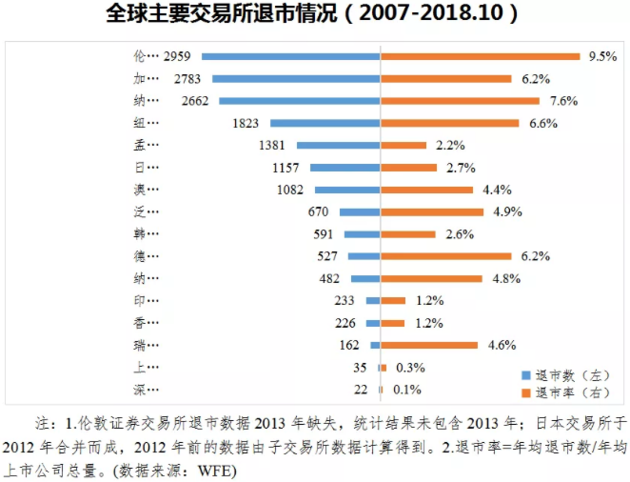

Let's take a look at the delisting rates of capital markets around the world:

The number and rate of delisting companies in mature capital markets are generally higher than those in emerging markets. The cumulative number of delisting companies in the LSE, TMX Group of Canada and NASDAQ all exceeds 2500. The delisting rates of LSE and NASDAQ (USA) are 9.5% and 7.6% respectively, far higher than those of other exchanges.

The delisting rates of the Shanghai and Shenzhen exchanges are only 0.3 per cent and 0.1 per cent respectively.

Delisting system is one of the basic systems for the healthy development of the capital market. In the mature capital market, delisting of listed companies has become a normal phenomenon. On November 5, Xi Jinping announced that he would set up a Science and Technology Innovation Board and viewpoint registration system on the Shanghai Stock Exchange. The policy details are waiting to be issued, and the market has high hopes for it. Close to the regulatory sources revealed that the construction of Science and Technology Innovation Board delisting system should learn from the experience of international mature markets: first, to set up multi-dimensional compulsory delisting standards, second, to establish strict delisting procedures, and third, to improve the investor protection system.

The number of delisting of global listed companies far exceeds the number of listed companies.

According to WFE data, from 2007 to October 2018, the total number of delisted companies in the world reached 21280, and the total number of global IPO reached 16299, which is larger than the scale of IPO.

From the perspective of annual distribution, except for 2015, the annual number of IPO in other years is less than the number of delisting. In 2015, the global issuance market warmed up, and the scale of delisting fell to the lowest in the sample period. the number of IPO slightly exceeded the number of delisting, but only 51 more than the number of delisting. The overall volatility of the number of delisting is less than the number of IPO, and the scale of global delisting is relatively stable relative to the change of the size of the issuing market.

In terms of the number of delisting companies, the number of delisting companies on the LSE reached 2959, ranking first on the list. In addition, the number of delisting of Canada's TMX Group and NASDAQ (USA) is more than 2500; the number of delisting of New York Stock Exchange, Mumbai Stock Exchange, Japanese Stock Exchange and Australian Stock Exchange is also more than 1000; and the delisting of pan-European and other exchanges is smaller, less than 1000.

In terms of delisting rate, the delisting rate of the LSE is as high as 9.5%, far higher than that of other exchanges. Nasdaq (US), NYSE, Canada's TMX Group and Deutsche B ö rse all have delisting rates above 6 per cent. Delisting rates for Euronext, NASDAQ (Nordic), Swiss Exchange and Australian Stock Exchange are between 4% and 5%. Delisting rates on other exchanges are less than 4 per cent.

From the delisting of each sector of the exchange, among the eight exchanges that disclose the delisting of each sector, the number and rate of delisting of the mature market main board are generally higher than those of emerging markets; the number of delisting of the small and medium-sized board TSX of the Canadian TMX Group is far higher than that of other exchanges; comparing the delisting of the two sectors, the delisting rates of NASDAQ (Nordic), pan-European gem, HKEx, JASDAQ and MOTHERS are higher than their respective main boards.

More than 70% of companies in the US stock market are delisted.

Between 1980 and 2017, the total number of companies still listed and delisted reached 26505, according to WRDS. After deducting 6898 companies with unknown survival status, a total of 19607 listed companies were included in the overall analysis. Among them, 5424 companies are still listed, accounting for 28%, and 14183 companies have been delisted, accounting for 72%.

Among the delisting samples, 7234 companies have access to listing time, accounting for about 51 per cent of the total number of delisted companies. Data show that of the 7234 companies mentioned above, as many as 2862 companies were delisted within five years of listing, accounting for 39.6% of all delisted companies. Among them, the largest number of companies are delisted in the third and fourth years after listing, with more than 800 companies per year.

The situation of delisting quickly after listing is not limited to the Nasdaq market, where technological innovation companies are concentrated. In a market for more mature companies, such as the New York Stock Exchange, the situation is similar. Data show that the delisting peaks on both exchanges are in the fourth year after listing: 13% of delisted companies on NASDAQ are delisted in the fourth year, compared with 10% on the New York Stock Exchange.

From the perspective of delisting reasons, mergers and acquisitions, financial problems and stock prices are the three axes of delisting. Data show that 56% of delisted companies are delisted because of mergers and acquisitions, 15% are delisted due to financial problems, and 9% are delisted due to low share prices.

Delisting standards vary from market to market.

Comparing the delisting mechanisms of the New York Stock Exchange, NASDAQ and the Stock Exchange of Hong Kong, we can find a lot in common. In terms of delisting system, the delisting standards set by the three exchanges include quantitative standards and qualitative standards. moreover, the quantitative standards of the New York Stock Exchange and NASDAQ are divided into several sets of standards, such as the number of shareholders, "market capitalization + operating income" and so on. this gives the exchange greater discretion and flexibility to ensure the quality of listed companies and safeguard the rights and interests of investors from various angles.

In addition, the delisting process of the three exchanges is clear and perfect, and the listed companies are given the right of appeal, and the supporting investor protection system is complete and mature. The United States and Hong Kong have strict laws and regulations and systematic investor protection institutions. Moreover, the class action system in the United States and the quasi-judicial protection in Hong Kong have also strongly safeguarded the rights and interests of investors.

1. New York Stock Exchange

The delisting standard of the New York Stock Exchange has few provisions in terms of voluntary delisting, mainly focusing on compulsory delisting. The criteria for compulsory delisting can be divided into three categories: transaction indicators, sustainable operating capacity indicators and compliance indicators. Specifically refers to:

One is whether there is active trading, which requires that the stock trading of listed companies must meet certain liquidity standards, including the number of shareholders, public shareholding, trading volume, market value, stock price and so on.

The second is whether it has the ability of sustainable operation, which requires listed companies to have the ability of sustainable operation. The indicators mainly include whether the main activities are stopped, whether there is bankruptcy liquidation, unable to repay debts, lack of financial operation ability and so on.

Third, whether to meet the compliance requirements, such indicators require listed companies to comply with the requirements of corporate governance, information disclosure and so on. the indicators mainly include whether the annual report is not disclosed on time, whether it violates the listing agreement, whether it violates the public interest, whether an audit committee is convened, whether it is issued a non-standard audit opinion, and so on.

2. NASDAQ

Nasdaq Stock Market is the largest listing place of Nasdaq in the United States, with three market segments: global selected Market (NASDAQ GS), Global Market (NASDAQ GM) and Capital Market (NASDAQ CM). The global selected market has the highest listing standard, which mainly attracts the listing resources of large and high-quality enterprises; the global market belongs to the middle level, mainly serving medium-sized enterprises; the capital market is the earliest market level established at the early stage of the establishment of NASDAQ, and the listing standard is the lowest, mainly serving small and micro enterprises.

According to the characteristics of different markets, NASDAQ has formulated different standards for continuous listing:

First, trading indicators, including the number of shares held by the public, the market value of shares, the number of market makers, and so on.

Second, continuing operation indicators, including income, asset scale, shareholders' rights and interests, etc.

Third, compliance indicators, including information disclosure, independent directors, audit committee and other requirements.

Among them, the first two categories are quantitative indicators, and the latter are qualitative indicators, which are mainly regulated from the internal governance of the company. Delisting is triggered when the listed company does not meet the conditions for continuous listing. However, NASDAQ in the implementation of the delisting system is not immutable, in 2001, 2008 and other market slump, NASDAQ suspended the implementation of the minimum market value and minimum quotation indicators.

From past experience, the delisting process of the company is relatively smooth. On the one hand, the NYSE effectively communicates with the market through press releases and websites, so that investors will not be misled by unofficial news. On the other hand, investors in the US market are mainly institutions, and their investment concepts are more mature. They can rationally see that the valuations of companies that touch delisting risks usually continue to decline, and there is not much market speculation. Under the influence of these two factors, the market is easy to accept that the company is forced to delist, the motivation of the stakeholders to resist delisting is small, and the delisting mechanism runs relatively smoothly.

3. Stock Exchange of Hong Kong

According to different delisting intentions, the HKEx can be divided into compulsory delisting and voluntary delisting.

There are three rules for compulsory delisting:

The number of securities held by the public is less than 25% of the total number of shares issued

The Exchange considers that the issuer does not have sufficient business operations or assets of considerable value (financial difficulties seriously impair the ability of the issuer to continue to carry on business or the issuer's liabilities are higher than the value of its assets.

The exchange believes that the issuer or its business is no longer suitable for listing.

There are also three rules for voluntary delisting:

Approved by the shareholders' general meeting to be listed on other recognized public stock exchanges

Withdraw the listing status with the consent of the shareholders' meeting.

The issuer is fully offered for acquisition or privatized.

Three conjectures on the Construction of Science and Technology Innovation Board's delisting system

Delisting system is one of the basic systems for the healthy development of capital market. In mature capital markets, delisting of listed companies has become a normal phenomenon, and exchanges in various markets have greater discretion and flexibility in deciding on delisting of listed companies. Delisting criteria are not limited to whether listed companies violate the rules of continuous listing.

Close to the regulatory sources revealed that the construction of Science and Technology Innovation Board delisting system should learn from the experience of international mature markets and carry out system construction from the following three angles:

1. Set up multi-dimensional delisting standards

Science and Technology Innovation Board should set up multi-dimensional and omni-directional criteria for compulsory delisting:

First, it is necessary to improve the indicators of sustainable operation. At present, the existing compulsory delisting criteria of A shares pay attention to the index of "whether the net profit is losing for three consecutive years", which is consistent with the current IPO listing standards emphasizing net profit and other accounting indicators. With the diversification of Science and Technology Innovation Board listing standards Delisting criteria should also be set up from the aspects of "market capitalization + operating income", "market capitalization + operating income + operating cash flow", sustainable net profit and so on.

The second is to improve liquidity indicators, give delisting warnings to listed companies with inactive trading, and give timely risk tips to investors.

The third is to improve the compliance indicators, in addition to major illegal acts, for some illegal business activities, but also the relevant listed companies should be forced to delist in accordance with the delisting standards in time.

2. Set up strict delisting procedures

Science and Technology Innovation Board should establish rigorous and standardized delisting decision-making procedures and delisting implementation procedures:

First, it is necessary to set up a decision-making mechanism of the delisting committee to consider whether the behavior of listed companies seriously affects the listing status and whether they should implement major illegal delisting, so as to make independent professional judgments and form audit opinions. Clarify the relevant review decisions, such as the time limit for review, the time limit for making delisting decisions, etc.

The second is to give reasonable relief channels and relief means to the parties, mainly the listed companies that are about to be delisted to apply for hearing, written statement and defense, request review and other rights, safeguard their due process protection rights, and protect the basic rights of the parties.

Third, it is necessary to clarify the important relevant links in the process of delisting, that is, suspension, delisting risk warning, suspension of listing and termination of listing.

3. Improve the investor protection system

The investor protection in the process of delisting of Science and Technology Innovation Board Company should be strengthened:

The first is to set up a thorough and effective investor protection mechanism. Build a systematic compensation relief system and compensation fund for small and medium-sized investors, when there is a delisting event, give some compensation to its investors within the scope of protection, in order to reduce the economic losses suffered by investors.

The second is to improve the supporting legal system, if investors are still not satisfied with the existing measures, they can also seek legal protection to protect their own rights and interests. In the long run, companies that disturb market order and continue to deteriorate performance indicators will be cleared out of the market, purify the market environment, improve the mechanism of survival of the fittest in the market, urge companies to standardize their operation, and really improve the quality of listed companies, is the fundamental policy to safeguard the rights and interests of investors.