/ she Qingqi / tr. by Phil Newell)

The deals of Wanda, Sunac and R & F have recently been targeted by the big three rating agencies.

Fitch released a report on July 23 that R & F Real Estate spent 19.906 billion yuan to take over Wanda's commercial hotel assets, pushing up its leverage and putting its bonds on negative watch.

In the secondary market, R & F real estate Hong Kong stocks fell 1.47%, opened high and opened low on the first trading day after the asset acquisition was announced, and now closed down for three consecutive trading days.

Fitch listed R & F as a negative watch

For R & F property to join, the international rating agencies Moody's Corporation and Fitch have recently given the latest views.Moody's Corporation said in a report last week that the acquisition had a negative impact on R & F, but would not change its rating outlook.

Zeng Qixian, vice president of Moody's Corporation, said: "if the proposed acquisition is successfully completed, it will have a negative credit impact on R & F, as part of the transaction funds will be supported by debt financing, which will delay R & F's leverage reduction process." However, we believe that the company is likely to control investment in land, thus extending its deleveraging measures until 2018. "

Compared with Moody's assessment of R & F, Fitch's view is more negative.

On July 23, Fitch placed R & F's long-term foreign currency issuer rating, priority unsecured rating and all outstanding bonds of its subsidiaries as "BB" as a negative review.

Fitch believes that the company's announcement of a Rmb20 billion acquisition of hotel assets owned by Wanda Commercial Real Estate is expected to push up the stock's overall debt level and bring its net debt to adjusted inventory close to the Fitch threshold of 60 per cent. and asset acquisitions by the stock will slow the company's process of deleveraging.

Interestingly, while R & F was included in the negative review, Fitch also published a report saying that the asset sale would help improve Wanda's commercial financial position.

Fitch's view was the opposite when S & P put Wanda Business on a negative watch, arguing that the deal had a positive impact on Wanda's outlook. According to Fitch's latest statement, the previous negative outlook for Wanda was mainly due to its high leverage ratio. Once the deal is completed, Fitch's outlook for Wanda is likely to change from negative to stable. Specifically, the deal will reduce Wanda's net debt from 124 billion to 41 billion.

Deal with "40% discount"

On July 19th, R & F officially announced that it would take over 76 hotel asset packages owned by Wanda (which increased to 77 when the contract was officially signed), with a transaction consideration of 19.906 billion yuan.

What has attracted the most market attention is the price of the deal. In the previous contract with Wanda, 76 hotel assets cost as much as 33.595 billion yuan, while the consideration fell to less than 20 billion when R & F Real Estate took over. Leaving aside what happened at the scene, this acquisition, which is only 60% of the original consideration, is really a good deal.

The hotel business acquired this time is precisely the deficiency of R & F real estate before. R & F Real Estate's results show that the hotel business has continued to lose money in the past five years.

CICC has previously analyzed that R & F's core business has always been real estate development, but has always been dragged down by the company's sideline. The company's hotel operation and other divisions continued the dilemma of net loss in 2016, with a total net loss of 730 million yuan, compared with 670 million yuan in 2015.

According to the announcement, R & F Real Estate has taken over core hotel assets such as Sheraton, Crowne Holiday, Westin, Hilton and Amy, with a total floor area of 328.63 square meters and 23202 rooms.

Moody's Corporation said that after the completion of the deal, R & F Real Estate's hotel portfolio (in operation and under construction) will increase to about 100. At present, R & F Real Estate has only 14 hotels in operation.

And how about the profitability of these 77 hotels in Wanda? According to VANDA HOTEL Development 2016 Annual report, VANDA HOTEL's development income in 2016 was 387 million Hong Kong dollars, down 82.8 percent from the same period last year, while the net loss was 60.663 million Hong Kong dollars, down 76.9 percent from the same period last year.

"the periodicity of hotel business is different from that of real estate development. Moody's Corporation said, "this acquisition will make R & F's business more diversified and benefit from it." "

The stock of bonds is twice that of financing.

According to Moody's Corporation's calculations, if the acquisition is completed successfully, R & F's debt leverage ratio, as measured by the income / adjusted debt ratio, will rise from 42 per cent at the end of 2016 to 50 per cent and 60 per cent by 2018. Moody's Corporation had expected R & F's income / adjusted debt ratio to rise to 60 per cent by the end of 2018.

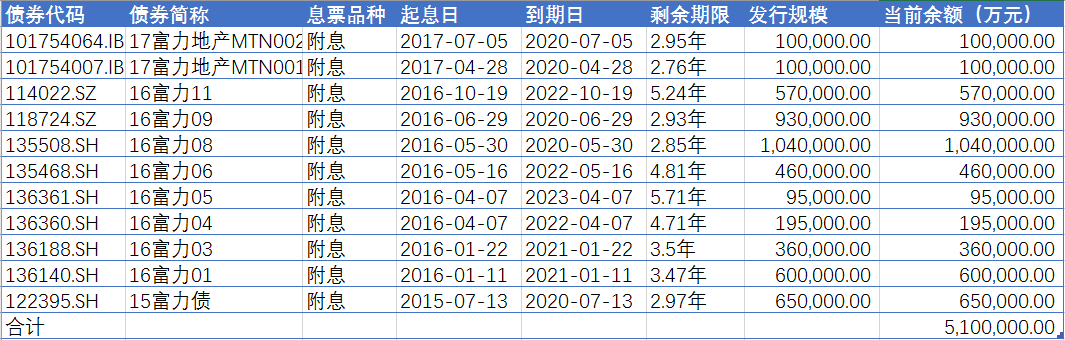

According to the public information, the first Financial and Economic reporter found that the total amount of bonds publicly issued by R & F Real Estate is 51 billion yuan. By the end of the first quarter, the balance of long-term loans was 43.978 billion yuan. Unlike Sunac China, who is highly dependent on bank loans, R & F property relies mainly on bond issuance for financing in terms of debt structure, and the stock of bonds is about twice that of Sunac China.

Of the 51 billion bonds, 49 billion are corporate bonds issued on the Shanghai and Shenzhen exchanges, mainly in the first three quarters of 2016.

Domestic stock bonds of R & F real estate

However, after the tightening of corporate bond issuance by real estate enterprises at the end of 2016, it is significantly more difficult for real estate enterprises to issue corporate bonds.

As of July 24, R & F Real Estate, a major issuer of bonds last year, has not been able to issue corporate bonds so far this year, issuing only 2 billion medium-term notes in the interbank bond market, which has relatively relaxed vetting conditions. In terms of foreign debt, R & F Real Estate also issued an additional $460 million in priority notes on January 12 this year, bringing the total balance of foreign debt to $7.25, which is due in 2022.

In the case of tight financing, can R & F make the relevant payment to Wanda in time? Although bond financing has decreased significantly since the beginning of this year, according to China Integrity's previous report, as of the end of the first quarter, R & F Real Estate still has 82.9 billion yuan of bank credit. In addition, the R & F real estate quarterly report shows that the company's book currency balance is 404.9 trillion.

For paying Wanda for the cash flow needed for asset acquisitions, Moody's Corporation expects R & F to have sufficient liquidity to support the deal. As of June 2017, R & F held the same amount of cash as it did at the end of 2016. Contract sales at R & F rose 30 per cent year-on-year to 38.8 billion yuan in the first half of 2017, making it easy to meet its full-year target of 73 billion yuan.

CICC also released a report on the 24th that R & F real estate's contract sales are expected to exceed 80 billion yuan in 2017. In the second half of 2017, 47% of its marketable resources of more than 100 billion yuan are new properties, and contract sales are expected to increase in the second half of the year.

But CICC also analyzed that R & F's balance sheet could come under further pressure. "We expect the net debt ratio to further increase the company's debt maturity of 33.7 billion yuan this year; at the same time, regardless of further acquisition of land for the rest of this year, the company's operating activities will create a cash gap of 13 billion yuan. The company will ease the liquidity pressure through financing instruments such as 46 billion yuan in cash and development loans, US dollar preferred notes and medium-term notes prepared at the end of last year. "