Authors: Zhong Zhengsheng, Xia Natural

I. overseas policy tracking

The health care reform bill basically ends, and Trump's reform process is blocked again.

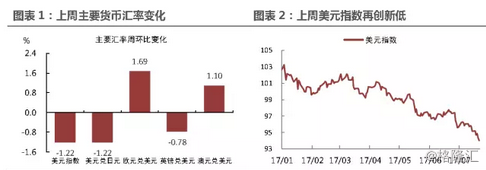

On Monday, local time, Trump's new health care bill suffered another setback, with senators Mike Lee and Jerry Moran both announcing through twitter that they did not support the current health care reform bill. Together with the previous Susan Collins and Rand Paul, a total of four Republican senators expressed opposition. According to the regulations, if Senate Republicans want the motion to proceed properly, they must get 50 of the 52 votes in the party, so the new bill has basically been rejected. On Monday night, Senate Majority Leader Mitch McConnell announced that Republicans would abandon the use of the new health care law to immediately replace Obamacare. Affected by the news, the dollar index fell 0.5% that day, and the euro continued to ferment in the second half of the week, and the euro rose sharply due to Draghi's speech, pushing the dollar index down 1.2% for the whole week, falling below the 94 mark (chart 2).

The defeat is a blow to Trump because the health care bill is the first major reform he is committed to, and the White House has revised manuscripts several times for this plan. If the health care reform is passed, confidence in Trump will be greatly boosted and is expected to reverse the recent market pessimism about him. However, health care reform has basically come to an end, and it is difficult to implement plans such as infrastructure and tax cuts in the later stage. Now, Trump has instead called for bipartisanship to vote to repeal Obamacare and continue to work on a new health care law within a two-year buffer.Predictably, he will shelve health care reform for the time being and focus on tax reform, but if tax reform continues to suffer, the market will completely lose confidence in Trump, and "no matter how great America is" will become empty talk.

The Bank of Japan is on hold and will continue to ease this year.

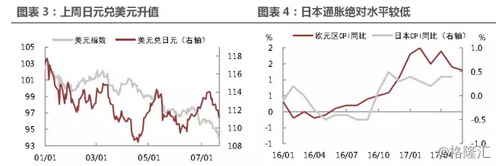

At last Thursday's monetary policy meeting, the Bank of Japan left short-term interest rates unchanged at-0.1 per cent, target interest rates for 10-year Treasury yields at zero, and annual bond purchases at 80 trillion. The BoJ cut its inflation forecast again, cutting its inflation expectations for 2017 and 2018 to 1.1 per cent and 1.5 per cent from 1.4 per cent and 1.7 per cent respectively. But it raised the growth rate of GDP in 2017, from 1.6 per cent to 1.8 per cent. The decision was in line with expectations, and the yen fell slightly after the news, but rose throughout the week on the weakness of the dollar (chart 3).

Although inflation in Japan has risen continuously this year, the absolute value is on the low side, currently only 0.4% (chart 4), which is also an important factor restricting the Bank of Japan from tightening monetary policy. According to the BoJ's expectations, inflation may struggle to meet its 2 per cent target by 2020, and BoJ governor Toshihiko Kuroda failed to deliver on his promise. Mr Kuroda said the BoJ had mispredicted prices and that the lower inflation target this time was due to deflationary attitudes among households and businesses as well as falling oil prices. At the same time, he said he would firmly implement strong easing, but there was no need to continue to expand it.The actions of the Bank of Japan are in line with our expectations. At least this year, there is no need to worry about the policy shift of the Bank of Japan. We need to pay more attention to the position of the adjustment-prone European Central Bank before September.

ECB assets hit a new high, Dragila rose to euro

The latest figures show that the ECB has bought more than 100 billion euros of corporate bonds, pushing the ECB's total assets to 4.23 trillion euros, higher than the total assets of the Federal Reserve and the Bank of Japan and close to Japan's total GDP last year. The Fed has kept its balance sheet unchanged at $4.5 trillion since 2014, but the European Central Bank and the Bank of Japan are still expanding. In fact, the Fed's assets were surpassed by the European and Japanese central banks in June (chart 5). The Fed plans to start shrinking its balance sheet by the end of this year, and its balance sheet will be further smaller than the other two central banks.

The ECB held its latest monetary policy meeting last Thursday, and although it unexpectedly announced that it would stand still, Mr Draghi's speech once again exploded the market. He said that for the withdrawal of QE policy, "the management committee also agreed not to set a date for adjustment, but should discuss forward-looking guidelines for monetary policy adjustment in the autumn".Because this talk of "see you in autumn" gives the market a full imagination, the euro has formed a V-shaped reversal in a short time.The euro rose 1.7% against the dollar throughout the week to break through 1.16 (chart 6).If the ECB does announce its withdrawal from the QE in September, and the Fed starts shrinking its schedule in September, it is bound to cause a panic slump in the stock and bond market. So the governors' comments need to be closely watched before the major central banks meet in September.

The second round of negotiations begins, the probability of soft Brexit is higher.

Last week, British Brexit Minister David Davis and EU Brexit Minister Barnier began the second round of Brexit negotiations in Brussels, Belgium. With little real progress in the first round of talks on the 19th of last month, the talks continued to focus on key contradictions in the Brexit negotiations, including border controls in Northern Ireland, civil rights, break-up fees and future relations. Davis said that last month's meeting was a good start, and that it was time to "talk about something substantive" and that progress must be made in this negotiation.

But it is not easy to reach an agreement. The EU believes that the terms offered by Britain to EU residents staying in the UK are far below the EU's expectations and wants Britain to pay more break-up fees. However, the British side regarded the terms proposed as "fair and thoughtful" and said that apart from those that must be paid, "not a penny will be given more". However, this tough stance has been attacked within the British government. Both the Labour Brexit Minister and the British Chancellor of the Exchequer believe that Britain should give priority to employment and economy in the negotiations, and that if Britain insists that "no agreement is better than an adverse agreement", Britain may face more serious sanctions.We believe that the new British government has just been formed, Theresa May is very weak, perhaps under internal and external pressure, she will finally compromise, Britain has a higher probability of soft Brexit.

Now is a good time to lay out emerging markets.

Last week, money continued to flow into emerging market equities and bonds, and the inflows expanded, according to the latest EPFR data. Emerging market stocks rose as a whole, with the MSCI emerging markets index up 1.0%, led by Chinese and South Korean stocks. The flow of money into the Chinese stock market was the largest weekly inflow in two months (chart 7). Similarly, most emerging market currencies appreciate, which is still driven by a weak dollar (chart 8).

Investor interest in emerging markets, especially in China, is picking up, Merrill Lynch said last week.The further decline in producer prices in China and the indicators of the credit cycle show that the pressure for further tightening of monetary policy in the future is decreasing, which is undoubtedly a big boon for the stock market.And, as we mentioned in last week's weekly newspaper,The earnings performance of emerging market technology stocks is strong and is likely to continue to drive the index higher in the future. So now may be a good opportunity to lay out emerging market stocks.

II. Trend of large categories of assets

Will the production reduction agreement still bring glory?

Oil prices fall again

Last week, WTI crude oil futures traded at $45.77 a barrel, down 2.1% from a month earlier, while Brent crude futures were at $48.88 a barrel, down 1.7% from a month earlier (chart 9). Although US crude oil and gasoline inventories fell much more than expected this week, and the number of US wells fell by 1, the second decline since January, oil prices were boosted at the beginning of the week. But then Petro-Logistics, the data provider, said the increase in Saudi Arabia, the United Arab Emirates and Nigeria would lead to an increase in OPEC crude oil production by 145000 b / d this month, bringing the organization's total oil production above 33 million b / d. Next week, ministers from OPEC and non-OPEC countries will meet in St. Petersburg to discuss production cuts, but market expectations for such negotiations are low.We are not optimistic about short-term oil prices. Unless more important news is announced at this meeting, it will be difficult for oil prices to recover significantly in the short term.

Gold prices may remain at current levels

Last week, COMEX gold closed at $1251.1 an ounce, up 1.9% from a month earlier (chart 10). As we said in last week's weekly report, gold broke through $1250 an ounce on the back of full release of interest rate hikes and rising risk aversion. Last week, however, the main helper was the dollar, which fell sharply after Trump's health care bill was vetoed in the Senate, and ECB President Draghi's remarks also boosted the euro and continued to weaken the dollar. all these are the reasons for the rise in gold.Gold lacks the incentive to move up quickly in the short term, and it is likely to remain at the central level of $1250 this week.

Draghi once again affects European stocks and bonds

Draghi's speech suppressed European stocks

Us stocks continued to rise last week, with the Dow Jones Industrial average, the S & P 500 and the NASDAQ rising 0.3 per cent, 1.0 per cent and 1.8 per cent, respectively, to 21611.78, 2473.45 and 6390 (figure 11). Even if Trump's health care bill was rejected in the Senate last week, US stocks have not been significantly affected. The main driver of last week's rally in U. S. stocks was that listed companies such as Morgan Stanley reported better-than-expected results again.In the short term, U. S. stocks are still supported by corporate earnings, and if you want to see a downward trend in U. S. stocks, you may have to wait until after August.

Most European stocks fell last week, with France's CAC40 index, Germany's DAX index and Italy's ITLMS index falling 0.7 per cent, 1.5 per cent and 0.3 per cent respectively, while the UK FTSE 100 index rose 1 per cent (chart 12). The fall in European stocks was understandable. Although the ECB announced that it would stand still, Draghi's speech hinted that he would announce his plan to withdraw from the QE in September, and the stock market fell.However, more investors expect the ECB to announce plans to exit the QE in October or later, so the recent market performance has been a bit excessive and is likely to rebound this week.

Us and European Treasury yields fall

The yield curve continued to flatten last week, with 2-year yields rising 1bp, while 10-year yields closed down 9bp at 2.24% (chart 13).Us bond yields fell for two main reasons: 1. The veto of Trump's health care reform bill led to a decline in investor expectations of Trump's market; 2. Market expectations for the Fed to raise interest rates are weak.Us bond yields rose along with European bonds in the first half of July, but then fell under the pressure of dove Yellen, a trend extended by the ECB's inaction last week.

German bond yields fell last week, with 1-year and 10-year yields falling 1bp and 2bp, respectively (chart 14). Although Draghi hinted at last week's meeting that he might announce his withdrawal from the QE plan at the September meeting, the market is divided on this, and the ECB did not do anything at this meeting. European bond yields fluctuated last week. Considering that it is only a matter of time before the ECB exits the QE and there is a high probability that European bond yields will rise, we need to be more cautious about investing in the bond market in the future.The ECB may continue to ease this year, and officials may be more dovish if inflation in Europe falls again, at a time when global inflation seems to be falling.