Authors: Niu Bokun, Zhang Wei

1 Real estate sales decreased month-on-month, and land transactions increased significantly.

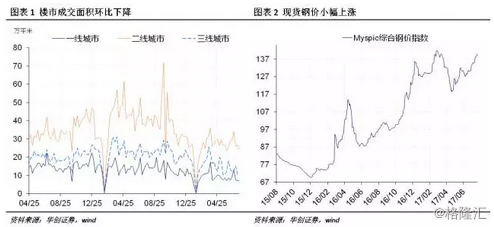

The average daily transaction area of the property market dropped sharply last week compared with the previous week. as of last Friday, the average daily transaction area of commercial housing in 30 large and medium-sized cities was 422300 square meters, down 44.07% from the same period last year. First -, second-and third-tier cities fell by 53.62%, 33.99% and 53.94% respectively; overall month-on-month decline of 6.07%, of which first-and second-tier cities decreased by 0.69%, 8.87% and 2.86% respectively (chart 1). In terms of land transactions, as of July 16, 100 large and medium-sized cities had a land transaction area of 27.5945 million square meters, a substantial increase of 77.3 percent over the 15.5638 million square meters in the same period last year.

Last week, the Ministry of Housing and Construction, together with the National Development and Reform Commission and other eight departments, jointly issued the Circular on speeding up the Development of the Housing Rental Market in large and medium-sized cities with net population inflow, calling for the accelerated development of the housing rental market in large and medium-sized cities with net population inflow. including the construction of housing rental trading platforms, encouraging multiple channels to increase the supply of new rental housing, and selected 12 cities, including Guangzhou, Shenzhen and Nanjing, to pilot.

After Shanghai announced at the beginning of this month that it would vigorously increase the supply of rental housing during the 13th five-year Plan period, the joint document issued by the nine departments further pointed out the direction of vigorously developing the housing rental market: first, the new land supply structure is more inclined to residential land, especially the proportion of new land for rental housing will increase significantly. With reference to Shanghai's 13th five-year Plan, the new rental housing supply accounts for 60% of the total number of new market-oriented housing units. Second, the increase in the supply of rental housing will to a large extent reduce the supply of commercial housing, and vigorously develop both rent and sale, which must be supplemented by the introduction of corresponding policies and measures. Guangzhou last week introduced policies related to "the same right to rent and purchase", which benefited a limited number of people. however, it is an inevitable trend to standardize the rental market and protect the rights of landlords and tenants.

(2) electricity and coal consumption increased month-on-month, and spot steel prices rose slightly.

On Saturday, the average daily coal consumption of major power generation groups rebounded sharply from the previous month. The average daily coal consumption of the six major power generation groups was 743300 tons, up 8.53% from the previous month and 15.12% from the same period last year. The South China industrial product index closed at 1977.25 points, up 2.94 per cent from the previous month. As of Friday, the steel price index closed at 139.17 points, up 0.97 per cent from the previous month (chart 2). Last week, rebar futures prices fell 2.01% from the previous month, while crude steel prices rose 1.176% from the previous month. As of last Thursday, domestic iron ore prices continued to rise, rising 0.6% month-on-month, while imported iron ore prices rose 8.02% month-on-month. In terms of inventories, coal inventories of the six major power generation groups fell 2.11 per cent month-on-month last week, up 4.31 per cent from a year earlier, while rebar inventories rebounded 3.32 per cent from a month earlier, up 5.85 per cent from a year earlier.

Last week, the average daily coal consumption and the year-on-year increase expanded. As of July 21, the average daily coal consumption rose 8.52% month-on-month in July, up 4.48% from the same period last year. According to the seasonal law over the years, July and August are the peak of electricity and coal consumption. In particular, the average year-on-year growth rate in July is 8.98%, and the growth rate of power and coal consumption will remain high in the short term.

As of July 21, the operating rate of blast furnace rose slightly by 0.3% month-on-month; the operating rate of all-steel tire and semi-steel tire dropped sharply. Combined with other high-frequency data, the industrial boom in July was not as good as the data on electricity and coal consumption. Spot steel prices rose slightly last week, the previous sharp rise in steel prices is mainly driven by the futures market and low inventory support, with the slight rebound in social inventories, steel prices are expected to be under pressure next week. However, with the slow recovery of demand under seasonal factors and the higher-than-expected process of capacity removal since late July, the supply and demand pattern supports steel prices.

(3) the price of food has stopped falling and rebounded, and the price of vegetables has risen sharply during the latent period.

Last Friday, the wholesale price index of agricultural products closed at 94.05, up 1.05% from the previous month, while the wholesale price index of vegetable basket products closed at 92.89, up 1.26% from the previous month (chart 3). Food prices rose due to the rise in vegetable prices. Judging from the detailed data, pork prices fell 1.36% month-on-month last week; vegetable prices rose 6.01% month-on-month (chart 4). Pork prices returned to the downward trend last week. Due to the hot weather, summer school holidays and other factors, the seasonal demand for pork showed a weakening trend, so pork prices will remain low in the short term. Vegetable prices rose sharply last week, and the weather in the south transitioned rapidly from continuous heavy rainfall to hot days, which was disadvantageous to the growth of vegetables, especially leafy vegetables. The south entered an incubation period, while leafy vegetables were more prone to rot in high temperature weather. The sharp reduction in supply led to a sharp rise in vegetable prices. With the extension of the incubation period, vegetable prices are expected to face some upward pressure in the short term.

(4) large-scale net investment by the central bank and upward interest rates in the money market

Overnight market interest rates rose sharply last week. Last Friday, the interbank pledge repo rate R001 closed at 2.8983%, up 24.27 BP from the previous month to 3.4590%, and 52.19bp from the previous month (figure 5). The maturity spread of Treasury yields widened last week, with 1-year and 5-year yields falling 4.59bp and 0.66 bpjue 10-year yields rising 1.92bp respectively (figure 6). Last week, a total of 200 billion yuan of reverse repurchase and 39.5 billion MLF expired. The central bank invested 710 billion yuan through the reverse repurchase operation, of which 500 billion yuan in 7 days and 210 billion yuan in 14 days, with a weekly net investment of 470.5 billion yuan, the largest weekly amount since June.

Last week, the central bank invested a large net amount of money into the market, but in reality, the tight liquidity of the market, especially the sharp rise in short-end interest rates in the money market, indicates the central bank's monetary policy orientation of maintaining tight balance. At the same time, in our interpretation of the financial work conference last week, we pointed out that more attention will be paid to behavioral supervision and accountability in the future, and tight supervision will not be a gust of wind, but will point to the regulatory style in the next five years. Judging from the spirit of People's Daily's successive articles and three meetings of the party last week, reshaping the regulatory framework, promoting regulatory coordination and financial deleveraging will be more determined than the market expected. It also means that the shift in monetary policy will come later than the market expected.

The dollar index fell to a new low and the offshore RMB rose sharply.

Last week, the dollar index closed at 93.9659, down 1.22% from the previous month. The weakening trend of the US dollar did not change last week, and the pattern of internal and external troubles once again led to a sharp weakening of the dollar index and falling below the 95 mark. From a domestic point of view, three Republicans in the US Senate opposed the direct replacement of the Obamacare bill, resulting in the failure of the bill by half a vote, which means that the health care bill failed again after several twists and turns. Market expectations of the "Trump New deal" have been further bruised, affecting the dollar to its lowest level since August 2016. Both the ECB and the Bank of Japan left monetary policy unchanged last week, but ECB President Draghi said at a news conference that he was optimistic about the economy and inflation and would discuss revising his forward guidance this autumn. The euro rose to a two-year high led by ECB hawkish expectations, and the dollar index fell further.

On Friday, the spot exchange rate of the US dollar against the RMB closed at 6.7681, down 60bp from the previous month; the spot exchange rate of the US dollar against the offshore RMB closed at 6.7620, down 205bp from the previous month, and the difference between the offshore and onshore RMB exchange rate widened to 61bp (figure 8). The onshore and offshore renminbi rose sharply last week, driven by a sharp weakening in the dollar index. Last week, safe released data on the settlement and sale of foreign exchange by banks in June, showing a deficit of 142.5 billion yuan in June, with a previous value of 117.8 billion yuan, and a deficit in the settlement and sale of foreign exchange for 24 consecutive months, and the scale has been continuously expanding; in June, the deficit between banks in settlement and sale of foreign exchange for customers was 92.3 billion yuan, with a previous value of 85.2 billion yuan, and the scale of the deficit expanded for two consecutive months.