Author: Zhong Zhengsheng Qian Wei

Source: Monita Macro Research

ReportAbstract

Topic of the week: the growth rate of government investment has rebounded sharply, will the recovery of private investment be affected?Under the efforts of investment in infrastructure, railways and the western region, the growth rate of government investment rebounded sharply in October, and the gap between the growth rate of government investment and private investment narrowed significantly again. Recently, the growth rate of loan balance of small and micro enterprises is higher than that of large enterprises; the recovery of private investment started at the beginning of the year, with a phased high at the end of the second quarter, and recently showed a downward trend as a whole; government investment has been declining since the beginning of the year and has rebounded since August. From the perspective of time, after the beginning of credit easing in the third quarter, government investment took the lead in rebounding, private investment slowed down, and the effect of the policy has not yet been reflected. The growth rate of government and private investment is divided into medium-term trend items and short-term disturbance items.According to the medium-term trend, private investment is generous and downward in recent years, and when government investment is upward (downward), the downward pace of private investment will accelerate (slow); from the perspective of short-term disturbance, both of them will be inThere is a significant negative correlation in 2005-2007, 2013-2016 and 2018, while the correlation in other regions is not obvious. government investment and private investment may "crowd out" each other most of the time, but rarely promote each other.At present, the possibility of government investment restraining private investment in the medium-term trend is relatively low, but on the one hand, private investment is generously downward, and this round may be related to equipment renewal and environmental protection technological transformation, on the other hand, under the stimulation of stable growth policies, short-term private investment may face certain "crowding out" pressure, the recovery momentum is facing challenges, and the follow-up trend should pay attention to the landing effect of wide credit and private support policies.

Real economy: infrastructure investment began to force, real estate sales pressure to start construction and land acquisition. Industrial productionThe industrial added value rebounded in October compared with the same period last year, driven by factors such as the rebound in exports and infrastructure investment, but the overall production willingness is still not high. The South China industrial product index continued to decline this week, and the demand for coal consumption in power plants rebounded at the beginning of the heating season.Upstream energyInternational oil prices have stopped falling and rebounded due to OPEC's consideration of production cuts, and the pressure of thermal coal destocking restricts short-term prices.Mid-stream productsWinter start demand weakens, steel mill inventory increases, steel prices continue to be under pressure in the short term; supply and demand in the south maintain a tight balance, local clinker supply is in short supply, and cement prices continue to strengthen.Downstream real estate"Golden Nine Silver Ten" is no longer, the national commercial housing sales for two consecutive months of negative growth compared with the same period last year, downstream sales pressure or upstream land acquisition and construction transmission, real estate enterprises financing pressure and difficulty also further increased.Food priceThe classical swine fever epidemic in Africa continues to spread, and pork prices are lower again this week, but the impact of industry capacity loss is greater, and pig prices may become a major risk to inflation next year. Domestic finished product oil prices have ushered in the largest reduction in domestic oil prices in nearly four years. On the whole, inflationary pressures eased further throughout the year.

Financial markets: over the past 50 years, the bidding of treasury bonds has exceeded expectations and stimulated the bond market to soar. Money marketThis week, the central bank still did not carry out reverse repurchase operations, the "quiet period" lasted 16 trading days, and monetary interest rates rose slightly.Bond marketSpurred by the expectation of economic downturn and the higher-than-expected bidding for 50-year treasury bonds, the bond market rose sharply this week, with long-term bonds outperforming short-term bonds, and the yield on 30-year treasury bonds fell the steepest. In addition, interest rates on Chinese and US one-year Treasuries were upside down for the first time in a decade.RMB exchange rateIt has fallen 34 points this week, and the offshore market has appreciated by 0.38% and 0.27% respectively in spot and forward, with a strong offshore performance or related to liquidity recovery. The deficit between banks' settlement and sale of foreign exchange narrowed significantly in October. The improvement in the trade surplus in goods and the large inflow of securities investment are important supports. In the short term, the market is concerned about the meeting between the heads of state of the two countries at the G20 summit at the end of the month, and the RMB may maintain a volatile trend until then.

I. this week's speechQuestion: will private investment be affected when government investment picks up?

According to the investment data released in October, although the growth rate of private investment remained high in that month, the growth rate of government investment, represented by infrastructure, rebounded sharply again, ending the previous continuous decline. So, will private investment face crowding-out pressure, and will the recovery so far this year be affected?

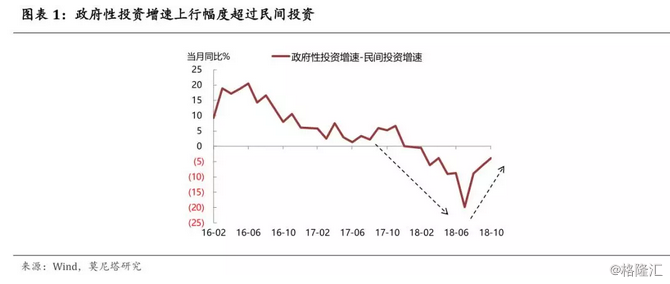

Joint efforts in infrastructure, railways and the western region, 10The growth rate of government investment rebounded faster than that of the private sector in June.Fixed asset investment data in October showed that investment in infrastructure (excluding electric power) was 5.5% year-on-year, railway transport investment was 18.8% year-on-year, and investment in the western region was 3.2% year-on-year, all of which directly led to a sharp increase in government investment growth. Private investment rose by 9.6% in October from a year earlier, a relatively limited increase and a long way from the July peak. As a result, the gap between the growth rate of government investment and that of private investment narrowed significantly, and the growth rate of private investment once again faced the possibility of hanging upside down after surpassing the government growth rate at the beginning of the year (chart 1). So, how to understand the recent relative trend changes, how will the recovery process of private investment be affected?

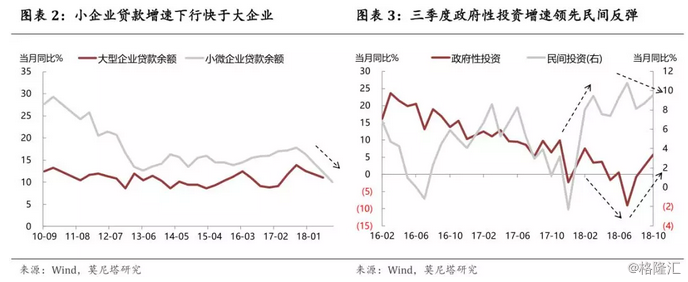

The effect of credit support to the private sector may not yet be reflected, and the growth rate of government investment has taken the lead in rebounding under the broad credit policy.At the recent policy level, there has been repeated emphasis on supporting the development of private and small and micro enterprises, while providing necessary help in monetary policy and credit policy. In terms of credit dimension, the recent growth rate of loan balances of small and micro enterprises is higher than that of large enterprises (chart 2). From the investment dimension, this round of private investment growth began to rise at the beginning of this year, recently there is a certain high downward trend (chart 3). In contrast to government investment, the growth rate of the month has been on a downward trend since the beginning of the year, with a phased low in July, which rebounded for the next three months and returned to positive growth. At present, the reason for the high growth of private investment can hardly be attributed to the credit policy, on the contrary, after credit began to ease, government investment bottomed out and rebounded, while private investment slowed down.

The medium-term trend shows that private investment has declined in recent years, and government investment has a certain impact on its rhythm.So, if government investment continues to increase, will it crowd out private investment? From the historical data, it is difficult to draw a direct conclusion that the overall correlation coefficient between them is about 0.15 (figure 4). In order to compare the relationship between the two, we use the method of HP filtering to split them into medium-term trend terms and short-term disturbance terms respectively. From the point of view of the medium-term trend, there is no obvious substitution to the opposite. the general direction of private investment has been downward in recent years, and government investment keeps in the same direction most of the time, and its effect is mainly reflected in the influence of rhythm. in the stage of the decline of the trend of government investment, the downward speed of private investment is slower (chart 5). Of course, in the mid-cycle dimension, this may be related to the underlying economic cycle, and can not be simply understood as the mutual occupation of the two.

From the perspective of short-term disturbance, there is a significant negative correlation between them in most stages, while the stage of positive correlation is relatively rare.Comparing the short-term disturbance items of government investment and private investment, if calculated as a whole, the correlation coefficient between them is about-0.39, which has a strong negative correlation. If we make a more detailed division of the interval, we can find that the two have a more significant negative correlation in 2005-2007, 2013-2016 and 2018 (Chart 6, Chart 7), while the correlation of other intervals is basically maintained around 0. Therefore, from the perspective of short-term fluctuations, government investment and private investment crowd out each other most of the time, but rarely promote each other. In particular, in the past year, there has been a negative correlation between the two.

Historical experience shows that the degree of recovery of private investment may face a certain crowding-out pressure from the rebound of government investment.Looking forward, can the recovery of private investment continue?From the perspective of medium-term trendIn the context of the overall decline in the nominal growth rate of the economy, private investment is slow to decline or continue. From the perspective of the whereabouts of banks' corporate loans, the growth rate of operating loans has continued to decline since the beginning of this year, while fixed asset loans have increased, and there is a certain differentiation between the two (figure 8). We believe that this may reflect that the willingness of enterprises to produce is still poor, and one of the main reasons for the rise in private investment is the demand for equipment renewal and environmental protection. Therefore, this may prove to a certain extent that it is difficult for private investment to turn upward in a major direction. On the other hand, government investment interferes with the pace of private investment only in the stage of sharp rise, which is also more difficult, because the demand for this round of government investment is mainly reflected in the steady growth of short-term infrastructure (figure 9).In the short termSince the beginning of this year, the negative correlation between government and private investment is relatively obvious, while the base of infrastructure investment is relatively low, and there is more room to continue to rise in the future, which may make the recovery of private investment face the threat of crowding out pressure. While maintaining the strength of infrastructure to make up for deficiencies, we should pay more attention to the confidence and willingness of private investment and pay attention to the guidance of credit flow.

Second, realityPhysical economy: capital construction investment begins to develop

1Industrial production

Industrial production is not booming, and the prices of industrial products continue to fall.With the start of the heating season, the average daily coal consumption of the major power generation groups this week continued to pick up last week, rising by 4% month-on-month (chart 10). The South China industrial product index continued to fall, falling 0.4% this week, and infrastructure investment began to rise, but it may still take time for industrial product prices to rise (chart 11). Industrial added value rose 5.9% in October from a year earlier, rising 0.1 percentage points from September, but the overall willingness of the production side is still weak. The main supporting factors include holidays, export grabbing, and infrastructure investment starting to strengthen sharply. In addition, the production and sales rate has fallen sharply, which also points to weaker overall demand downstream. It is worth noting that the output of major industrial products has rebounded, in addition to infrastructure demand, there may also be the effect of marginal relaxation of production restrictions, but whether this phenomenon can be maintained still depends on the pressure of the overall environmental quality in the heating season. Infrastructure investment rebounded sharply in October, under the background of increasing downward pressure on the economy, infrastructure investment is expected to continue to pick up, central and western railways, rural poverty alleviation and other directions or key points, but recently, the NDRC has repeatedly stressed that infrastructure construction insists on "doing its best, acting according to its capacity, avoiding blind investment and repeated construction". At the same time, the control of local invisible debt has not been relaxed, and the possibility of a sharp rise in infrastructure investment is relatively low.

2Upstream price

International oil prices rose for three days in a row, thermal coal futures fell more. Coal:The futures of thermal coal, coking coal and coke are down 1.2%, 2.7% and 1.6% respectively this week (figure 12). The decline in power has not expanded compared with last week. At present, the inventory of upstream Qingang and downstream power plants is still rising, and the main tone of recent depots remains unchanged. However, with the advent of the heating season, downstream demand has rebounded, and coal prices may remain stable or decline slightly in the short term.Crude oil:Us oil and cloth oil fell 4.7% and 3.7% respectively this week, falling below $60 and $70 per barrel respectively. On the supply side, US production and EIA inventories continued to rise, the overall increase outside OPEC exceeded expectations, and the OPEC also increased slightly in October. On the demand side, OPEC reduced global demand in 2018 and 2019, respectively, and the contradiction between supply and demand heated up in a short time. However, oil prices have risen one after another in the last three days, there are rumors in the market that OPEC may be considering production cuts, and oil prices may have a phased bottom (figure 13).Colored:This week, LME copper and aluminum rose 3.4% and fell 0.4% respectively. In addition, gold also rose more than 1%. The Federal Reserve said this week that it was more cautious, the global economic downturn was expected to rise, the prices of major non-ferrous varieties continued the downward trend, and gold rose (Chart 14).Iron ore:It fell 1% again this week, fluctuating in recent weeks after periodic highs. October production data showed a pick-up in production activities such as steel, and downstream demand still supported short-term prices. (figure 15).

3Mid-stream products

The seasonal weakening of demand is a drag on steel prices, and the differentiation of cement glass continues. Steel:Rebar futures fell 1.4% this week, spot prices fell synchronously (chart 16), in the short term, winter start demand declined, social inventory as a whole is low (chart 17), but steel factory inventory increases rapidly, downstream traders do not have a strong desire to hoard goods, corporate profit pressure has increased, unless the air pollution problem becomes serious again, steel prices may continue to weaken in the short term. In the medium term, on the one hand, the Tangshan municipal government disclosed that this year's cumulative reduction in steelmaking capacity was 5 million tons and ironmaking capacity was 2.98 million tons, and the annual task of 7.81 million tons had been overfulfilled ahead of schedule. On the other hand, data show that the upper limit targets of reducing coal production capacity by 500 million tons and crude steel production capacity by 150 million tons during the 13th five-year Plan period are expected to be completed two years ahead of schedule. This may mean that the industry pattern and the logic of supply-side dominant prices will change in the next two years.Building materials:The cement price index continued to rise this week, although there was rain in the south, but the demand was relatively stable, and the off-peak production also made the supply slightly insufficient. In the case of catching up with the progress of infrastructure construction, the short-term market may maintain a tight balance and the price was guaranteed, but as the north gradually entered the off-season, prices continued to lack momentum. The glass index narrowed its decline this week and continued to hit a new low for the year.

4Downstream real estate

Downstream sales pressure began to transfer to the upstream construction and land acquisition.The sales area of commercial housing in 30 cities fluctuated in a narrow range compared with the previous week (chart 18), while the land supply area in 100 cities rose seasonally last week (chart 19). In October, the national real estate investment was 7.7% year on year, still maintaining a high position, showing a certain degree of resilience, and real estate investment may remain stable in the short term. However, from the marginal data, the pressure of downstream sales shows signs of starting construction and taking land upstream. The growth rate of commercial housing transactions across the country continued to slow in October, with an increase of 2.2% from January to October, down 0.7 percentage points from January to September. In a single month, there has been two consecutive months of negative growth, the sales market of "Golden Nine Silver Ten" is no longer available, and the policy signal of relaxing purchase restrictions on the demand side is still difficult to see. In October, the growth rate of new construction area and land purchase area fell by 5.6% and 4.2% respectively compared with the same period last year, both showing a decline for three consecutive months, and the downward pressure on real estate investment is emerging.

The early acquisition of land continues to push up the financing pressure of real estate enterprises.As sales are not as expected, it is more difficult to get the money back, and a large amount of land is taken in the early stage, all of which are increasing the financing pressure on real estate enterprises, but the illegal entry of funds into the property market, such as financial regulatory policies and verification trusts, has not been significantly relaxed, and the financing difficulties of real estate enterprises are also increasing. However, Central Plains real estate statistics show that since November, real estate enterprises have raised a total of more than 10 billion yuan, financing costs are still high. In this context, short-term housing enterprises intensive financing, increased development, promotional payback and other trends will continue.

5Food price

Pork and vegetable prices continued to weaken, domestic finished oil prices fell sharply, and inflationary pressures further reduced during the year.This week, the 200 index of major agricultural products of the Ministry of Agriculture continued to fall 0.6% month-on-month (chart 20), fruit prices narrowed, vegetables continued to weaken seasonally, and pork prices fell wider (chart 21). The epidemic of classical swine fever in Africa continues to spread. This week, an outbreak of African classical swine fever occurred in Xishui County, Hubei Province. The current spread is obvious, and pig prices are restrained to a certain extent in the short term, but the impact of industrial capacity loss in the medium term is greater, which will be an important risk of rising inflation next year. Gasoline prices have been cut by 510 yuan per ton since Friday, the biggest drop in finished oil prices in four years, and the boost of crude oil consumption to CPI may weaken as crude oil prices weaken.

III. FinanceMarket: more than expected bidding of treasury bonds in the past 50 years has stimulated the bond market to soar.

1Money market

The reverse repurchase "quiet period" lasts for 16 trading days.Money market interest rates rose slightly.Affected by factors such as the tax period, although the total liquidity of the banking system has declined, the central bank believes that the overall level is still reasonable and sufficient, and there is still no reverse repurchase operation this week. This quiet period has reached 16 trading days. Money market interest rates rose slightly this week (figure 22). The interbank certificate of deposit issuing interest rate continued to diverge this week, with one-month issuing rates lower and three-month and six-month issuing rates higher, reflecting the relative shortage of medium-and long-term funding sources for banks (chart 23). The size of the base money is shrinking this year, although the reduction of the reserve requirement has increased the monetary multiplier, but the distance between it and the theoretical limit has not been significantly reduced, which means that the effect of credit expansion is not satisfactory at present, and some liquidity is still silted up in the banking system. Monetary policy may be further relaxed in order to continue to support the real economy.

2Bond market

Over the past 50 years, the bidding of treasury bonds exceeded expectations and stimulated a sharp rise in the bond market, and the yield of 1-year treasury bonds between China and the United StatesThe rate is upside down.The bond market has soared this week, with long-term bonds performing better than short-dated bonds, with 30-year bonds actively traded, with yields down 17 BP (chart 24) and the yield curve slightly flattening (chart 25). The one-year spread between China and the US has been upside down for the first time since 2008. Mid-week economic data show that downward pressure on the economy is still high, while inflation is relatively moderate. In an environment of overall loose liquidity, the "asset shortage" may once again become the driving force of capital allocation in the bond market, especially long-term funds such as insurance. On Friday, the bidding of 50-year treasury bonds by the Ministry of Finance significantly exceeded market expectations, or an example. Fed officials spoke this week about concerns about the economic downturn, the market is expected to slow the pace of interest rate increases, and the upward pace of short-term US bond interest rates and the constraints on domestic long-term interest rates caused by the spread between China and the United States may also slow. this is also good for the bond market.

3RMB exchange rate

The Federal Reserve sent a mild signal that the RMB exchange rate depreciated slightly.This week, the RMB exchange rate fell 34 basis points, a slight depreciation of 0.05%, the offshore market spot and forward rose 0.38% and 0.27% respectively, the dollar index fell 0.51% (chart 26), and the CFETS RMB index closed at 92.48, continuing to appreciate slightly from last weekend (chart 27). The continued stabilization of the renminbi this week is related to the weakening of the dollar index and the marginal easing of the Sino-US trade conflict atmosphere. A number of Fed officials released concerns about the uncertain economic outlook, the market believes that the pace of raising interest rates may be uncertain, and the dollar index fell back this week. China's Ministry of Commerce said that after the call between the heads of state of China and the United States, high-level contacts in the economic and trade fields between the two sides have resumed, and the working team has maintained close contact and conscientiously implemented the consensus reached by the two heads of state on the phone. In addition, the stronger performance of the offshore market may have something to do with the central bank's tender to issue 20 billion yuan of central bank notes in Hong Kong to recover liquidity. In the short term, the market is concerned about the meeting between the heads of state of China and the United States at the G20 summit at the end of the month, and the RMB exchange rate may remain volatile until then.

10The deficit between bank settlement and sale of foreign exchange narrowed significantly in April.The deficit between banks' settlement and sale of foreign exchange in October was 2.9 billion yuan, 14.6 billion yuan smaller than that in September, and the deficit in foreign-related payments was 7.4 billion yuan, 20.5 billion yuan lower than in September. The main source of the deficit is still trade in services. in the case of high consumption of services such as imports and tourism, the demand for foreign exchange sales in service trade may gradually increase the deficit between current account settlement and sale of foreign exchange. Capital and finance once again turned into a surplus of 1.8 billion yuan, mainly because the demand for securities investment settlement of foreign exchange increased in October, while direct investment remained relatively stable. With the opening of the domestic financial market, the inflow of foreign capital is expected to form support. The overall deficit in foreign exchange settlement and sales narrowed significantly from the previous month, mainly due to a sharp rise in the trade surplus in goods, which was related to the high growth in exports in October. In addition, earnings and current transfers are a significant improvement. Looking at the trend in the past few years, it has a clear seasonal pattern and tends to rise in the fourth quarter.