Author: Shen Wanhongyuan Financial Research team

The strict regulatory environment over the past 17 years, the initial weakness of 18 years of economic growth, and the recent significant policy tilt towards small and micro enterprises, especially the "125th" target put forward by Chairman Guo Shuqing for loans to private enterprises on November 8, have made investors continue to pay more attention to urban agricultural banks. It is undeniable that the credit risk of small and medium-sized enterprises is higher than that of large enterprises. Under the unanimous expectation that the market forms an economic downturn, urban agricultural commercial banks with small and medium-sized enterprises as the main customer group will inevitably be questioned by investors on asset quality. But because of this, the difference in expectations is often more easily ignored. For the "gold" banks, which are externally in line with the east wind of policy and have unique internal operations without historical undesirable baggage, we cannot generalize, as is the case with Changshu Bank. (1) on the one hand, for the "12th five-year Plan" goal, Changshu Bank has actually reached the standard, and the earlier development strategy has made Changshu Bank the biggest beneficiary under the current regulatory environment. (2) on the other hand, different from other local banks, Changshu Bank walks out of the differential road of focusing on operating loans, and its unique small and micro business model makes it have the characteristics of "high return + low risk". This report starts with the high profit of Changshu Bank, excavates the core factors of sustained high growth of performance, and corrects the difference of investors' expectation on the persistence of small and micro model and asset quality of Changshu Bank. We believe that Changshu Bank's differentiated small and micro business model and excellent asset quality can stand out in the current environment of increasing macroeconomic uncertainties.

1. High profits come from stronger asset-side bargaining power

1.1 performance growth reached a record high, high interest rate spreads established absolute advantage

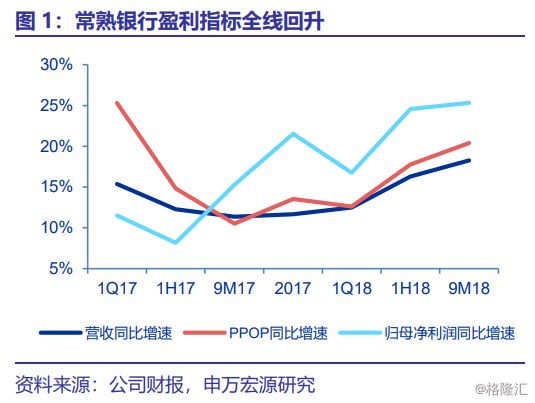

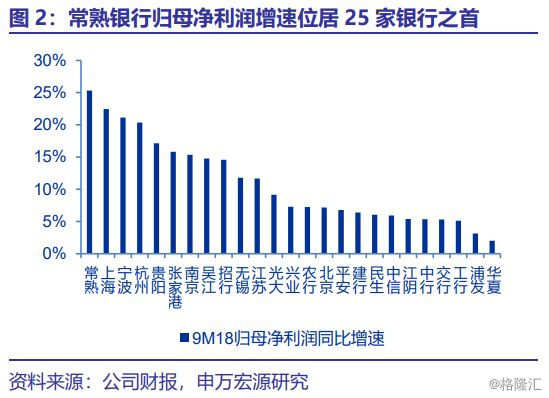

Over the past 18 years, the revenue, PPOP and performance growth of Changshu Bank have rebounded in an all-round way, and the core trend of stable and sustained growth has been basically established. Changshu Bank was listed on September 30, 16, compared with the old 16 listed banks, investors' attention and understanding of Changshu Bank may not be sufficient. From the performance point of view, the 17-year quarterly report of Changshu Bank began to return to double-digit growth in net profit, and revenue growth gradually picked up. In the past 18 years, the performance of Changshu Bank has exceeded market expectations twice. The net profit of 9M18 has increased by more than 25% year-on-year, reaching the highest level of 25 listed banks. The revenue and PPOP have also accelerated repair. Revenue and PPOP have increased by 18.3% and 20.4% respectively, far higher than the average of 7.9% and 9.4% of listed banks. We believe that the continued and significant profit statement repair of Changshu Bank over the past year strongly demonstrates the certainty of its core profitability, driving ROE back to the upward channel.

The growth of net interest income shows a "smile curve" to boost revenue, and the spread is much better than that of the industry. It is not difficult to find that the year-on-year growth rate of net interest income of Changshu Bank has continued to rise since it hit bottom at the end of 17 years, and 9M18 grew by 17.2% year-on-year, which continues to narrow the scissors gap with revenue growth. At the same time, the net interest margin of Changshu Bank began to stabilize and pick up, and the 1H18 spread ranks first among listed banks. At the same time, we estimate that the annualized net interest margin of 3Q18 rebounded to 3.03% from the previous quarter, establishing the absolute advantage of the interest margin.

1.2 the small and micro model based on operating loans gives stronger loan pricing power.

The high credit growth contributes to the performance growth, and the differentiated credit structure achieves high interest rate spreads. In terms of performance drivers, scale expansion is the core driver of high performance growth, with a 28.3 per cent growth in retail loans driving a 22.7 per cent year-on-year increase in loans. At present, retail loans are basically on a par with public loans, and the proportion of retail loans has reached 49.2%, ranking firmly in the forefront of listed banks. Different from large banks and consumer loans, Changshu Bank is dominated by personal operating loans, accounting for 63.4% of retail loans. This differentiated development strategy makes the loan yield much higher than that of comparable banks, with 1H18 retail loans and total loan yields as high as 8.0% and 6.8% respectively, ranking first among listed banks. Stronger loan bargaining power is the main reason why Changshu Bank continues to be ahead of its peers in interest rate spreads.

Obviously, the small and micro development model focusing on operating loans can make Changshu Bank the biggest beneficiary in this round of regulatory environment.On November 7, Chairman Guo Shuqing put forward the "12th five-year Plan" target for loans to private enterprises, that is, among the new loans to private enterprises, the loans of large banks to private enterprises should not be less than 1 to 3, and the loans to small and medium-sized banks should not be less than 2 to 3. After three years of striving, the proportion of loans to private enterprises from the banking sector to private enterprises will not be less than 50% of the new loans to public enterprises. At present, the statistical caliber of banks on "private enterprise loans" remains to be further clarified, and we roughly estimate that Changshu Bank has reached the standard according to the rough estimate that "small enterprises are dominated by private enterprises". By the end of the third quarter, the total amount of loans from Changshu Bank reached 91.86 billion yuan, of which 41.48 billion yuan was for public loans. According to our research, according to our research, according to the Ministry of Industry and Information Technology, the loans for large and medium-sized enterprises in Changshu Bank are not as good as those for public loans. Obviously, the proportion of loans for small enterprises has reached the standard, and we judge that the proportion of increment may be even higher. Therefore, taking advantage of the policy, Changshu Bank will enjoy more policy dividends in the regulatory environment of supporting the operation and development of private enterprises.

two。 Deeply ploughing small and micro businesses has become the core cornerstone of sustained high performance growth.

If it takes ten years to sharpen a sword, the newcomer may not be able to chase it. Local banks are oriented to meet the financial needs of local residents and small and medium-sized enterprises. the limitation of cross-regional expansion makes local banks face greater competitive pressure while ploughing the local market. Changshu Bank has been laying out retail small and micro business since 2009, regionalizing, grassroots and finely serving individual operating loan customers, which is "hard work" and requires a lot of human resources as support in the early stage. in the later stage, we pay more attention to the cultivation of customer stickiness; at the same time, it is also the company's long-term and firm development confidence at the strategic level, which is not achieved overnight.This section will analyze in detail the five bright spots of Changshu Bank in serving small and medium-sized enterprises, especially small and micro enterprises: strong team construction, "semi-automatic" credit factory, heterogeneous card position advantage of branches, unique layout of village banks, and stable management. Because of this, Changshu Bank can establish the fundamental advantages of high interest rate spreads and high profits.

2.1 strong small and micro team size to build team barriers

The combination of the early "crowd tactics" and the later "credit factory" created a team barrier for Changshu Bank to develop small and micro business:

The target group of retail business of Changshu Bank is small and micro enterprises and individual industrial and commercial households. Different from large and medium-sized banks, the average size of small and micro loans in Changshu Bank is only about 200000. In terms of small and micro credit, it has its own unique marketing strategy: since 2003, it has implemented the customer manager system, actively collected and analyzed customer information, and strengthened business contacts with customers through online and offline channels. It is worth noting that: (1) the small and micro team of Changshu Bank expanded rapidly before 2015, from a team of less than 50 people in 2009 to a team of 1000 people in 2015. We believe that a large, timely and effective input of personnel is very necessary in the early stage of the development of small and micro business. it is also the main reason why it is difficult for "latecomers" to surpass due to high labor costs; (2) the small and micro team of Changshu Bank has continued to grow in the past two years, but the growth rate has slowed down, and the team size has been stable at about 1400 people since 16 years. As the small and micro account managers of Changshu Bank are all locals, in the mature period of small and micro business development, the past crowd tactics began to be optimized, relying more on the chain relationship of "people with people" to excavate customers and expand the service radius. It is not difficult to find that despite the slowdown in the expansion of small and micro teams, their loans can still maintain a rapid growth rate of more than 20%.

If the "crowd tactics" is the 1.0 version of the development of small and micro business front-end "deep mining, close tracking of customers", then the "credit factory" is the high-end version of the back-end "double risk prevention and control". As the name implies, the credit factory is the process operation of the loan. Changshu Bank set up a credit factory in 2014. Usually, the customer manager collects customer information to form a unified and standardized template, and then it is delivered to the background for centralized approval of the loan, while the customer manager is still responsible for tracking the loan. On the one hand, this "semi-automatic" credit factory model improves the replicability of business operations, on the other hand, front and rear segmentation and slicing management further ensure the security of small and micro credit. The front end of the account manager collects customer information, maintains close contact with the customer after the loan, and is completely isolated from the loan examination and approval, thus greatly reducing the probability of moral hazard and further ensuring the security of small and micro credit.

2.2 remote branches interpret "card position advantage", and village banks verify the successful replication of small and micro business.

Changshu Bank not only ploughs locally, but also exports its small and micro business model to remote branches and village banks. at present, only 20% of the nearly 25 billion small and micro loans are contributed by Changshu, which fully shows that the small and micro model of deep ploughing small household operating loans has been successfully replicated to other places.

Non-local organizations to expand business space, operating results have been shown. By the end of September 18, Changshu Bank had set up seven branches in Nantong, Yancheng, Wuxi, Yangzhou, Taizhou, Suzhou and Zhenjiang. At present, Jiangsu Province Inner Rural Commercial Bank has opened a total of 20 off-site branches, and Changshu Bank accounts for 35% of the total, substantially ahead of the same industry. Under the circumstances that the current supervision does not liberalize the agricultural commercial bank to set up branches across regions, the expansion territory of Changshu Bank, which ranks first in the number of branches in different places, fully reflects the advantage of card position and occupies the opportunity that other agricultural and commercial banks are difficult to surpass. It will provide an effective guarantee for future performance growth. At the same time, Changshu Bank has opened 15 off-site branches. Nevertheless, at present, 7 sub-branches have not yet been fully arranged, and there is still huge room for sinking in the future. From the perspective of operation, the proportion of 1H18 Changshu non-local loans in total loans has further increased by 3.6 percentage points to 49.7%, more than 10 percentage points ahead of Zhangjiagang Bank, which ranks second, while the proportion of off-site operating profits has already accounted for more than half, a substantial increase of 11.3% over 17 years, fully verifying the effectiveness of off-site business operations.

As the only agricultural and commercial bank in the province with the qualification of mass establishment of village banks, Changshu Bank is proving that "the success of small and micro business can be replicated". Changshu Bank is the first county-level agricultural bank in China to set up village banks, and has the qualification to set up village banks in batches. Thirty village banks have been set up in Jiangsu (9), Henan (6), Hubei (5), Yunnan (10) and other provinces. By contrast, the number of village banks opened by the other four listed agricultural and commercial banks is less than half that of Changshu Bank. From our research, village banks are still mainly small and micro business. At present, 30 village banks are basically profitable, which shows that they have successfully copied the core technology of the parent bank to develop small and micro business. For a long time, the company's financial, retail business and financial market business troika drive Changshu bank performance growth, we judge that village banks will become a new source of sustainable performance growth. At the same time, considering that the current establishment of village banks in Yunnan is not long, it is expected that the contribution to profits will be further enhanced in the future. Therefore, in the case of successful replication of small and micro business models in different places, we have full confidence in the continued high growth of our performance.

2.3 stable management is the solid backing for the long-term development of small and micro business.

From a higher level, Changshu Bank can not do without stable management and long-term firm conviction for a decade of deep ploughing. Song Jianming, chairman of the board, first worked in Changshu Rural Credit Co-operative. In 2009, Changshu Bank formally established the micro-loan department, while the current chairman, Song Jianming, happened to be president at that time. Chairman Song Jianming not only served in Changshu Bank for a long time, but also a staunch supporter and practitioner of retail small and micro transformation. In an interview with the Securities Times on January 17 this year, he made it clear: firmly deepen the small and micro strategy, time will prove that this is the right choice. In addition, President Zhuang Guangqiang has been in office since 2016, but he was the vice president of Changshu Bank in the early days and has actually served in the bank for a longer time. On the whole, the management of Changshu Bank has fully witnessed the ups and downs of the development of small and micro business, and we believe that the stability of management, the long-term nature of service and the firm belief in the development of small and micro business from top to bottom will protect the success of small and micro business.

2.4 Future prospects: increasing per capita production capacity and "dark horse" village banks will become an effective focus for performance growth.

We believe that the future small and micro business of Changshu Bank will no longer rely on the past crowd tactics, but pay more attention to the improvement of per capita production capacity. In fact, in the previous analysis, we can see that the pace of small and micro team expansion has slowed down, while the scale of small and micro loans can still maintain a rapid growth, which is a strong verification of the increase in per capita production capacity. We believe that it is unlikely that the small and micro teams of Changshu Bank will be greatly expanded in the future. the main reasons are: (1) the number of employees of Changshu Bank is several times that of other listed agricultural banks, and the growth of employees has begun to slow down in 17 years. Accordingly, the salary expenditure of employees is also significantly higher than that of other agricultural and commercial banks. (2) the initial stage of small and micro development has passed, and the era of high expenditure on front-end human resources investment will also come to an end, thus relying more on scientific and technological innovation to change to the "offline + online" development model, promoting per capita production capacity to a higher level.

At the same time, the "dark horse" potential of village banks can not be ignored.Changshu Bank announced on October 30 that it plans to set up an investment management village bank in Haikou, Hainan, giving it the status of major shareholders to manage the village banks distributed all over the country as a whole, which is the first listed bank. It is expected that the radiation radius of village banks will expand again in the future. We believe that at present, financial services in the central and western regions are still insufficient, and relying solely on local agricultural commercial banks and rural credit cooperatives is far from meeting the financial needs of residents and enterprises. The superposition of Changshu Bank is to go deep into the grass-roots level to locate the "small and micro". The lack of regional financial services and the misplaced competition of Changshu Bank make the "dark horse" potential of village banks particularly promising.

3. The network sinks and overlaps the potential of different places, and the deposit base is further consolidated.

Changshu Bank's excellent loan bargaining power has achieved high profits, while the more sinking network layout and remote contribution will further consolidate the deposit base and thicken the financial margin for sustained high performance growth.

(1) since 3Q17, Changshu bank deposits have maintained double-digit growth. 3Q18 has increased by 15.8% compared with the same period last year, which is much higher than the average level of listed banks by 8%. Compared with the end of 17 years, the proportion of deposits has also increased by 2 percentage points to 75.4%. Benefiting from the continuously sinking network layout and long-term retail transformation strategy, personal deposits are relatively dominant, with 3Q18 accounting for 53% of personal deposits, ranking first in agricultural and commercial banks. With the gradual consolidation of the deposit base, the deposit cost of Changshu Bank has dropped significantly to 2 per cent of 1H18 after reaching a peak in 15 years.

(2)On the other hand, we expect that the contribution of remote branches to deposit growth will continue to increase.. As mentioned earlier, Changshu Bank currently has 7 remote branches, 15 remote branches and 21 remote village banks, which is a huge advantage different from other agricultural and commercial banks. The competition for local deposits is inevitably fierce, and going deep into the grass-roots regional layout in different places can make additional contributions to the growth of deposits. At the end of 17 years, the proportion of non-local deposits in Changshu Bank was 17%, while by the end of September 18, the proportion of non-local deposits increased by 10 percentage points to 27.2% compared with the end of 17 years. We initially estimate that off-site deposits have increased significantly by 85% compared with the beginning of the year. We believe that the sinking of Changshu banking institutions is still in its infancy, and with the gradual expansion of branches and the continuous development of village banks, remote deposits are bound to create new growth space for deposit business.

4. The asset quality is significantly better than that of the same industry, and the bad rate of small and micro loans is not high.

With the same improvement with the region and the same optimization with credit, the bad inflection point appeared earlier. The bad rate of Changshu Bank has fallen from its highest point since 2016, and the 3Q18 bad rate has dropped to 1.00%. (1) from the perspective of external factors, Changshu Bank has become the beneficiary of the first improvement in regional asset quality. In 2012, China's banking industry entered a new round of bad cycle, with the defect rate rising from less than 1% to 1.67% at the end of 2015. Compared with areas with concentrated excess capacity, the more developed Yangtze River Delta region was the first to expose bad conditions in 2015, with the bad rate in Jiangsu Province turning back after peaking in 2016. By the end of March 18, the bad rate of the banking industry in Jiangsu Province had dropped to 1.23%, far lower than the national average of 1.75%. 90% of the loans of Changshu Bank are distributed in Jiangsu Province, which is bound to benefit from the improvement of regional asset quality. (2) from the perspective of internal causes, Changshu Bank has continued to reduce public loans in the past five years, increasing the proportion of weak cyclical retail loans. The proportion of retail loans of 1H18 Changshu bank rose sharply to 48 per cent from 25 per cent in 13 years, much higher than the average of 25.9 per cent of listed urban agricultural banks. Taken together, Changshu Bank showed a bad inflection point earlier in 2016, which is enough to highlight its excellent asset quality compared with the rising bad rate of agricultural and commercial banks across the country.

The current market concern is that the anti-risk ability of small and medium-sized enterprises is relatively weak or accumulate adverse risks in the economic downturn. We believe that the small and micro business of Changshu Bank is to locate individual operating loan customers. in fact, the probability of moral hazard of such small and micro customers is much lower than that of large enterprises. On the one hand, the front-end small and micro account managers are deeply bound with customers and maintain close contact in grass-roots research, information collection and post-loan management; on the other hand, the "semi-automatic" credit factory is separated and granted objectively, and the small and micro account manager is not involved. Moreover, when they are in operational difficulties, apart from being burdened with the pressure of repaying bank loans, large enterprises also need to consider additional costs such as high staff salaries, and bank debts may not be given priority. For small enterprises, the cost of default is relatively high, and individuals may face lifelong liability for breach of contract. At the same time, a flexible operating system allows small enterprises to minimize other operating costs. According to our recent research, in fact, the bad rate of small and micro loans of Changshu Bank is less than 1%, which is lower than the total bad rate of loans.

In addition, the leading bad indicators and bad identification are significantly better than the same industry, and the overdue loan rate is the lowest level of agricultural and commercial banks. No matter from the static absolute value or from the marginal change trend, Changshu Bank's two leading indicators of concern loans and overdue loans are significantly better than their peers, and the scale and proportion have declined since 17 years. The proportion of overdue loans is as low as 1.12%, which is the lowest level of agricultural and commercial banks. At the same time, in 18 years of regulatory requirements for banks to take the initiative to expose and strictly confirm the bad environment, Changshu Bank does not have the pressure to digest the history of bad baggage, and its "overdue loans / non-performing loans" has dropped to 62.2%.

Looking to the future, in the environment of increasing external economic uncertainty, investors' attention to the bank is bound to focus on asset quality, which can reflect its advantages for Changshu Bank.From a static point of view, the bad rate, bad leading index and bad identification of Changshu Bank are much better than those of the same industry; from a dynamic point of view, (1) based on the weak cycle credit structure of Changshu Bank, the risk of personal operating loans is lower, even if the economy is in a downturn. the impact is also limited. (2) at the same time, we also see that the provision coverage rate of 9M18 Changshu Bank has greatly increased from 325.93% at the end of 17 years to 406.74%, and the performance can still achieve more than 20% growth in the case of additional provisions, which shows that there is plenty of room for provisions to feed profits in the future.

5. 1.4x PB for 19 years, upgraded to buy rating

5.1 the valuation premium of Changshu Bank under the relative valuation method is not sufficient.

We select comparable companies to reasonably value Changshu Bank based on two dimensions. The current valuation level of Changshu Bank is not enough to reflect its excellent fundamentals:

(1) considering the nine cities and agricultural banks in the Yangtze River Delta region, according to the closing prices on November 16, the average PB of the nine comparable companies from 2018 to 2020 is 1.03X/0.94X/0.85X respectively, and the latest share price of Changshu Bank corresponds to 1.23X PB in 18 years. (2) from the perspective of fundamentals, China Merchants Bank, Bank of Nanjing and Bank of Ningbo, which have strong core profitability, improved ROE and excellent asset quality, are selected as comparable companies. The average PB of the three banks from 2018 to 2020 is 1.28X/1.15X/1.01X, while that of Changshu Bank in 2018 is 4%. No matter which comparable dimension, the valuation of Changshu Bank does not fully reflect the excellent fundamentals of better-than-expected performance improvement, high interest rate spreads and low bad.

5.2 continuous improvement of ROE is expected to drive revaluation

At the ROE level, although the current ROE of Changshu Bank is lower than that of China Merchants Bank, Bank of Nanjing and Ningbo Bank, from the perspective of marginal change, the core trend of continuous improvement of ROE can better confirm the certainty of enjoying valuation premium in the future. Compared with city commercial banks that used to rely on inter-bank expansion, Changshu bank's leverage level is not high; on the contrary, Changshu bank's ROA is as high as 1.04%, second only to Ningbo bank and Guiyang bank among the 12 urban rural commercial banks. We believe that the unique small and micro development strategy and prudent risk control system make the sustainability of Changshu Bank's performance growth particularly promising, and it is a high probability event to maintain high performance growth in the next three years, while sufficient provisions also increase the margin of safety in response to economic fluctuations, and the continuous improvement of ROE is expected to drive the revaluation. Net profit from 2018 to 2019 is expected to increase by 25.8 per cent, 26.3 per cent and 27.2 per cent year-on-year, giving a 19-year target valuation of 1.4X PB. The current share price corresponds to 19-year 1.07XPB, corresponding to 30.8 per cent upside space, upgraded to "buy" and included in the first portfolio of A-share banks.